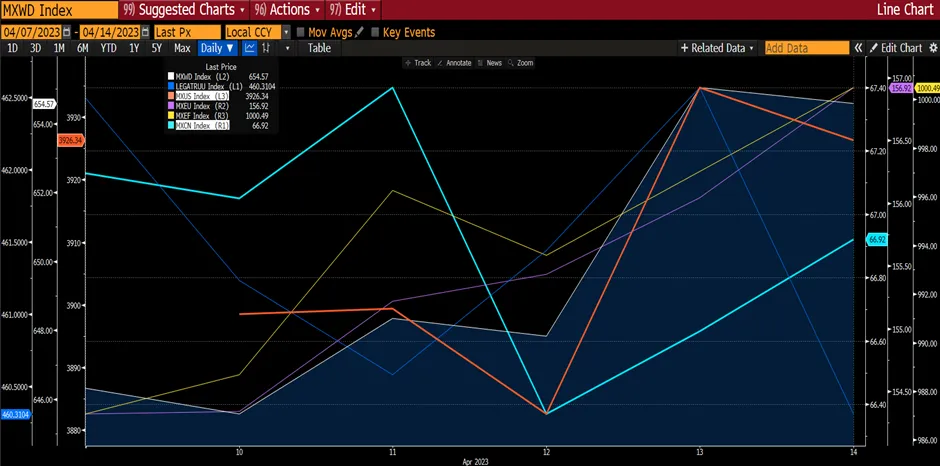

In a relatively quiet and short week, news flow is typically very light as investors take stock of the year that was ravaged by multiple headwinds. The market direction in the final trading week, some geopolitical developments, and the look ahead for 2023 predominated the news over the weekend. The major news that led to the mid-week uptick in the market was the announcement of China opening its borders on 8 Jan 2023. MXCN rose 1.35% but MXWD was flat the week at -0.3%. MXUS was relatively flat, declining by 0.10% while MXJP rose by 0.8%. Fixed Income Index (Total Aggregate) declined by 0.3%. For the full year, MXWD fell 18.4%, led by MXCN declining by 20.5% and MXUS falling by 19.8%. Fixed Income outperformed the global equity market as it fell by 15.6%.

Figure 1: Global Market Performances

Source: Bloomberg

Source: Bloomberg

Although China has seen a spike in Covid-19 cases (estimated 37m people possibly having been infected on a single day last week) following the easing of its Covid zero policy from 7 Dec, it further relaxes by scraping quarantine requirements for international travelers, starting from 8 Jan 2023. Hong Kong Daily quoted 3 sources from health authorities and hospitals in Guangdong, Fujian and Jiangsu provinces as saying they were asked by China’s National Health Commission to prepare for a downgrade in Covid-19 management levels, meaning lockdown, isolation and quarantine will no longer be required. Subsequently, the National Health Commission government released a statement confirming the chatter in the evening. At present, 5 days quarantine at a designated facility and three days of isolation at home are required for foreign arrivals. With effect from 8 Jan, travelers into China will only be required to obtain negative Covid test results within 48 hours of departure.

The government also said it will facilitate visa applications for foreigners who need to travel to China for everything from businesses to studies to family reunions, while outbound tourism, which dwindled to almost nothing during the pandemic, will resume. Current limits on the number of international flights between China and the rest of the world and passenger capacity will also be removed.

Following the announcement on 26 December, MXCN rose for 3 days before taking a breather on the fourth day by declining 0.4%.

While China may be reopening allowing Chinese to begin to travel, however, a slew of countries have imposed restrictions on Chinese traveling into their countries. For example, South Korea will require travelers to take Covid tests before and after they arrive from China and will limit short term visa issuance until the end of January and suspend any increases in flight from China. Italy has introduced a mandatory rapid Covid-19 test for all passengers entering the country from China, a move after authorities in Milan earlier said that almost half of the passengers on two flights from China tested positive for the virus. Most weren’t showing any symptoms. The US has also imposed airline passengers from China to show negative test results, regardless of their nationality or vaccination status. Other countries that either require a negative PCR test results or limit travelers from China are Taiwan, Japan, India and Singapore.

In China, the highly monitored data for China is the mobility figures that suggests economic activity is rebounding in several Chinese cities where Covid infections have likely peaked, although many parts of the country are still grappling with soaring cases and mobility is still far below levels reached a few months ago.

For example, the number of passengers using subways in Beijing, Chongqing, Chengdu and Wuhan rose about 40% to 100% in the week through 29 December 2022, a sign suggesting that residents in those areas are returning to work, shopping and restaurants once again. A measure of traffic congestion in those cities had increased about 150% to 240% over the period.

Improvements were seen in cities as per comments made from the Chinese Center for Disease Control and Prevention that infections have peaked in places like Beijing, Tianjin and Chengdu. The situation remains serious in Shanghai, Chongqing, Anhui, Hubei and Hunan. Subway and road usage in Shanghai, Shenzhen and Suzhou, had declined by 34% to 48% compared to a week ago and 34%-57% respectively. Residents appear to be homebound as fear of becoming infected sets in.

Air travel recovered ahead of the three days New Year public holiday. The number of daily domestic flights rose 50% by Friday from a week ago, although the volume is still 32% below 2019 level.

Figure 2: Subway Traffic

Figure 3: Traffic Congestion Index Rising For Some Cities

Figure 4: China Air Travel Activity Rebounds

In coclusion, as China continues to ease its covid restriction, activities in China will slowly but surely recover, despite an expected spike in Covid cases since the relaxation. Notwithstanding the rise in Covid cases in some cities, we see China’s economy being back on track for growth and would provide support to global economies (via stronger demand for commodities, tourist spending, manufacturing output etc). There should be pent up demand for travel after 3 years in isolation as well. Manufacturing activities, in our opinion, would also be returning, but may not be strong until after January-February (after Chinese New Year). From recent news, it appears that Chinese policymakers have shifted to refocus on growth and to accept the large Covid wave (Damn if I do. Damn if I don’t). Furthermore, Chinese policymakers have taken more decisive steps to ensure funding for major private property developers as well as broader policy easing for other sectors. Looking ahead into 2023, the China reopening and support for its housing debt crisis should be viewed positively as it would drive towards a better growth in 2023. Economists have been revising up their China 2023 GDP forecast up to as high as 5.8% from 2022 GDP growth of about 3%, reflecting the likelihood of a better year ahead.