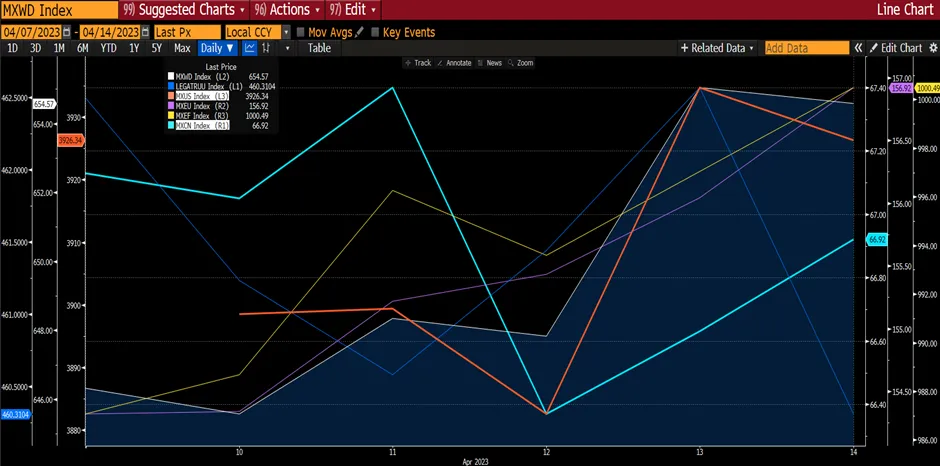

Markets trended higher this week fluctuating on the back of results announcement this week and waiting for Fed announcement on interest rates (on 31 Jan). China was closed for the week. MXWD rose 2.14% on the back of MXUS rising by 2.6% and MXEM increasing by 1.71%. MXEU also rose by 0.83%. The fixed income market (Bloomberg Global Total Aggregate Index) fell by a mere 0.03%. It appears that investors are taking on more risk as USD is at a near nine-month low and hopes for a pause in interest rate hikes (as per cited by Bank of Canada). Next Fed meeting will be on 31 Jan 2023.

Figure 1: Major Indices Week Performance

Source: Bloomberg

Source: Bloomberg

Hong Kong market (HSI) on the first day back after the Chinese New Year holidays (26 Jan 2023) rose by 2.4% driven by HK listed Chinese technology companies surging by more than 3%. Investors took on the view that technology equipment would see an improvement of demand from the reopening of China. This was despite results from US tech giant Microsoft warning that revenue growth in its cloud computing business will decelerate in the coming months and corporate software sales will slow fueling concerns about demand for the products that have driven its momentum in recent years. Other tech companies (Texas Instruments, Teradyne, Intel, IBM) guidance also affirms the weakness in revenue going into 1Q23. China tech companies were further affected with news that Japan and Netherlands are poised to join the US in limiting China’s access to advanced semiconductor machinery.

Can China save the world demand for electronic products? We believe so! China is one of the largest consumers and producers of electronics products. Take Apple’s iPhones as an example. Sales from China accounts for 17% of total sales (in 4Q22) while 70-80% of iPhones are being produced in China as well. During the Covid lockdown in China, Apple’s sales were affected by the production bottleneck while demand was still relatively strong. To mitigate similar experience in the future, manufacturers are moving some productions out of China into India, Brazil and even Mexico. With the US CHIPS act being put in place, with Japanese and Netherlands announcing they too will adopt the act, production bottlenecks could continue in China. The move out of China, in our opinion, would continue to help ease supply constraints to satisfy demand.

Figure 2: Revenue Of Apple By Geographical Region

China’s high frequency data signal spending surged during China’s first unrestrained Lunar New Year celebrations since 2019, the release of pent-up demand. Most of the data suggest that the reopening will be rapid, and that consumer spending should provide key support to recovery. This is also confirmed by LVMH comments that they too see demand returning from the re-opening of China’s economy. Anecdotal evidence of this strong recovery are seen by 1) Hotel bookings in the first 4 days of the holiday exceeded the comparable period in 2019; 2) 308m people travelled for sightseeing. This amounts to more than 1/5 of the population, 23% more than in 2022 and comes within 12% of the pre-crisis level; 3) Tourism revenue increased 30% compared with last year but was still about 27% less than in 2019; 4) Revenue at major retailers and restaurant rose 6.8% during the Lunar New Year period from 2022; and 5) Box office revenue exceeds those in 2022 and 2019 holidays. Although the improvement seen in the holiday figures may not be sustainable, investors will still likely pay close attention to these data because of a lack of other figures that the government doesn’t publish. Overall, we are comfortable with China's recovery and the Chinese markets have now entered the bullish trading territory.

Figure 3: China GDP Growth Forecast

On the other side of the globe, there are further signs of the US inflation slowing, which was previously held up by sticky wage growth and strong consumer spending. We are beginning to see that the consumers’ stockpile of savings diminishing and access to credit is becoming harder with the rise in interest rates. These factors help ease inflation. Furthermore, falling prices and weakness of energy prices are also helping to cool the inflation. Other anecdotal evidence is the number of companies that are scaling back their employee headcounts such as Goldman Sachs, Google, Amazon, Microsoft (representing more than 10% of the headcounts) have all announced job cuts in anticipation of a slowdown in business going into 2023.

US 4Q23 GDP grew by 2.9% which is a slowdown from 3Q22 growth of 3.2% but ahead of the consensus forecast of 2.6%. The quarter print means that the US economy did see a slowdown in growth. Imports and exports both fell with seasonally adjusted annual rates of -4.6% and -1.3% respectively. This suggests that recession could be avoided, or a soft landing is imminent. The increase in real GDP primarily reflected an increase in consumer spending, exports, private inventory investment, and nonresidential fixed investment that were partly offset by decreases in residential fixed investment and federal government spending.

Figure 4: US Core PCE Declining

Source: Bloomberg

Source: Bloomberg

Figure 5: Real US GDP

Source: Bureau Of Economic Analysis

Source: Bureau Of Economic Analysis

Consumer spending, which fuels about 70% of the US economy, is likely to soften in the months ahead, along with the still robust job market. The resilience of the labour market has been a major surprise. Last year, employers added 4.5m jobs vs 6.7m jobs added in 2021. Unemployment rate hit the lowest in 53 years at 3.5%. As per discussed above, the job market would likely see unemployment rise and as higher rates make borrowing and spending increasingly expensive across the economy, many consumers should begin spending less, and employers will likely hire fewer.

Figure 6: Business Leaders Much More Downbeat than Production, Shipment and Employment

Source: Haver Analytics, Bloomberg, US Federal Reserve Bank, GS

Source: Haver Analytics, Bloomberg, US Federal Reserve Bank, GS

Business surveys are suggesting a gloomy outlook ahead in 1Q23, with Empire Fed business conditions and several prominent measures already at recessionary levels. Subjective measures like business conditions were a helpful leading indicator during the financial crisis and subsequent recovery but proved excessively negative during the US-China trade war period. Nevertheless, business sentiments are negative and suggest that the business environment would be difficult going forward. With lower sales expected, margins are also expected to decline.

While waiting for the Fed to meet on 31 Jan 2023, consensus is expecting a 25bps interest rate hike. Although some investors would take this as positive from the view that rate hikes are slowing (from 50bps at the last meeting), we believe the Fed could provide guidance that rate hikes could continue for a longer period. This could dampen the sentiments and disrupt the market's current upward momentum.

In summary, the rally has already provided a 6-7% rise in global equities since the beginning of the year. Although we hold the opinion that the market would trend higher this year, we would however continue to see volatility as earnings and guidance are being released and caution towards Powell’s guidance with regards to rate.