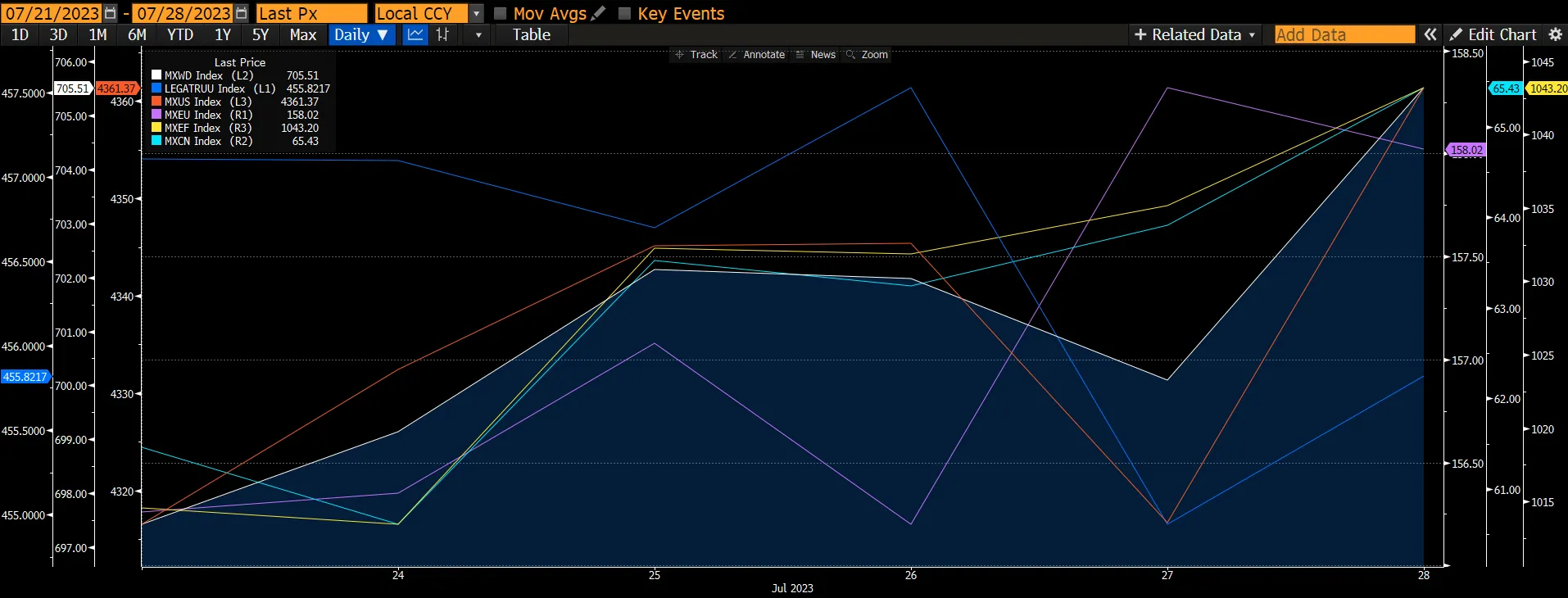

The global equity markets were higher for the week ending 28 July led by stocks in China after Beijing promised to take steps to bolster domestic demand, and expectations of the US interest rate peaking soon. The global market rally, initially driven by the mega-cap stocks previously, is broadening, with over 50% of companies trading above their 50- and 200-day moving averages for the first time in six months. The global equity market increased by 1.19% boosted by the emerging markets and the Chinese markets which rose 2.85% and 6.76% respectively. The US market continued to rally by rising 1.06% while the European market rose by 0.27%. The global fixed income market fell 0.28%, continuing to underperform the global equity market as risk-on sentiments persist.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

On Wednesday (26 July), the Federal Reserve resumed raising interest rates by hiking the Fed fund rate by 25bps to 5.25-5.5%, the highest level in 22 years. This was largely expected by the market as a 90% chance of a 25bps hike in this meeting was priced in. However, Powell failed to provide any clear signal about its intentions for the September meeting. “All of that information is going to inform our decision as we go into that meeting in September”. “It is certainly possible that we would raise (rates) again if the data warranted, and I would also say it is possible that we would choose to hold steady at that meeting”.

From Powell’s comments, we interpret that the economy is still resilient which makes core inflation difficult to forecast and the decision to raise or hold rates would therefore be very much data dependent. While Powell said that the FOMC would look at the totality of the data, he also said that it will be particularly focused on inflation and on whether forecasts that inflation will remain low prove right. Powell pointed to encouraging signs that the Fed’s efforts to curb inflation are working, but “what our eyes are telling us is the policy has not been restrictive enough for long enough to have its full desired effects.” FOMC intends again to keep policy restrictive until they are confident that inflation is coming down sustainably to the 2% target and are prepared to further tighten if that is appropriate.

In the FOMC statement, it repeated its description of inflation as “elevated,” and upgraded its description of economic growth to “moderate” from “modest”. It also reiterated that the banking sector is “sound and resilient,” while cautioning that credit tightening is expected to weigh on the economy.

Figure 2: Fed Target Rate

Source: Bloomberg

Source: Bloomberg

Other takeaways from the FOMC meeting were 1) Powell did not seem particularly concerned about the tightening in bank credit as he noted that bank lending has been stable quarter over quarter and up significantly year over year and he emphasized that “things have settled down for sure” since the recent bank failure; 2) Powell noted the Fed staff is no longer forecasting a recession, though it does still expect a noticeable slowdown in growth later this year; and 3) Powell clarified that it would not be self-contradictory for the FOMC to continue QT even if it started to cut the funds rate in the future because both actions would form normalization.

Meanwhile, the 2Q23 earnings season has thus far ushered in a more positive view toward stocks both via sentiment and fundamentals. Since the start of reporting, the S&P 500's 2024 earnings estimate has been on the rise, and revision momentum -- a breadth gauge that measures the percentage of companies with higher year-ahead estimates -- is back to flat for the first time since May. Likewise, pure cyclical sectors -- financials and industrials -- have surged ahead of their purely defensive peers (utilities and staples) over the past 12 weeks by the widest margin since 2021. Performance spreads as wide or bigger than the current have indicated strong forward returns for the large-cap gauge since 2014.

The S&P 500's pure cyclical sectors (Financials and Industrials) have staked out a large lead over defensive sectors (Utilities and Consumer Staples), which has historically been a positive signal for the S&P 500's performance. The pure cyclical sectors were up 9.4% on average over the last 12 weeks, while the pure defensives were down 2.1%, bringing the spread to 1,148 bps. This is the widest since the 12 weeks ended in early May 2021, and over the last 500 rolling, 12-week periods since 2014, has only been surpassed 34 times.

Cyclical sector outperformance has historically led to a continuation of the S&P's bull run. The S&P 500 has been up 5.3% on average in the 12 weeks after the cyclical-defensive performance spread surpassed 11.5% vs. just 2.1% when the spread is below that level.

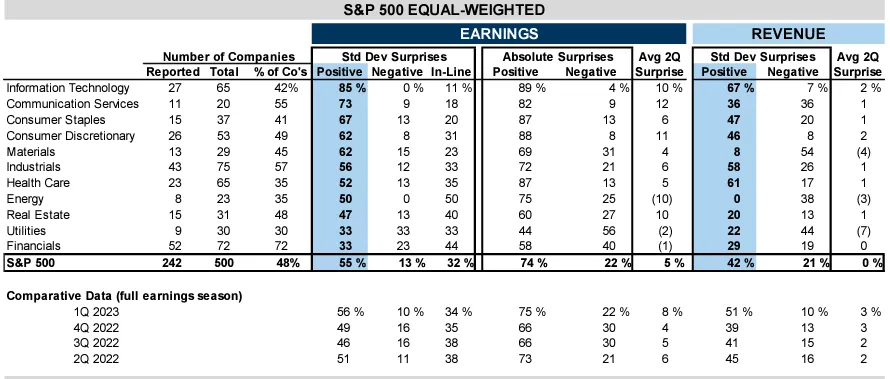

This earnings season has been “better than fear” as 48% of S&P 500 firms have reported. 74% of the companies have reported positive earnings surprises. The biggest positive surprises came from the IT and consumer discretionary sectors while the largest negative surprises were from the utilities and financial sectors.

Figure 3: S&P 500 Earnings Season Report Card

Source: Compustat, FirstCall, Bloomberg, IBES, Goldman Sachs Global Investment Research

Source: Compustat, FirstCall, Bloomberg, IBES, Goldman Sachs Global Investment Research

On 27 July, the Governing Council delivered the widely anticipated 25bps hike and President Lagarde indicated that the data will determine “whether and how much more ground” there is to cover. ECB officials acknowledged that growth has deteriorated and linked the weakening in demand primarily to the forceful transmission of the ECB’s tightening. The Governing Council noted that some measures of underlying inflation are now showing signs of easing (especially in goods) but that services inflation remains too high, reflecting rising wages. The council also softened its forward guidance and is now fully data dependent. The statement now indicates that future decisions will ensure that rates “will be set” at sufficiently restrictive levels to get inflation down to 2% (rather than “will be brought to”). ECB President Christine Lagarde noted during the press conference that upcoming meetings “could be a hike or could be a pause” but if the Council decides to pause, this would not necessarily be for an extended period and would be revisited at subsequent meetings with new data.

Lagarde did not repeat her previous verbal guidance that there was more ground to cover and instead noted that the data will determine “whether and how much more ground” there is to cover. She indicated that the Governing Council would consider “all data” between now and September where she focused on (1) the upcoming two inflation prints, (2) news on policy transmission (including measures of financing conditions and effects on demand), and (3) the staff projections, but put little direct emphasis on the activity data. She said that the focus on inflation will be on headline and core, measures of underlying inflation and the drivers of services inflation.

In the announcement, the Governing Council acknowledged the deterioration in the near-term activity outlook and linked weaker domestic demand to the effect of tighter financing conditions. The monetary policy statement continued to stress the resilience of the labour market but noted that forward-looking indicators suggested a slowdown in employment growth.

Figure 4: Signs of The Economy Slowing

While inflation is still judged to be “too high for too long,” ECB officials noted that some measures of underlying inflation are now showing signs of easing, especially in goods inflation. That said, ECB officials stressed that the drivers of inflation are changing away from external factors to domestic drivers, including rising wages and robust profit margins. President Lagarde stressed that firm services inflation is difficult to slow it down and that the progress seen so far is not “quite enough.” The Governing Council reiterated two-way risks around inflation but put new emphasis on potential upward pressure on food prices, following adverse weather and Russia’s termination of the grain deal with Ukraine.

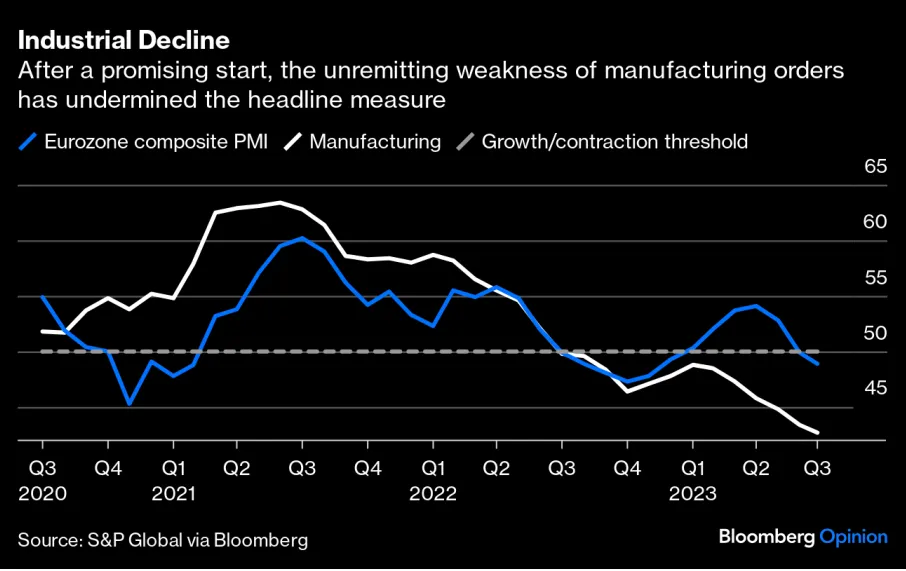

The Stoxx Europe 600 index has gained nearly 12% this year on a total return basis, with the large-cap Stoxx 50 climbing by more than 17%. Promising signs of European economic resilience, decent first-quarter earnings, and an AI-driven tech stock rally that has lifted stocks globally all contributed. But enthusiasm is waning.

Figure 5: European Equities Are Defying Signs Of Economic Weakness

Strategists see no reason to buy European equities. The average of 16 forecasts in a Bloomberg News survey of equity analysts is for a 2% decline in the wider index by the end of the year, with several major investment banks expecting a sharper drop. Bank of America Corp.'s July survey of European fund managers shows two-thirds of investors expect stocks to decline over the rest of this year. More than 80% of those surveyed reckon earnings per share will deteriorate.

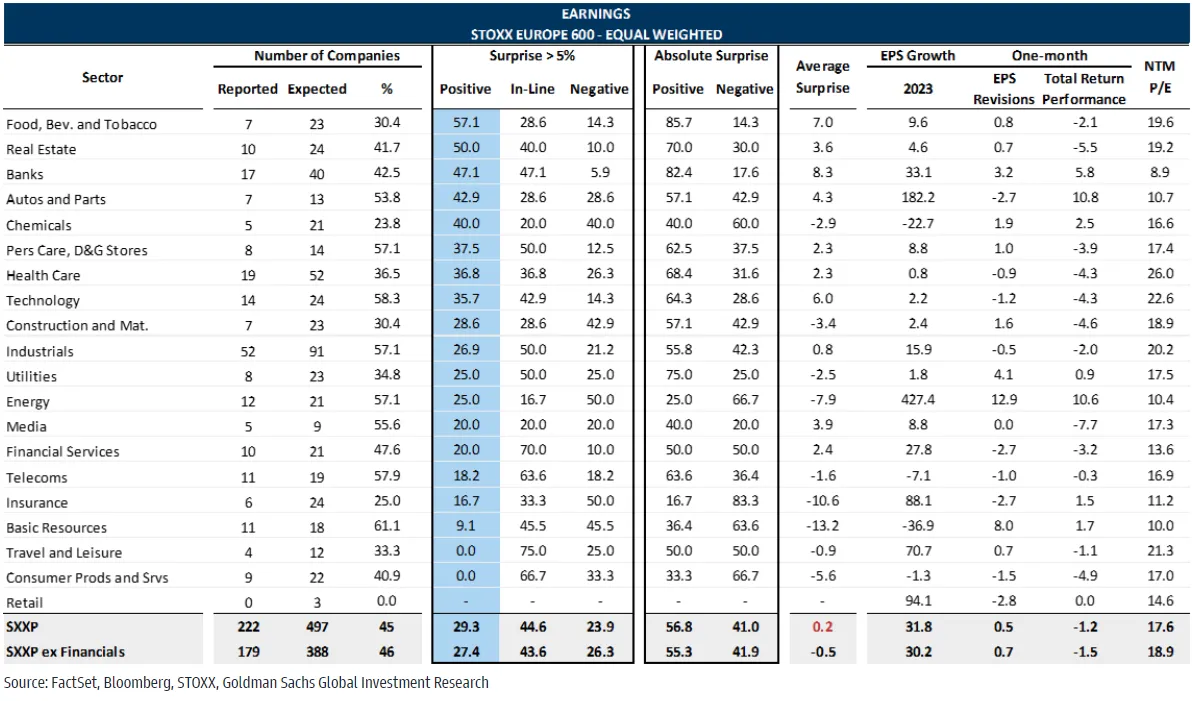

However, for this 2Q23 earnings season, so far 45% of STOXX companies have reported earnings and 56.8% of the companies’ earnings had surprised on the upside. According to Goldman Sachs, the number of positive beats is low; only 30% of companies beat consensus estimates by more than 2% - below the long-term average of 40% and levels seen in recent quarters. The low share of beats comes against already negative revisions and softer sentiment going into the season.

Figure 6: STOXX 600 2Q23 Earnings Report Card

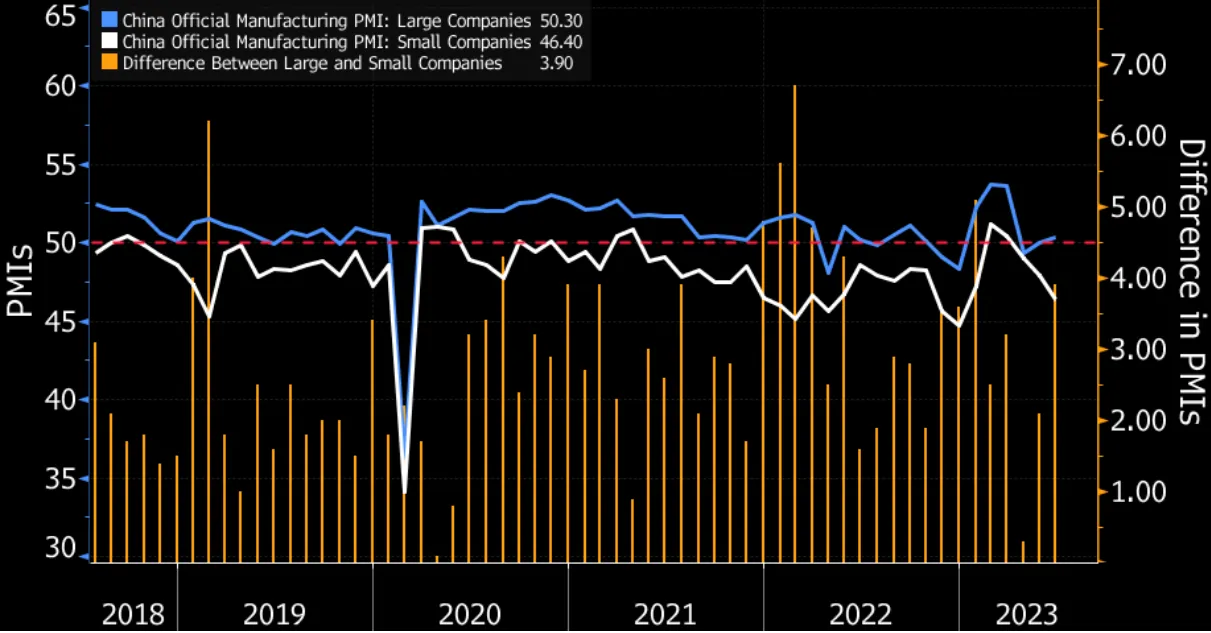

China’s economy is continuing to display a slower momentum than many economists expected at the start of the year. Year-on-year growth in 2Q23 was much slower than the market was expecting, while quarter-on-quarter growth of 0.8% was far below the 2015-2019 average of 1.4%. It was slow compared with other economies at a similar stage of recovery from the pandemic. Many of the factors damping growth – most notably weak sentiment and a troubled housing market — are likely to extend into 2H unless the government provides a significant stimulus to help the ailing industry. Furthermore, a lack of confidence has suppressed consumption and private investment. This is unlikely to turn around quickly. The recovery pace in retail sales – a key indicator for consumption – slowed noticeably in 2Q23. Total investment decelerated in 2Q23, as flagging private investment offset strong public spending on infrastructure. Small private firms saw widening contractions in activity even as large firms started to stabilize toward end-2Q. Higher unemployment, especially among young people, is damaging confidence.

The property market cooled in 2Q again after a brief rebound. The government’s shift to a more supportive stance prevented a costly crash. Yet increased economic uncertainty and well-understood changes in housing fundamentals, together with the government’s clear intention not to prop up the market, rule out a strong comeback. Real estate investment shrank 7.9% in 1H, more than double the 3% contraction which is projected. External demand will remain negative for China’s recovery. Bloomberg Economics projects US growth will slow in 2H as the Federal Reserve’s aggressive rate hikes start to take a heavier toll. This will therefore hurt China’s exports, which dropped sharply in 2Q on a year-on-year basis.

Figure 7: Divided Between Big and Small Firms

Source: NBS

Source: NBS

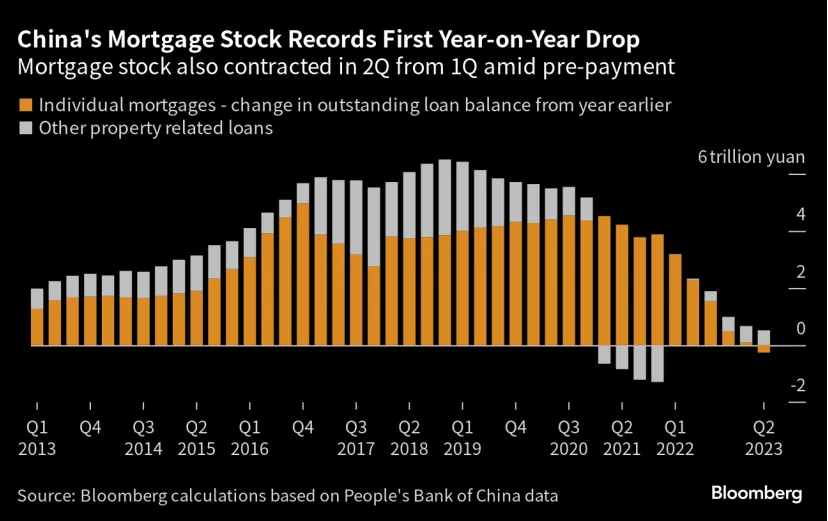

The bane of China’s economy is the housing market. The total amount of money lent out to buy homes shrink from a year earlier for the first time on record. The outstanding amount of individual mortgages fell to RMB38.6t at the end of June, down RMB260b from the same period a year earlier, according to data from the People’s Bank of China released on 28 July. This is the first year-on-year drop in the data going back to 2011 and the third QoQ contraction. The data also indicates people across the country repaid more than what was borrowed for new mortgages in the April-June period, showing the housing market is shrinking again after a short-lived rebound in 1Q23. According to Bloomberg calculations based on data provided by China Real Estate Information Corp, the market looks to have weakened further in July, with the weekly average of new housing sales by floor space in China’s tier-one cities on track to hit a six-month low.

Despite the strong month for China, we would remain cautious and selective in China. To date, we have only heard the intention to further stimulate domestic consumption and aid for the property sector, but there hasn’t been anything concrete announced yet.

Figure 8: China’s Mortgages Fell

On the fixed income front and following Fed decision to raise interest rates by 0.25%, the market ended the week pricing in only a 27.4% chance of further rate hikes by the end of the year. Furthermore, Friday’s reassuring inflation data helped push U.S. Treasury yields down, but the yield on the benchmark 10-year note ended the week sharply higher on strong growth signals.

The Bank of Japan (BoJ) signalled a change to its yield curve control (YCC) policy by injecting some flexibility into its YCC policy and indicated a loosening of its defensive cap on interest rates. While BOJ maintained its target for a 10-year Japanese government bond (JGB) yield at 0%, it however widened the top of the target band from 0.5% to 1%. This means the central bank would offer to buy JGBs at 1% in fixed-rate purchase operations.

BoJ governor Kazudo Ueda stated the change did not represent a "step towards policy normalization. Rather it’s a step aimed at enhancing the sustainability of yield curve control." However, some participants saw the move as the first step towards an eventual shift from the BoJ's long-standing ultra-loose policy stance. Following the announcement, on Friday 10-year JGB yields jumped to the highest levels since 2014.

Spreads tightened throughout the week in the investment-grade corporate bond market, led by mid-tier banks. High yield securities felt some pressure as risk assets turned lower on news that the Bank of Japan (BoJ) had announced a potential change to its yield curve control policy.