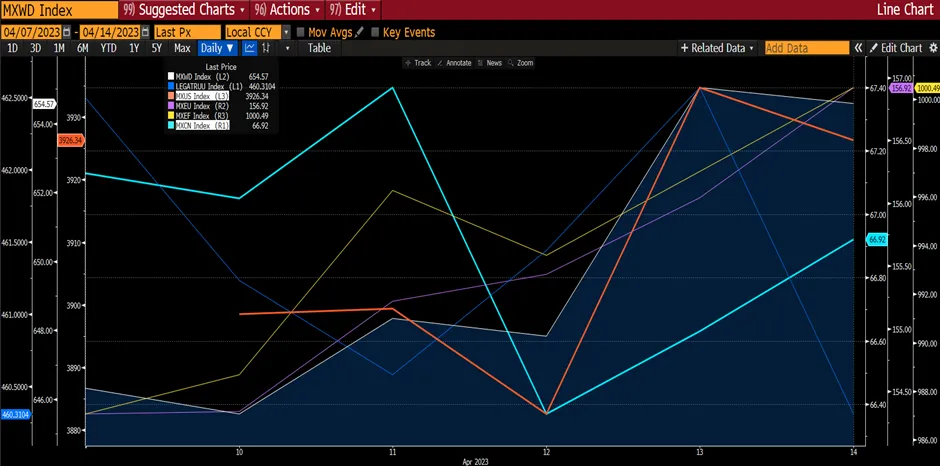

Global markets sold off on the back of 1) Silicon Valley Bank fallout with possibility of contagion across global banks; 2) Chinese government announced GDP growth of 5% that is in-line to below market expectations, 3) jitters from Fed Chairman may need to re-accelerate interest rate hike, and 4) Silvergate Capital filed for voluntary liquidation. Global equities index (MXWD) fell 3.54%, underperforming the fixed income index that rose 1.31% as investors feared a recession and fleeing to safe haven. MXUS fell 4.71% while MXEF (emerging markets) declined by 3.28%, partly the effect of MXCN (China) declining by 7.25%. MXEU (European Union) continues to outperform global markets by dropping just 1.7%.

Figure 1: Performance Of Key Indices

Source: Bloomberg

Source: Bloomberg

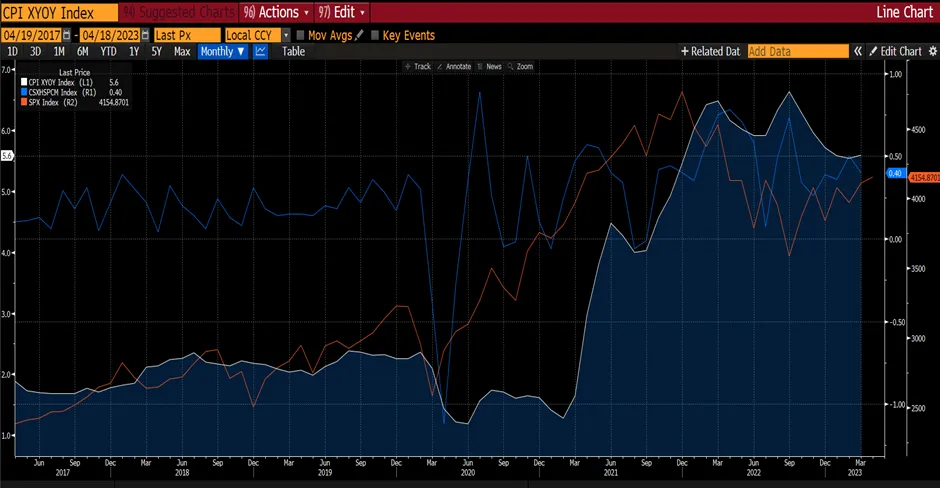

The US economy has remained more robust than expected so far this year as more than half a million net new jobs were created in January and, and the unemployment rate fell to its lowest level in 53 years. Retail sales rose 3% compared to December, one of the biggest monthly increases of the past 20 years. The service sector also unexpectedly rebounded: The ISM services index rose to 55.2 in January after dipping below 50 the previous month.

The question investors are now grappling with is whether this represents good news or bad news.

Of course, better-than-expected growth is a good thing, and resilience against higher interest rates could suggest a higher chance of the US economy achieving a soft landing, in which inflation falls back to target and growth remains positive. But equally, a stronger economy and a resilient labour market could also suggest the Fed may have to raise rates a lot further to cool inflation. The annual rate of consumer price inflation declined only modestly to 6.4% in January from 6.5% in December, and the Cleveland Fed’s trimmed mean, a gauge that strips out the biggest price moves, was up 0.6% on the month.

However, less than five weeks after the FED slowed its pace of interest rate hikes, Fed Chairman Jerome Powell has served warning it may need to re-accelerate interest rate hikes. Powell on 1 Feb declared he could now say the “disinflationary process” had begun but delivered a notably different message at a congressional hearing on 7 March 2023. “The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rate is likely to be higher than previously anticipated. If the totality of the data were to indicate that faster tightening is warranted, the Fed would be prepared to increase the pace of rate hikes.” The hawkish guidance has led to some economists raising the peak rate in the near term. Goldman Sachs raised the peak rate forecast by 25bps to 5.5-5.75% and we believe others will follow suit soon. We believe the resetting of base case rates have begun and talks of recession would begin to resurface as interest rates inch higher to suppress the stubborn labour market.

Figure 2: Economic Data Has Positively Surprised Globally, Lifting Policy Rate Estimates

Source: Bloomberg, Citi Group

Source: Bloomberg, Citi Group

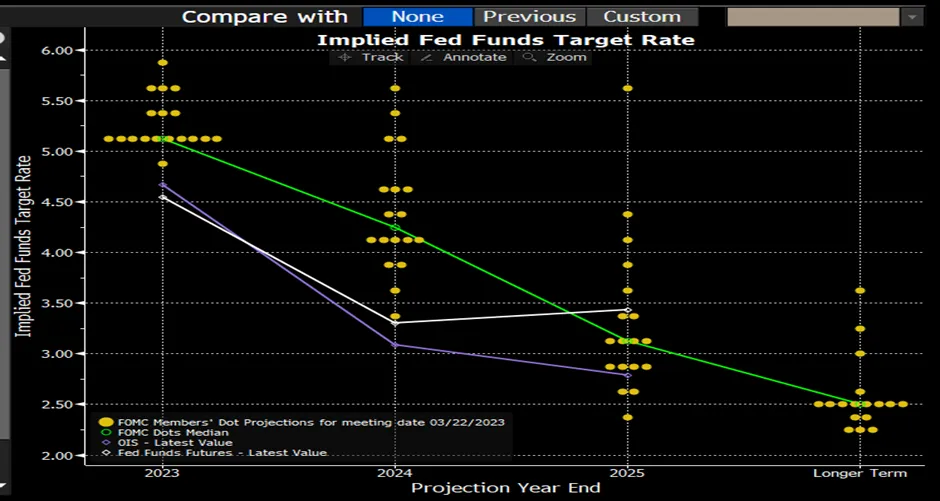

As rates would continue to be “higher for longer”, fears of recession resurfaced as treasury curve inversion deepens. The two-year Treasury note’s yield increased to 5% for the first time since July 2007. It has jumped from a 2023 low of 4.03% in early February as traders adopted higher forecasts for the peak Fed policy rate. This spooked the market once again.

Figure 3: Treasury Curve Inversion Deepens

While recession risk rises, 2 banks – Silvergate Capital and Silicon Valley Bank – announced that they are faced with liquidity issues.

Silvergate Capital (a central lender to the crypto industry) announced it would voluntarily wind down its operations and liquidate the bank. It blamed the “recent industry and regulatory developments” for its woes. These regulatory developments covered a host of issues, from a Justice Department investigation to growing moves by the Federal Reserve and other federal agencies with oversight of the banking industry pushing these institutions far away from crypto. The shutdown also raises new doubts about the relationship between traditional banks and the cryptocurrency world. Without Silvergate now, several crypto exchanges (such as Crypto.com) would be struggling to figure out how to allow customers to move money into their trading accounts and off-ramp them into their bank accounts.

Separately, Silicon Valley Bank announced that 1) management significantly increased their estimates for the pace of customer deposit withdrawals in 1Q23, 2) the company liquidated the bulk of their Available for Sale securities at a $2b loss, contrary to market expectations that they would tap alternate channels to raise liquidity before selling securities at a loss, and 3) the bank announced a capital raise to help replenish its liquidity. Given the rapid withdrawal of deposits last week, the FDIC (Federal Deposit Insurance Corporation) placed Silicon Valley Bank into receivership. As part of that initial announcement, insured depositors with account balances up to $250,000 were set to be paid in full on 13 March. The fate of uninsured depositors — representing about 90% of SVB’s total funding base— was more ambiguous, featuring an initial payment next week likely worth 30-50% of their outstanding deposits and a claim on future recoveries as SVB assets matured or were liquidated. Uninsured depositors would not have immediate access to their funds and could even suffer losses in certain scenarios that increased the risks of contagion, especially among smaller banks.

As a result, the Federal Reserve and the FDIC announced a set of emergency measures to safeguard depositors on Sunday evening (12 March). The FDIC designated the third bank casualty, Signature Bank (NY), and SVB as systemic risks to the financial system, which gave them the authority to backstop uninsured deposits at both institutions.

Figure 4: SIVB Deposit Funding Mix (as of 3Q22)

At the same time, the Federal Reserve introduced the Bank Term Funding Program (“BTFP”), which allows banks and other depository institutions to pledge US treasuries, agency mortgage-backed securities, and other qualifying assets—at par value—in exchange for a loan with maturities of up to one year. This liquidity source essentially eliminates the need for banks to sell high quality securities at a loss to meet deposit withdrawal shortfalls. The Fed also indicated that it stands ready to address any liquidity pressures that may arise.

What is the risk of contagion in the banking sector? The policy measures described above are significant and directly aimed at preventing contagion risk from spreading in the US banking sector. We think that risk is also mitigated by the fact that the broader banking sector — especially the large systemically important banks — do not share the same idiosyncratic vulnerabilities of Silicon Valley Bank, which included: 1) high industry concentration; 2) rapid growth in deposits, 3) rapid growth in lower yielding securities, 4) raising liquidity where its equity price below tangible book value. Moreover, the banking sector today is significantly healthier (across all matrices) than prior to the GFC and with the forceful policy response to provide that backstop to an idiosyncratic nature of SIVB’s vulnerabilities, it will indeed lower the risk of a contagion. Unlike GFC concern (credit quality), today risk for SIVB is due to interest rate / mark to market losses. We believe following the announcement by the Fed, the contagion risk in the banking sector should ease.

The SVB situation is an effect of Fed interest rate hikes. While investors will be relieved that SVB should be a contained risk, the economic outlook for the US has not changed with the plausibility of either a hard or soft landing. Because of this potential `banking crisis”, the market is now pricing in a 50% chance of a25bps rate hike at the March meeting while Goldman Sachs now predicts a pause in the rate hike for the March meeting.

In summary, the new liquidity measures from the Federal Reserve and the announcement that both SVB and Signature's depositors will be made whole looks to have shielded the banking industry from further contagion risk. With the Fed stepping in with new available funding, banks have effectively bolstered liquidity capacity to fund operations. The US banking sector may have averted another financial crisis for now. Nevertheless, we view the backstop by the Fed could provide some support to the falling market in the near term.