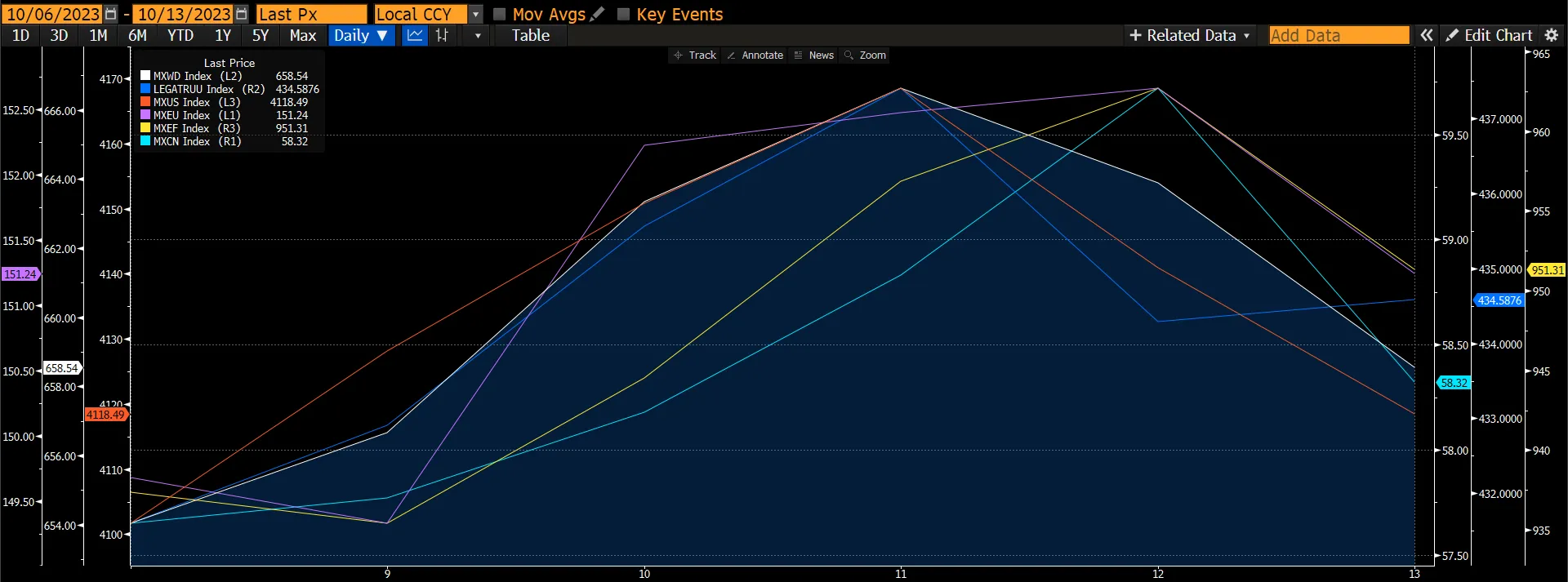

The global equities markets managed gains for the week from dovish comments from the Fed, despite losses in the latter part of the week stemming from pressures of higher oil prices and rising inflation expectations. Oil prices surged on fears the Israel-Hamas war could escalate geopolitical tensions in the Middle East while inflation expectations rose on the back of slightly higher than CPI in September the global equities markets rose 0.71% led by the Chinese market (+1.27%) while the US and European markets increased by a slower rate of 0.43% and 0.4% respectively. It appears that investors' attention remains sharply on global yields and inflation data. The global fixed-income market rose by 0.69% as investors’ sentiment turned risk-off and fled into fixed income. Additionally, several Federal Reserve policymakers suggested that the recent spike in yields may potentially negate the need for the Fed to tighten any further.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

Focus Topic – Impact Of Higher Rates For Longer

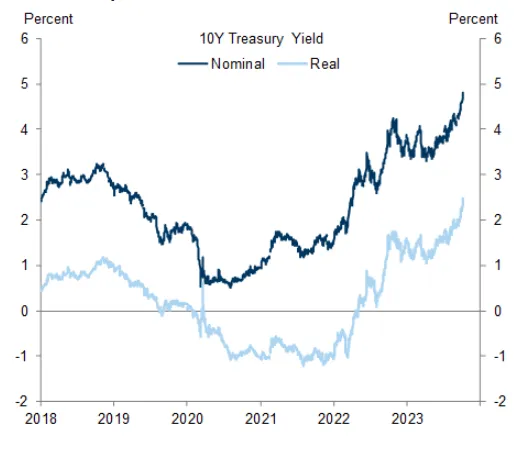

Interest rates have risen across the curve in recent months even as inflation has slowed, and the hiking cycle has increasingly looked finished. Both nominal and real 10-year yields are now well above the levels seen toward the end of the last cycle, and forward interest rates across the curve are around 2pp higher than in the pre-pandemic years. Font end rates have risen moderately, and it has become less clear whether falling inflation will be enough to prompt cuts anytime soon. Markets have become less confident that falling inflation will be enough to prompt cuts anytime soon as evident from the September FOMC meeting where some Fed officials now appear less convinced that rate cuts are necessary to avoid recession and less certain that the current policy rate is so restrictive.

Figure 2: Rising Interest Rates

Source: Federal Reserve Board

Source: Federal Reserve Board

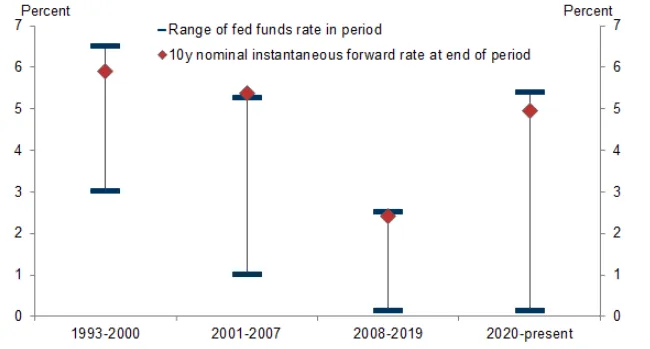

The much larger recent increase in interest rates further out the curve appears to have been driven mainly by investors inferring from the economy’s strong performance at 5%+ Fed funds rate that the equilibrium interest rate might be much higher than was widely assumed in the last cycle when markets embraced the secular stagnation hypothesis. Investors have been surprised by the economy’s resilience and have quickly reevaluated the level of interest rates that might be sustainable in the future.

Figure 3: The Rise in Forward Rates

Source: Federal Reserve Board

Source: Federal Reserve Board

The implication of the further tightening in financial conditions led by rising rates is the drag on GDP growth will last longer. However, US consumption has been resilient in 3Q complemented by encouraging employment growth and a recent upward revision in GDP forecast. There are still some concerns looming as the savings rate hovers near a decade-low. With the potential resumption of student loan repayments, younger demographics may find their disposable incomes strained. In the last cycle, the belief that real rates would remain close to zero in the future helped to rationalize a few major economic trends that would otherwise have looked more questionable such as elevated valuations of risky assets in financial markets, the survival of persistently unprofitable firms in the corporate sector, and wide deficits that added to an already historically large federal debt in the public sector.

Historically In financial markets where rates are rising, the key risk is that valuation measures that are benchmarked to interest rates would trend lower. This subsequently drives down price targets (rise in risk-free rates and higher cost of equity). Moreover, in the absence of much better growth in corporate profits, the significant increase in both nominal and real interest rates creates a much higher bar for equities to beat. The rise in PE ratios this year has, unusually, occurred despite a rapid rise in TIPS yields. At 4.3% risk-free and inflation-protected return makes equities look stretched unless there is significant growth. However, we believe the market has already somewhat repriced rate-sensitive assets significantly and the support would likely come from the resilience of the economy and job markets. In this case, we prefer quality companies that have a strong cash flow and balance to sustain their business expansionary plans.

Figure 4: Major Indices Are In A Wide Trading Range Since 2022

Source: Bloomberg

Source: Bloomberg

Since the start of 2022, equity markets have gone through several phases dominated by shifts in inflation and growth expectations. Nonetheless, while growth has held up much better than many investors feared at the start of the year, the rise in interest rates, at a time of stagnant profit growth, has resulted in a wide trading range. Equities in overall terms have made little progress at the broad index level. Yet, MXUS has risen by 15% while the global equity markets have increased by 10%.

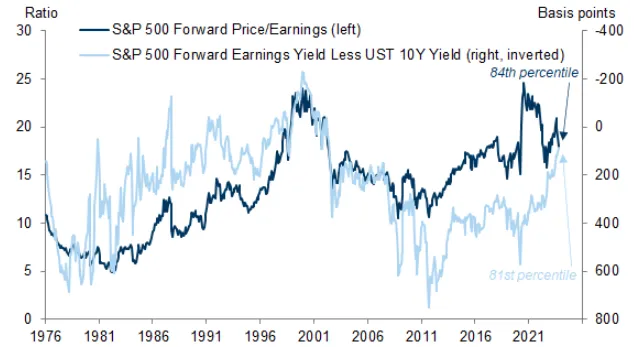

Figure 5: Divergence In Valuations and Yields

While the equity market looks much less stretched than during the technology bubble, many investors would likely have been surprised in 2019 if they were told that current valuations could prevail alongside the current level of interest rates. The gap between the forward earnings yield and the 10-year Treasury yield is now much higher than before the pandemic.

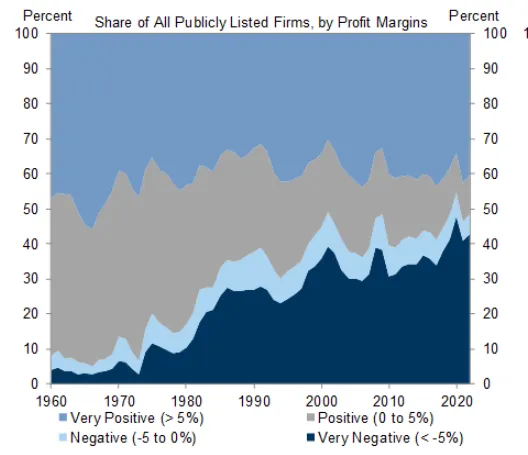

In the corporate sector, investors might hesitate to continue financing unprofitable companies that they hope will pay off well down the road now that the opportunity cost has risen. The number of unprofitable firms has risen in recent decades, reaching almost 50% of all publicly listed companies in 2022. The share of business activity that they account for is much smaller but still an economically meaningful 10% of total business revenues. Moreover, unprofitable firms account for about 13% of capital spending and employment, and even just the smaller group of persistently unprofitable firms account for about 5% of employment.

Higher funding costs could force some of these companies to cut labour costs or even close. Unprofitable firms tend to cut capital spending more aggressively when faced with margin pressure and cut labour costs more aggressively when hit with interest rate shocks. The larger risk is that some firms might simply have to close if their path to profitability is too distant. The exit rate of unprofitable firms is currently low by historical standards and has declined since the start of the pandemic, leaving it ample room to rise from here.

Figure 6: Unprofitable Firms Have Been Rising

Source: Compustat

Source: Compustat

In the public sector, projections of real interest expense and the federal debt-to-GDP ratio look much worse than before the pandemic, when the largest pandemic relief programs were already included in fiscal projections. According to Goldman Sachs, they project that federal interest expense as a percentage of GDP will surpass the early 1990s peak by 2025 and that the debt-to-GDP ratio will rise from 96% to 123% over the next decade. The higher interest rates will eventually add about 2% of GDP in real interest expense to the cost of stabilizing the debt-to-GDP ratio.

The above-mentioned risks are significant and collectively could trigger a deep recession when they occur abruptly and aggressively or simultaneously. If these risks were to materialize and add more meaningfully to the growth headwind, we believe the Fed would also likely deliver rate cuts that would offset some or all the impact. Thus, in this scenario, investors might well revise their expectations of future interest rates part of the way back down. Nevertheless, investors should be mindful of the risk and be selective. We like thematic sectors such as AI Generative, EV, and consumer discretionary along with stocks that possess growth and quality traits which would weather a deep recession and risk of closure. The fixed-income markets are closely following the Fed rhetoric and more odds are for additional rate hikes this year and less pronounced cuts in 2024. Shorter-term investment-grade bonds and shorter-term treasuries are the best options to combat potential rate hikes and limit interest rate risks.