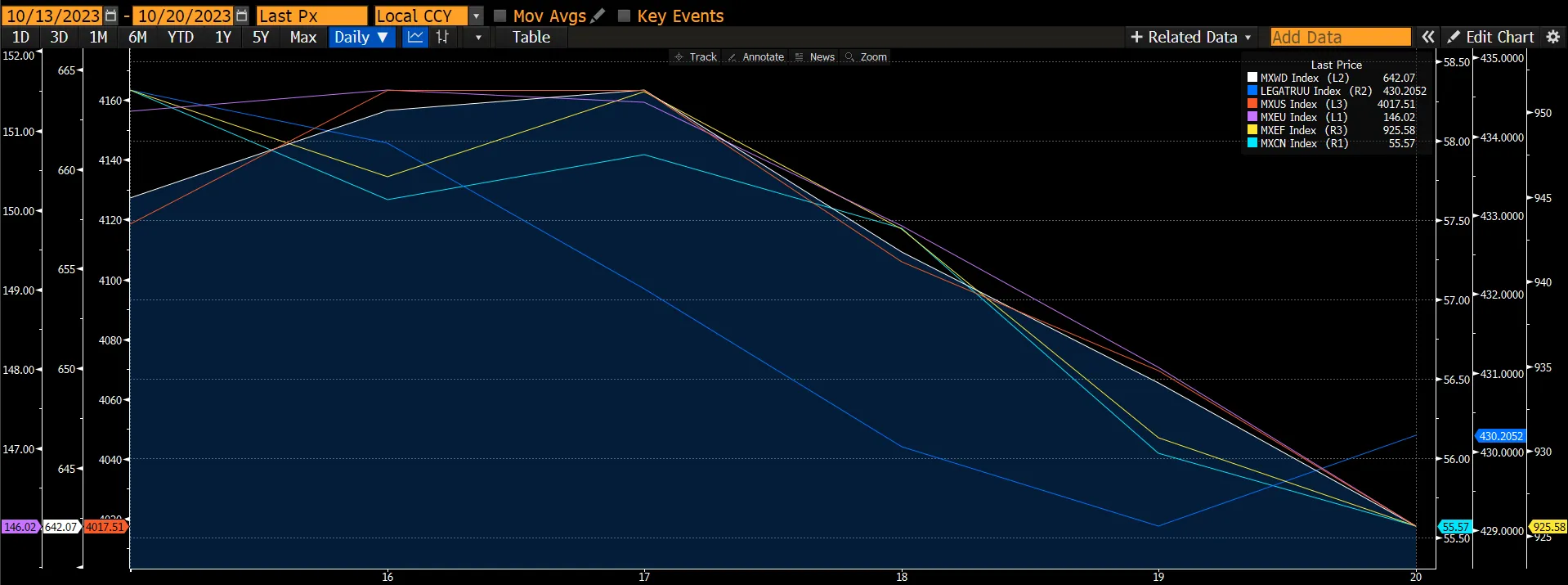

Spiking rates continued to punish long-duration equities despite generally better-than-expected earnings results this season thus far. The global equities market fell sharply by 2.49% caused by the rise of a 10-year yield past the 5% level, the first time since 2007. The decline was partly led by the Chinese markets that fell at a faster rate of 4.73% as the Biden administration curbed the export of more AI chips, the UST 10Y yield rose after Chair Powell stressed that the FOMC “is proceeding carefully” in light of two-sided risks, China’s property market remains a concern with Country Garden missing a $15m coupon repayment, and property prices fell further in September. The US and European equities markets fell by 2.44% and 2.69% respectively. The global fixed-income markets fell by 1% stemming from the rise in yields and outperformed the global equities markets.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

Topic on focus: Hamas-Israel conflict and investment implications

Geopolitical developments have shocked the world, altered the course of history, and dominated the headlines. But oftentimes, financial markets are not impacted proportionally. This looks to be the case two weeks into the latest crisis following Hamas’s attack on Israel. The broad market reaction to date could be described as mostly muted. The S&P 500 was up slightly in the first week following the attack, reflecting the view that this currently remains a local conflict with a mostly local impact on financial assets. While stocks came under pressure last week, this was more likely due to the sharp rise in yields.

Still, more pronounced moves since the attack in geopolitically sensitive asset classes like oil (Brent crude up 11%) and gold (up 9%) have brought questions about side effects for the economy, and the best way to hedge against any worst-case scenarios.

When it comes to the market reaction from here, oil remains the main transmission mechanism, and a significant move higher is the key risk to watch. While there is no set oil price that will tip the economy into a recession, the relationship with the US consumer is very much linear: Every dollar that gasoline prices rise as a result causes a bit more pain, incrementally redirecting spending from elsewhere. This, of course, has a trickle-down effect on earnings and complicates the Federal Reserve’s battle against inflation.

As we know, geopolitical risk premiums can disappear quickly. And whether the initial moves intensify will depend on how relationships in the Middle East evolve among Israel, Hamas, other local and regional players, and most importantly, Iran.

As of now, it is expected that oil prices will spiral out of control. It is believed the most likely scenario is that Brent crude oil fluctuates between USD 90/bbl and USD 100/bbl, alongside any local escalations such as involvement from Hezbollah. While pressure toward the USD 105–110/bbl range is possible with an incremental reduction in Iranian exports, there is currently spare capacity sitting with OPEC+ to help offset the impact.

A more pronounced move above USD 120/bbl likely would only come with significant supply disruption. There are a few ways this could feasibly play out: through a larger removal of Iranian oil from the market; a closure of the Strait of Hormuz, which accounts for over 20% of the world’s daily flow; or by some form of coordinated embargo among Arab countries, like the Yom Kippur War in 1973.

Figure 2: The Strait Of Hormuz Is An Important Place To Consider

Source: Reuters

Source: Reuters

But while none of these outcomes can be ruled out, they are currently tail risks. Initial reactions from the US have skewed toward de-escalation, and with Israel immediately focused on its imminent ground operation in Gaza, the desire to confront Iran is likely low, at least in the near term. And even if oil prices did move to extreme levels temporarily, it is expected them to be sustained.

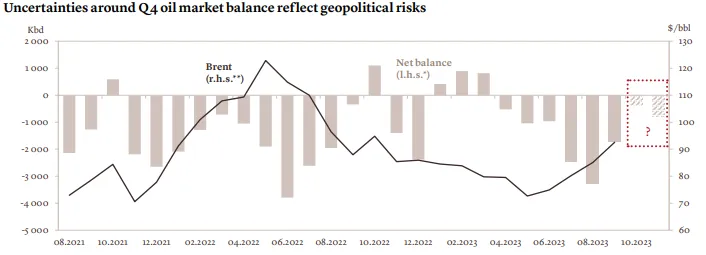

Figure 3: Oil and geopolitics

Source: Lombard Odier

Source: Lombard Odier

Finally, it’s worth noting that what’s most important to the consumer is the end-product at the pump. Despite the recent uptick in crude oil prices, gas prices have actually been falling, and data suggests they may be relatively less sensitive to spikes in oil prices at the moment.

The base scenario is that oil prices remain relatively contained, and as long as supply disruptions don’t feed through to the consumer for a prolonged period, the Israel-Hamas war is unlikely to be a main driver of the macro picture for now.

To hedge or not to hedge

Outside of uncertainty around oil prices, perhaps the most common investment-related question accompanying any war or crisis is whether investors should buy gold. If you look at history, while no two risk-off events are identical, the percent change in the gold price has been around the mid-single digits, on average.

Once again, it has been seen that gold proved its worth as a geopolitical hedge in the days and weeks following Hamas’s attack. This supports the view that gold’s importance in long-term portfolios has only increased in recent years alongside geopolitical unrest, and it is believed investors should hold onto existing positions despite the latest rally.

To be a buyer of gold here, one must believe this conflict is going to meaningfully escalate—which is not yet the base case. And in the absence of a major escalation, one would be left with a relatively uncertain fundamental picture. It is expected the US dollar to remain resilient in the coming months, and while correlations between gold and the USD have broken down recently, that usually does not last for too long.

It’s important to remember that geopolitical events have rarely caused a global recession or left a lasting mark on markets. Therefore, the best course of action is almost always to stay diversified and stay invested. But when answering specific questions on how to position, each event needs to be assessed alongside the fundamental backdrop. In this case, the Israel-Hamas war comes at a time of already elevated geopolitical tensions, with the ongoing war in Ukraine, and the intense rivalry between the US and China.

At the same time, even though the global economy has remained very resilient, it is expected growth to slow in the fourth quarter, inflation to continue to cool, and yields to trend lower over the next 12 months.

Against this backdrop, we recommend that investors buy high-quality bonds, which now boast great potential for price appreciation alongside compounding.

For equities, there was some positivity within the energy sector prior to the attack by Hamas, given that the supply-and-demand backdrop was supportive of current oil prices, and among other factors. The war further supports a positive view on the energy sector and provides a hedge in the event of an escalation and further rise in oil prices.