A data-driven week that kept the market fretting till Friday when the non-farm payroll and unemployment were released surprised the market. Investors were again concerned about a recession and waiting for guidance from the Fed about interest rates. MXWD recovered and fell just 0.34%, underperforming the Global Fixed Income market that rose 0.15%. MXUS dropped the most (by 0.75%), MXEU was flat (-0.04%) while MXEF and MXCN increased by 0.52% and 0.69%.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

The much-awaited rate hike on 3 May was widely expected. The FOMC raised the target range for the federal funds rate by 25bps to 5-5.25%. The FOMC hinted at a pause in the hiking cycle by removing “the committee anticipates that some additional policy firming may be appropriate” from the statement. However, the FOMC balanced that hint toward a June pause with a clear message that it retains a hawkish bias, noting that it would consider “the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments” in “determining the extent to which additional policy firming may be appropriate”.

The statement did not nod toward a June pause quite as strongly as the market expects. Specifically, it did not say that the current policy stance will most likely be sufficiently restrictive to return inflation to target. But putting together a statement that was acceptable to everyone when the range of views on the appropriate path forward is wide was likely difficult, and in retrospect, we sense that it will still be data driven going forward.

The FOMC also made it clear that it now sees the credit tightening as a fact rather than just a likely possibility, which adds to the case for a pause. Powell noted that credit conditions had already been tightening for a while before the recent banking turmoil began and tightened further once the recent strains emerged in the banking sector in March.

Figure 2: Fed Fund Rate vs CPI and Core CPI

Source: Bloomberg

Powell said that the credit tightening would weigh on economic activity and that its impact remains uncertain. When asked what the FOMC needs to see to conclude that its policy stance is sufficiently restrictive, he noted that the combination of real interest rates that are meaningfully above most estimates of neutral, the Fed’s balance sheet reduction, and the credit tightening add up to enough that “we may not be far off, or possibly even [are] at that level.” The post-meeting statement reiterated that, while the “banking system is sound and resilient,” “tighter credit conditions” are likely to weigh on economic activity, hiring and inflation, “though the extent of these effects “remain uncertain.”

Powell said that he does not expect a recession, unlike the Fed staff, and he made his statement so far that he thinks a soft landing is possible and finds the labour market rebalancing to date encouraging. If Powell thinks that a recession is not necessary to solve the inflation problem, he will be reluctant to deliver future hikes that he thinks would materially raise the risk of pushing the economy into a recession.

Specifically, Powell noted that supply and demand in the labour market are coming back into better balance, that surveys and other evidence points to gradual labour market cooling, that job openings have fallen sharply without unemployment rising, and that wage growth has been slowing down to a more sustainable rate. All of this, he said, makes it possible that “we can continue to have a cooling in the labour market without having the big increases in unemployment” seen in prior cycles.

That said, on Friday 5 May, the solid non-farm payroll and unemployment figures were released, and it excited the market and tempered fears of a recession with the thinking that the economy is growing well. NFPR rose 253k in April, exceeding consensus expectations for the thirteenth straight month, and an increase from the previous month of 236k. April payroll growth was once again strong in healthcare and social assistance (+77k) and business services (+43k) but slowed somewhat further in leisure and hospitality (+31k vs. 3-month average of 44k) perhaps due to tighter credit conditions in that bank-loan intensive sector. The unemployment rate declined 0.11pp to a new cycle low of 3.39%, reflecting a 139k increase in household employment and a 43k decline in the size of the labour force (labour force participation rate unchanged on a rounded basis at 62.6%). In our opinion, this would suggest that the labour market remains tight.

Figure 3: Treasuries Yield Surge

Although the European Central Bank delivered the smallest interest rate increase of 25bps, it is still in its battle with persistently strong inflation. And cited “We have more ground to cover, and we are not pausing.” President Christine Lagarde was “extremely clear” with her statement. Future decisions will remain data dependent as the aim is to bring rates to levels sufficiently restrictive to return inflation to the 2% target. The ECB also said it expects to halt reinvestments under its Asset Purchase Program as of July. The market reaction following the ECB’s decision to slow down to 25bps after three consecutive hikes of 50bps was a strong rally in the front end and some repricing (lower) of policy expectations. The ECB’s decision to terminate APP reinvestments surprised the market as a more gradual approach was expected. As a response, long-end rates edged higher while peripheral spreads widened.

Figure 4: ECB Interest Rate vs EU Inflation

Source: Bloomberg

MXCN edged up (+0.6%) while CSI300 was flat in a shortened trading week post Labour Day holiday boosted by a strong recovery of tourism and retail spending during the holiday, with domestic visitors and tourism revenue both exceeding 2019 levels. A total of 274m people travelled domestically during the 5-day Labour Day holiday period, representing 119% of 2019/21 daily run-rates, up from 89% during the CNY holidays. Tourism revenue reached RMB148b, +31% YoY or at 101% of pre-pandemic levels on a per-day basis. Spending and tourism have been trending higher since the reopening of China last year. We believe the trend would likely continue as the Chinese government continues to support domestic demand to spur the economy as well as recovery of corporate earnings.

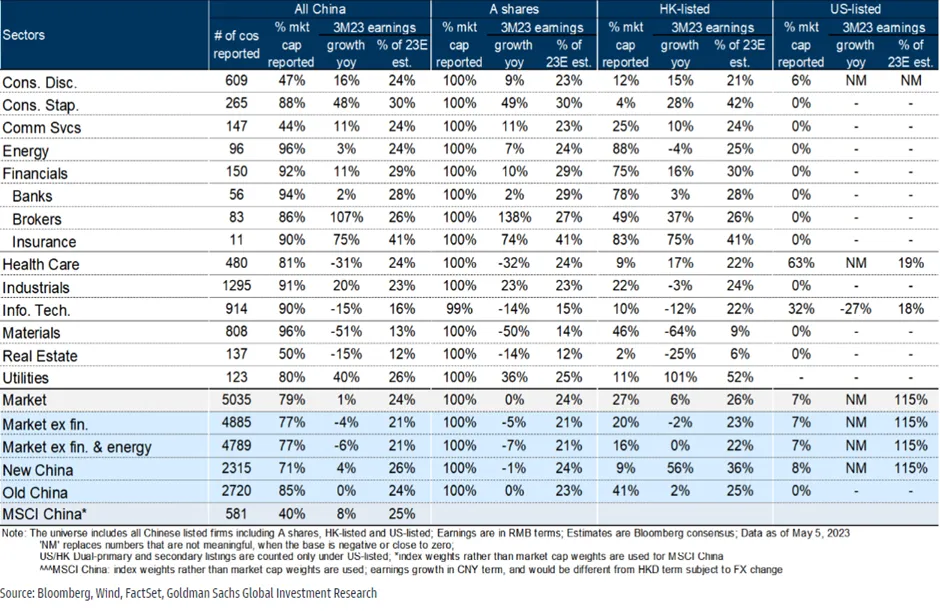

Thus far, 79% of all China-listed universe has reported 1Q23 earnings and this season has been uneventful with unexciting earnings growth of just 1%. The strongest YoY growth came from brokers and insurers which saw earning growth of 107% and 75% respectively. Consumer staples sector earnings grew by 48% while consumer discretionary rose by 16%. On the other hand, the materials and healthcare sectors disappointed with earnings declining by 51% and 31% respectively.

In summary, the US economy appears to be resilient with better-than-expected NFPR as well as the job market. From these data, concerns arise that the Fed may need to raise interest rates further at the next meeting. According to Jerome Powell, he believes recession, if any, would be a shallow one. The Eurozone, on the other hand, has clearly stated that it will continue to raise interest rates to fight the stubbornly high inflation rate. On the other side of the globe, while corporate earnings appear to be unexciting, tourism and consumer spending have been recovering nicely spurred on by the holiday season and government stimulus. We expect this trend to continue.

Figure 5: Total Domestic Trips and Tourism Revenue During Public Holidays

Source: Ministry of Culture and Tourism

Figure 6: Retail Revenue By Category

Figure 7: 1Q23 Earnings Season Report Card