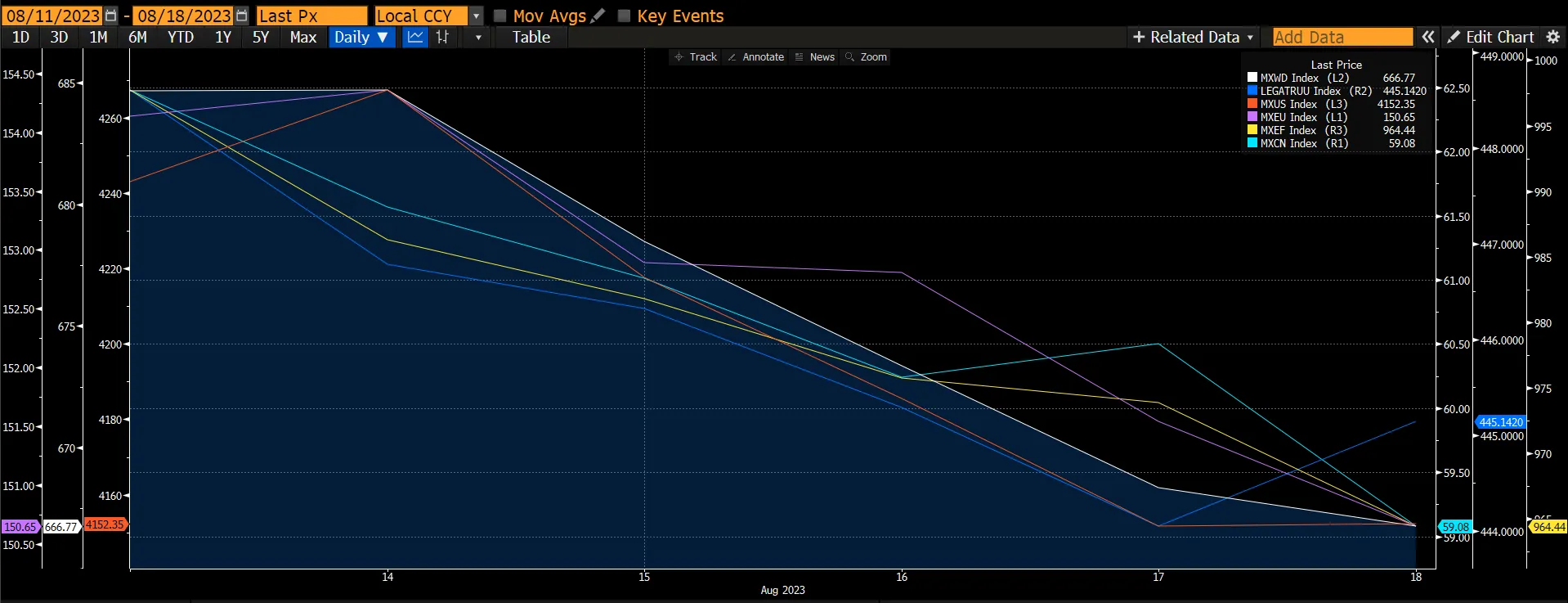

The global equities market experienced its worst week of performance since Oct 2022 (-2.62%) as concerns over higher global interest rates, rising concerns related to China’s housing market and its contagion to the financial economy, despite PBOC 2Q23 monetary policy report reiterating a supportive monetary policy stand. All major markets contributed to the fall of global equity markets with MXCN declining by 5.6% while MXUS and MXEU fell by 2.08% and 2.87% respectively. The global fixed income market also fell but to a lesser extent (-0.77%).

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

On 17 August, the US central bank’s July 25-26 policy meeting minutes were released. In the minutes, Federal Reserve officials largely remained concerned that inflation would fail to recede and that further interest rate increases would be needed. At the same time, cracks in that consensus were also becoming more apparent. “More participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy. But two Fed officials favoured leaving rates unchanged instead of the rate hike the Federal Open Market ultimately authorized at the conclusion of the meeting. The July rate hike brought the target range for the Fed’s benchmark rate to 5.25% to 5.5%, the highest level in 22 years.

The Fed staff no longer expects the economy to enter a recession, reflecting stronger-than-expected spending and activity data since the turmoil in the banking system in mid-March. However, the staff expects real GDP growth in 2024 and 2025 to be below its estimate of potential growth and projected “a small increase in the unemployment rate relative to its current level.” The staff judged that risks to its economic growth projections were tilted to the downside, in part because “additional monetary tightening” could be needed in response to “higher and more persistent inflation.” FOMC participants noted that GDP growth remained resilient in the first half of 2023, but that “a gradual slowdown in economic activity (appeared to be in progress)” and that tighter credit conditions would likely weigh on growth in coming quarters. Participants continued to judge that the economy needed “a period of below-trend growth and some softening in labour market conditions” for aggregate supply and aggregate demand to be brought into better balance.

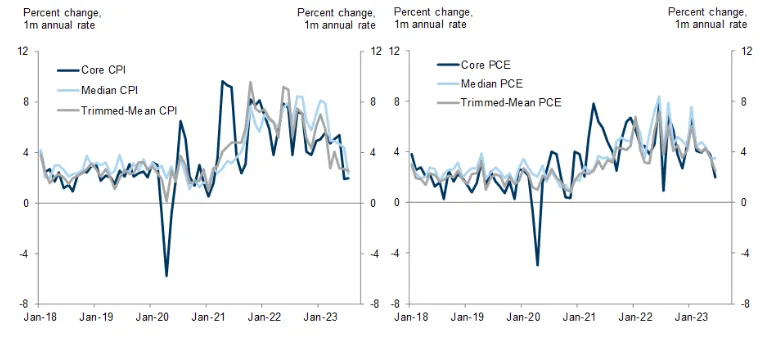

Figure 2: The Underlying Inflation Trend Has Slowed

Source: US Bureau of Labour Statistics, Federal Reserve, Bureau of Economic Analysis.

Source: US Bureau of Labour Statistics, Federal Reserve, Bureau of Economic Analysis.

The market currently does not expect another rate increase this year, according to futures contracts, though the implied probability of a hike at the 31 Oct – 1 Nov meeting is higher than the next meeting on 19-20 Sep. The market also sees the Fed commencing with rate cuts in 2025, with the benchmark seen falling to around 4.25% by the end of the year. Key economic data published since the July gathering have mostly supported the notion that Fed officials will have some time to deliberate on the need for more tightening. We, on the other hand, expect one more 25bps hike in rates this year before it starts to pivot next year. The Chinese market rallied about 10% in 5 days post the Politburo meeting but gave back all the gains in the first two weeks of August and is now just 1% above the YTD index trough in late May. The ailing housing market and its potential contagion to the real and financial economies are the main culprits for this current correction, in our opinion.

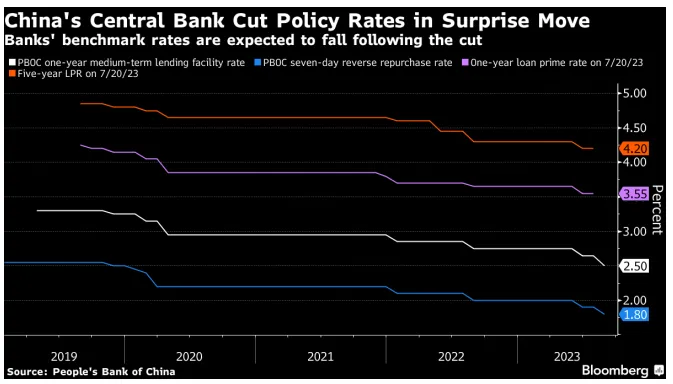

On 15 August, China’s central bank unexpectedly reduced a key interest rate by the most since 2020 to bolster an economy that is facing fresh risks from a worsening property slump and weak consumer spending. The People’s Bank of China lowered the rate on its one-year loans — or medium-term lending facility — by 15 basis points to 2.5%, the second reduction since June. A short-term policy rate was also cut by 10 basis points. Upon the announcement, the market reacted negatively by declining by 0.91% and 1.26% 2 days post the announcement. Until more forceful policy responses are made available to backstop the contagion risk, we believe investors will continue to lower their exposures to the Chinese market, but being mindful that the market is priced at already a discount to historical averages.

Figure 3: PBOC Lower Policy Rates

The housing demand weakness has been evident for the past 2 years, during which land sales, new starts, property sales, and completions have fallen about 50% from their respective all-time peaks in early 2021. But the pressures have recently percolated to the financial economy, as exemplified by: 1) the missed payments of its offshore USD bonds and the proposed onshore debt restructuring by Country Garden, the largest POE developer by assets and sales in 2022 with more than 3,000 projects nationwide; 2) Zhongzhi Group, one of the largest trust companies domestically that manage more than Rmb1t of assets in a Rmb21t industry, among which RMB1.6t of assets could be exposed to developer financing, failed the interest payments on some of its wealth management products (WMP); and, 3) the continuing LGFV issues for local government across the provincial, city, and municipality levels where explicit and implicit leverages are high and fiscal revenues are fairly dependent on the housing market (land sales and related taxes). Recall when the financial stresses by the then-largest developer Evergrande were spurring systemic concerns in mid-2021, MSCI China and CSI300 corrected 34% and 21% from May 2021 to Mar 2022 (when Evergrande suspended its equity trading), with most property-related cyclicals underperforming during that period.

Home prices in China fell for a second month in July, a further sign of the deepening property market downturn that’s weighing on the world’s second-largest economy. New home prices in 70 cities, excluding state-subsidized housing, fell 0.23% MoM in July vs a decline of 0.06% in June. Last month’s price decline was widespread, with 49 cities out of the 70 tracked by the government seeing new home values drop from a month earlier, the most this year. In the existing home market, where prices are less subject to government intervention, they fell in all but seven cities. Shenzhen, a bellwether city in the south saw prices slide 0.9%, trending closer to the level in June last year after Covid lockdowns. The declines offer no relief to developers like Country Garden which faces a potential default after missing bond payments this month as the housing market sputters. Risks are also spreading to the financial sector, where a trust company, Zhongzhi, with massive exposure to real estate missed payment on some investment products.

Figure 4: China Home Prices

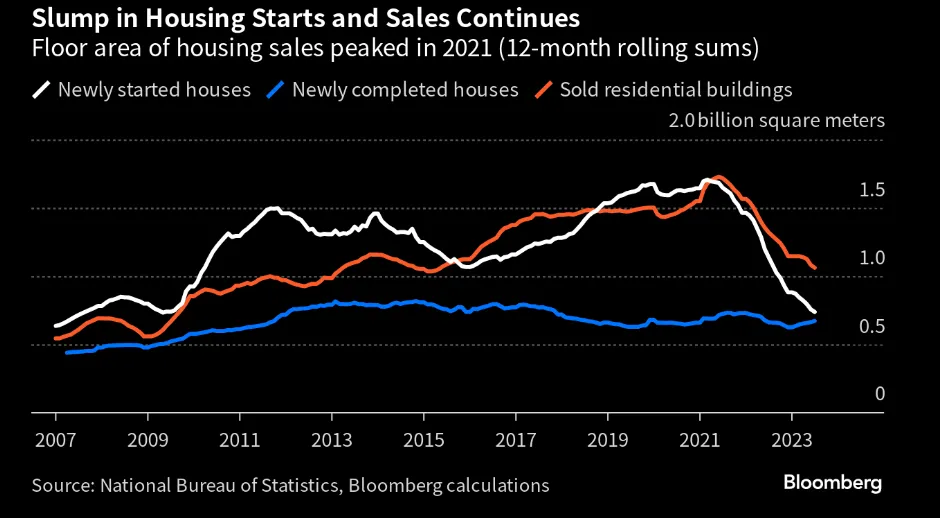

Figure 5: Slump In Housing Starts and Sales

Economists have cited China’s real estate as the sector in greatest need of aid, with the drop in new home sales in China recording a steep decline in June 2023. China’s huge property industry was long an important engine of economic growth, accounting for as much as 30% of the country’s GDP, and investors see the revival of the sector as crucial to China’s recovery. However, as long as sentiments remain poor, consumer demand will likely remain weak, setting up a vicious cycle in the Chinese property market that we see may take a significantly long time to recover. Currently, we are seeing many economists revising down their China GDP forecast closer to the government’s guidance of 5%.

According to Goldman Sachs, they view that the systemic risks stemming from the housing market appear to be well contained because: 1) while property-related debt is significant in size (Rmb58t, 47% of GDP), two-thirds of which is mortgage loans where the effective loan-to-value (LTV) ratios are relatively healthy and the aggregate homeowner equity in existing housing stocks looks sufficient to absorb substantial price declines; 2) the remaining one-third of the debt resides with developers, which seems more likely to incur losses and write-offs amounting to an estimated of Rmb2t (loss rate of around 10%). However, these debts are largely unlevered and the potential losses will mostly be borne by bondholders and trust investors as opposed to banks; and, 3) the institutional setup in China where the government has strong control over its banking system makes a market-driven, unordered unwind less likely to happen than would otherwise be the case.

For equities, we believe this current correction would be a shallow one and investors should take this opportunity to restructure their holdings and value hunt. Despite valuations deemed to be fair to expensive for developed markets (we view it to be fair), recent data and earnings releases are positive and should provide the catalysts to drive developed markets higher. We, however, would remain cautious and selective in China due to the disappointing corporate earnings, a crisis in the property sector, and economists are still revising their GDP forecasts down. While China’s equity market looks attractive by historical standards, the uncertainties and challenges would be a drag on the market. China is possibly a “value trap”.

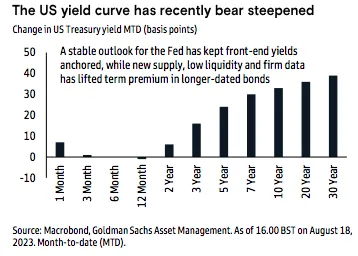

Fixed Income US Treasury yields rose again this week, with the 10-year yield ending 10 basis points (bps) higher at 4.26%. 2-year yields were muted, rising 5bps. Continued strong economic data drove the increase, with US retail sales expanding 0.7% month-over-month in July, almost double the expected pace. The data for June were revised up as well. Industrial production beat expectations, and US GDP growth estimates for the third quarter are being revised up across the board. The closely watched forecast from the Federal Reserve Bank of Atlanta has risen to 5.8% annualized quarter-over-quarter growth. That would be the strongest quarterly growth since 2003, excluding the post-Covid surge.

Figure 6: US Treasury Yield Curve

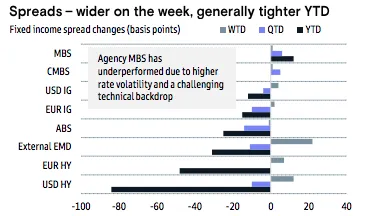

Investment grade corporates weakened, returning -0.71% for the week and lagged similar-duration Treasuries by -21 bps. This marks the fourth consecutive weekly selloff, as interest rates have steadily moved higher in August. High yield corporates also weakened, returning -0.81% for the week and underperforming similar duration Treasuries by -69 bps. According to July FOMC minutes, while “almost all” participants supported last month’s 25bps rate hike, “a couple” preferred unchanged policy, and others flagged “additional monetary tightening” could be required in response to “higher and more persistent inflation”.

Figure 7: Yield Spreads Widen

Source: Goldman Sachs

Source: Goldman Sachs

Emerging markets lagged materially, returning -1.45% for the week and underperforming similar duration Treasuries by -104 bps. Economic data from China continued to soften, with retail sales, industrial production, and fixed asset investment disappointing versus expectations in July. The official unemployment rate also ticked higher to 5.3%. Though the People’s Bank of China cut interest rates by -15 bps, more than expected the weakness in the data outweighed the support from policy.

With recent spread widening, both IG and HY corporate bonds look attractive value-wise. Softened recession prospects and predictable Fed policy trim off volatility in bond markets. However, within each sector, security selection is a key aspect to optimize the credit and market risk of the portfolio.