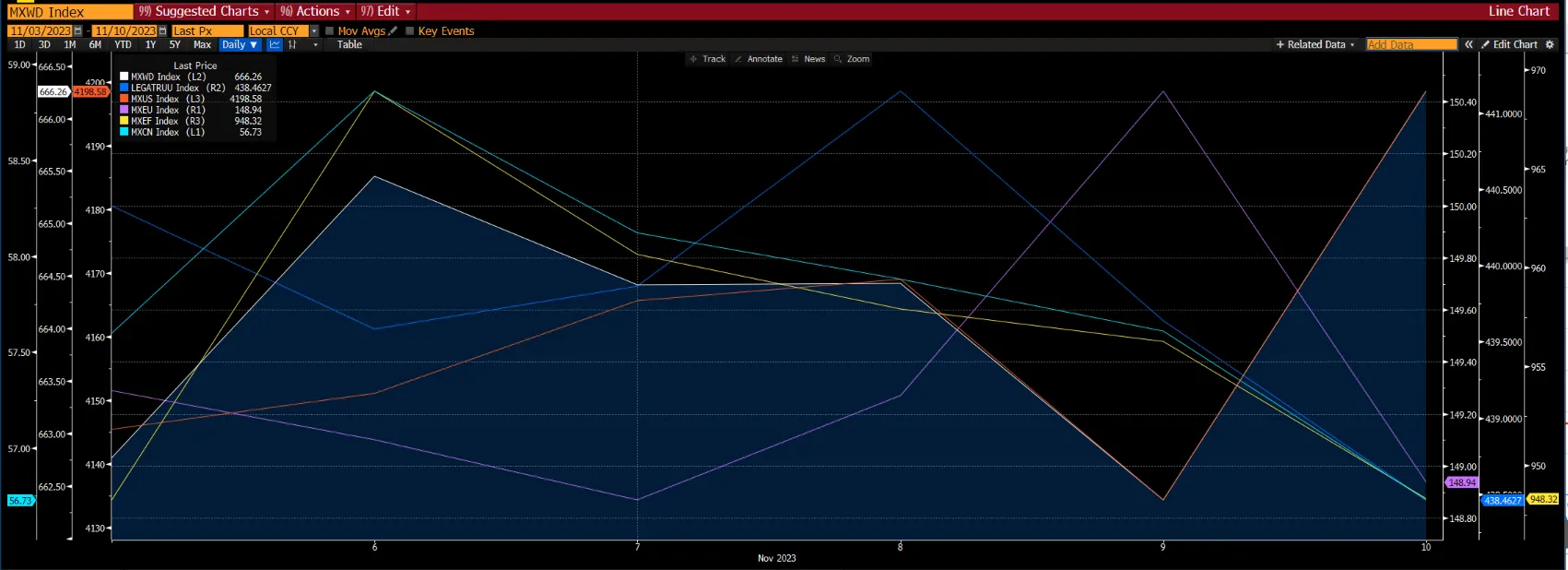

The global equities markets continue to rise on the back of the Fed’s dovish pause, a better-than-expected earnings season and the intensification of the Israel-Hamas war did not materialize. The global equities rose by 0.57% led by the US markets which increased by 1.33%. The European and the Chinese however fell by 0.73% and 1.34% respectively. The decline in the Chinese market was due to China’s headline CPI inflation turning negative again and import growth surprised to the upside, while export growth edged down in October. The global fixed-income index underperformed the global equities markets by declining 0.44% due to “risk on” sentiments as well as the 10-year US treasury rate rose to 4.6518% from 4.5724% in the previous week.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

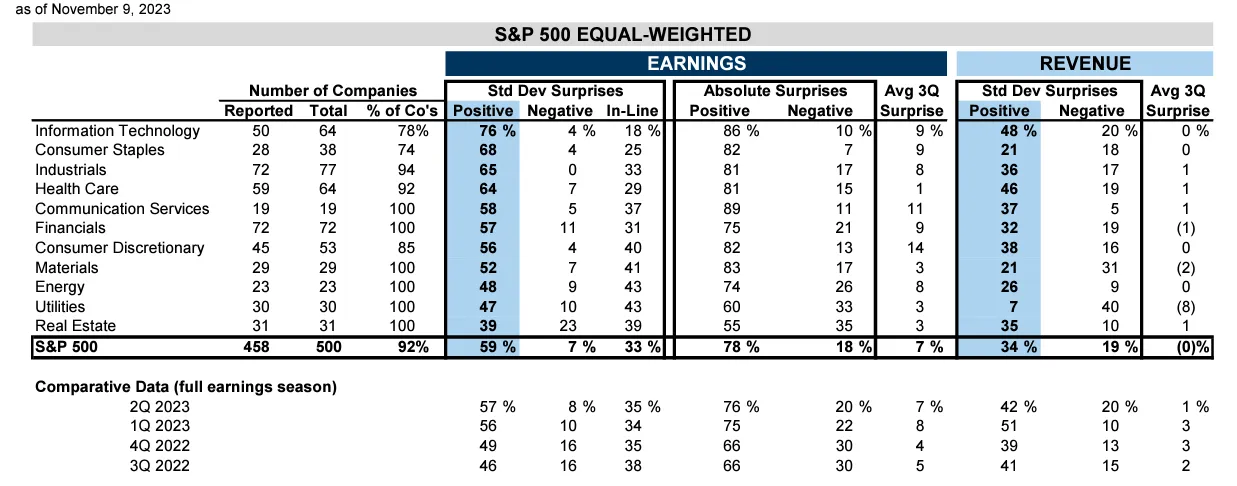

Topic in focus – Earnings Season Surprises On The Upside

The US equities ended their earnings recession. Over the past 6 weeks, 92% of the S&P 500 corporates have released their 3Q23 earnings. Companies in the S&P 500 3Q23 earnings results were stronger than expected and are on pace for positive quarterly earnings growth. This was the first quarter of 2023 where EPS YoY growth was seen since 3Q22. EPS grew by 4% or 10% excluding Energy driven by sequential margins improvement and 3% sales growth. 56% of the earnings announced positively surprised to the upside while only 9% were negatively surprised.

Figure 2: S&P 500 Earnings Results

Source: Factset

Source: Factset

The sequential quarterly improvement in profit margins represented the bright spot during the 3Q23 earnings season. Excluding the Energy sector, S&P 500 margins rose to 11.6% from 11.1% in 2Q23. These results are 40bps better than what analysts expected. Energy sector margins fell alongside Brent crude oil prices that averaged 12% below levels in 3Q22 ($86 vs. $97).

The most surprising beats came from the communication services and IT sectors while the largest disappointments were in the Real estate and utilities sectors. Nevertheless, the positive earnings growth and increased optimism that the US Federal Reserve will soon end its rate hiking cycle fueled a robust rally in the past two trading weeks. If the broad macroeconomic backdrop remains mostly benign, investors should be able to focus more on fundamentals, perhaps sustaining a classic Christmas rally into year-end.

Following the results, investors however remain concerned about negative consensus earnings revisions for 4Q23 and 2024. Estimates for 4Q23 EPS have fallen by 4% since the start of the fourth quarter. This contrasts with the pattern in 1Q23 and 2Q23, where one-quarter ahead estimates fell by 2% and rose by 0.2% during the respective earnings seasons. Full-year 2024 estimates have also fallen by about 1% since the start of earnings season.

The cuts to the 4Q23 EPS estimate since the end of September now suggest sequential margin contraction, once again setting a low bar for companies. Consensus forecasts currently imply that margins will decrease by 75bps sequentially and remain roughly flat on a YoY basis. Although seasonality could weigh on margins in 4Q23, stocks have consistently beat margin expectations in the first three quarters of the year and input cost pressures continue to ease.

With the bulk of the 3Q23 earnings season in the rear-view mirror, EPS is on track to grow by +1% YoY. Consensus is forecasting 2024 EPS growth of 5%. Looking ahead to 2024, 5% sales growth and modest margin expansion to achieve 5% EPS growth. If earnings continue to surprise on the upside and downward earnings revisions are muted, we believe earnings growth will continue to drive the market higher. Valuations should therefore be re-rated.

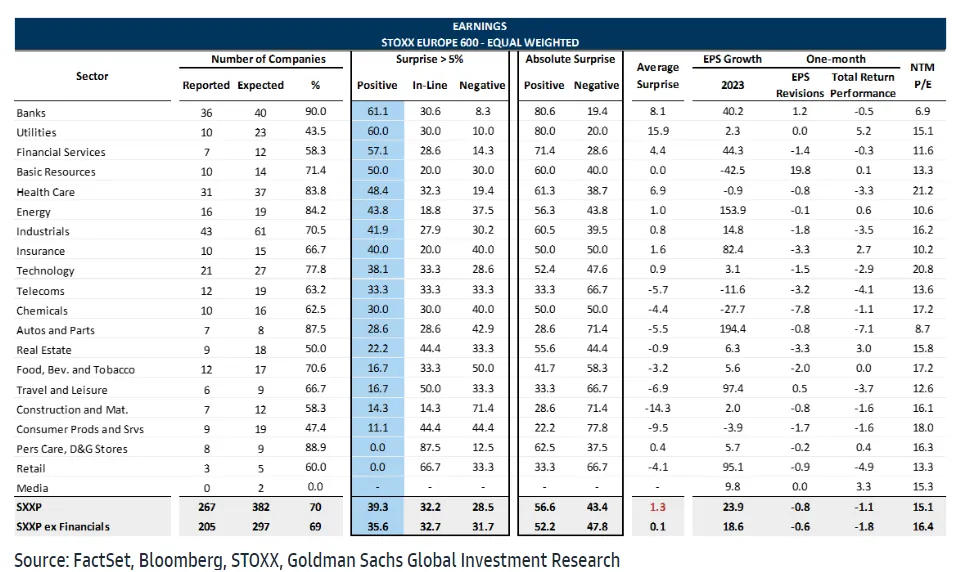

Figure 3: STOXX 600 Earnings Season

For the European markets, more than 75% of the STOXX 600 corporates have reported and so far, 3Q23 earnings have surprised by 1% to the upside. The market continues to penalize companies with negative surprises and 4Q23 earnings have been revised down by about 1%, with commodities and defensives seeing the largest downgrades this year. Investors have been rewarding companies that have been returning cash to shareholders rather than investing for growth. Since early July, companies returning the most cash to shareholders via dividends and buybacks have outpaced those stocks investing for growth by 8 pp (-5% vs. -13%).

Goldman Sachs’ European economists expect 2024 to be a better year primarily for three reasons. First, growth is expected to pick up as negative effects from a high gas price, the drag from ECB's tightening and modest growth headwinds abroad diminishes. Second, real disposable income is set for a notable boost as headline inflation slows and nominal wage growth remains elevated, which is likely to boost consumer spending throughout the year. Third, they forecast a more accommodative ECB policy setting and believe the negative credit drag will recede in 1H24. In addition, manufacturing growth would normalise even though the upside remains capped as the global industrial environment remains mixed. GS expects a 7% EPS growth in 2024 (after +3% in 2023) for STOXX 600 companies.

Shareholder returns (through dividends and buybacks) and acquisitions should remain a key theme for 2024. However, the main hurdle to return cash to shareholders will be the cost of debt. Refinancing rates are now more than double the current coupon rates of already-issued debt. We do not see a broad problem for the market given that aggregated balance sheets are not especially stretched. That said, debt and higher borrowing costs will likely prove a constraint for some companies, and we think this is under-appreciated by the market. Those companies with weak balance sheets and small caps are more at risk from high debt and higher borrowing costs than the market.