USA

Most of the major indexes moved higher over the week, with the S&P 500 Index reaching new highs and breaching the 5,000 threshold for the first time. The advance remained relatively narrow, however, with an equally weighted version of the index significantly trailing the standard market-weighted version for the fourth time in five weeks.

After a quiet start to the week, the market picked up momentum on Wednesday morning, seemingly helped by the solid reception given to the U.S. Treasury Department’s record $42 billion auction of 10-year notes. The auction calmed fears that the government’s record borrowing levels would push borrowing costs higher, thereby removing some of the Federal Reserve’s power to cut interest rates if needed to stimulate the economy in the coming months.

The week’s sole economic surprises arguably came on Monday morning in the form of S&P Global’s reading of services sector activity, which jumped unexpectedly to a four-month high and back solidly in expansion territory.

Treasury yields increased at the start of the week, spurred higher by the strong jobs report seen last week and Fed Chair Jerome Powell’s comments.Powell reiterated that he saw no need to cut rates immediately.

Europe

STOXX Europe 600 Index ended 0.19% higher on some strong company earnings updates. However, the likelihood of interest rates staying higher for longer curbed gains. Italy’s FTSE MIB rose 1.43%, while France’s CAC 40 Index advanced 0.73%. Germany’s DAX was little changed but remained near its record high. The UK’s FTSE 100 Index slipped 0.56%.

Japan

Japan’s stock markets gained over the week, with the Nikkei 225 Index rising 2.0% and the broader TOPIX Index up 0.7%. The Nikkei reached a 34-year high on yen weakness, prompting some profit taking, and gains were also capped by a pullback in expectations about a March rate cut by the U.S. Federal Reserve. Reports of strong foreign investor interest in Japanese stocks in January, on the back of a solid earnings season, were supportive of sentiment, as was the latest signal of Bank of Japan (BoJ) monetary policy continuity even after an exit from its negative interest rate regime.

The yield on the 10-year Japanese government bond rose to 0.72%, from 0.68% at the end of the previous week, struggling for direction as the BoJ provided assurances that financial conditions would remain accommodative. On these dovish remarks, the yen weakened to around JPY 149 against the U.S. dollar, from about 148 the prior week.

China

Stocks in China rallied in a holiday-shortened week as the government’s latest raft of stimulus measures offset concerns about deepening deflation. The Shanghai Composite Index gained 4.97%, while the blue chip CSI 300 added 5.83% for the week ended Thursday. Markets in mainland China are closed for the Lunar New Year holiday from Friday, February 9, and resume trading on Monday, February 19. In Hong Kong, the benchmark Hang Seng Index rose 1.37%.

Topic of the week - Airports of Thailand company

AOT reported 1QFY24 core profit of Bt4.6bn, +29% Q/Q , and ~10% below street estimate of ~Bt5.1bn. The miss largely resulted from higher-than-expected employee benefit expenses and D&A expenses, while non-aeronautical revenue were also slightly shy of expectations. 1QFY24 EBITDA moved +19% Q/Q, with the EBITDA margin expanding to ~64%.

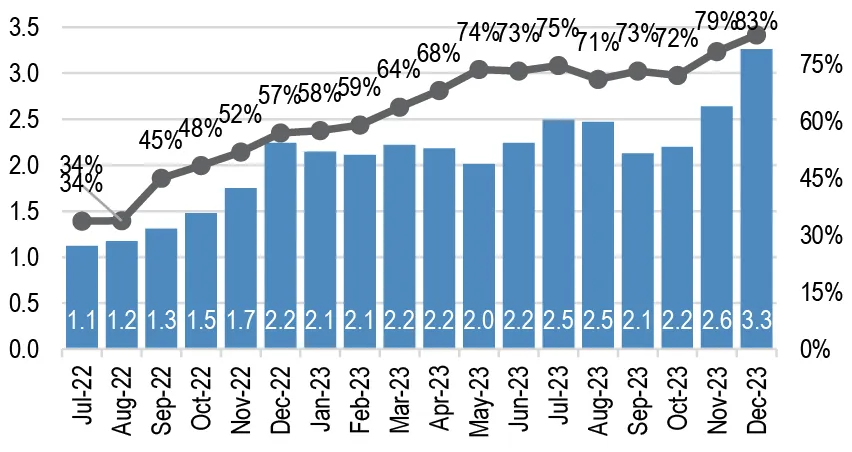

AOT reported 1QFY24 revenue +2% Q/Q, mostly driven by a ~12% Q/Q bump in Aeronautical revenue in line with international PAX volumes (+13% Q/Q). With Jan-Feb tourist arrivals run-rate at a healthy ~3.0mn per month (as Feb month is supported by the Coldplay concert, regional CNY holidays and an extra day being a Leap Year), we expect the aeronautical revenue momentum to sustain into 2QFY24, ahead of the potentially weaker seasonality build-up in Apr-Sep period.

Figure 1: Thailand: Foreign tourist arrivals in the last 18M (mn) and % recovery from 2019

Source: Ministry of Tourism of Thailand

Source: Ministry of Tourism of Thailand

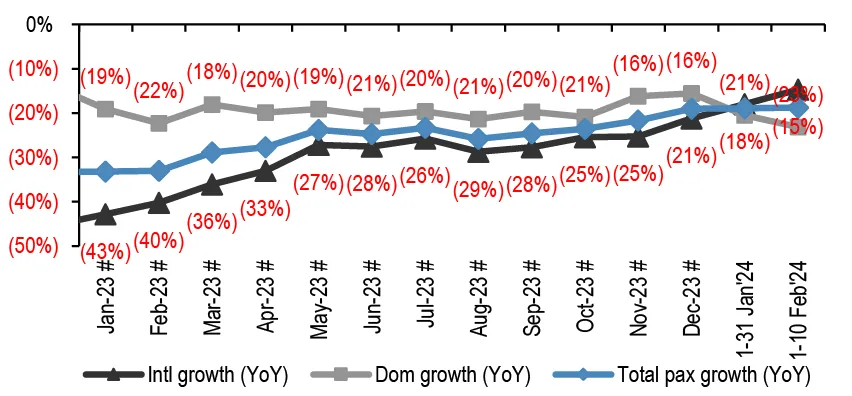

Figure 2: PAX volume growth Y/Y (%)

Source: J.P. Morgan

Source: J.P. Morgan

Key Negatives/Question Marks

AOT’s costs continue to drag the bottom-line below street expectations. Employee benefit costs have moved even higher from elevated levels by +22% Y/Y (-26% Q/Q due to seasonality of staff bonuses) as the company highlighted additional expenses from increased staff for ground handling services and security services, as well as staff bonus accrual.

Meanwhile, AOT’s aeronautical revenue fell ~5% Q/Q despite a jump in international PAX volume. This was slightly sub-par but could be largely attributed to a one-off office rental item in 4QFY23 of ~Bt0.5bn.

Investment Thesis

AOT’s share price has outperformed the SET index YTD, as the Thai tourism recovery, driven by growing arrivals from China, remains one of the most defensive themes for the market. AOT’s share price is highly correlated to international PAX volumes. Higher-than-expected costs could be a negative factor.