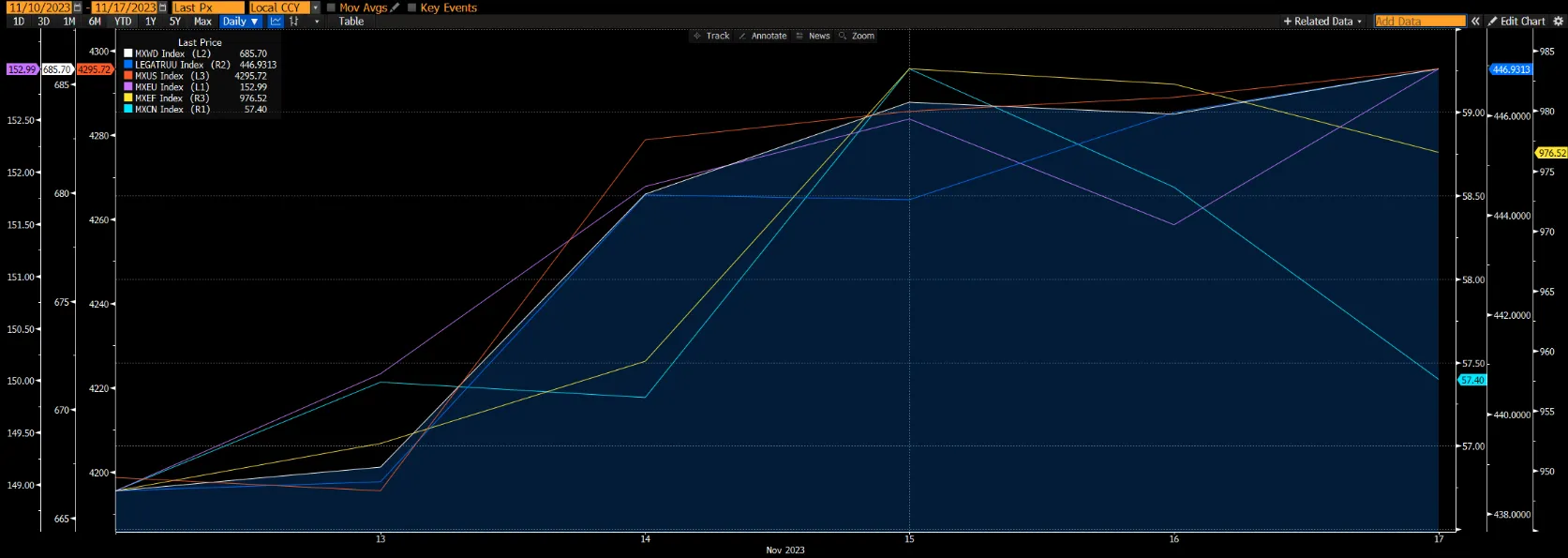

The global equities markets continue to rally by surging 2.99% for the third consecutive week driven by weaker-than-expected CPI, PPI and rising jobless claims. The 10-year treasury yields briefly traded at 4.379%, the lowest since Sept, falling from 4.65% in the previous week. The European markets surged by 4.81% while the emerging markets and the US markets increased, albeit at a slower pace, by 2.99% and 2.39% respectively. Despite China October's broad credit data and fixed asset investment being disappointing, while retail sales beat expectations and on-budget revenue improved, the Chinese markets increased by 1.36%. We believe this is partly because of some easing expectations regarding China’s geopolitical risks: President Biden-Xi meeting resulted in an agreement to restore military communications, and Xi pledged to take friendly steps to attract foreign investors. The fixed-income market rose 1.93% as yields fell on the optimism that the Fed has CPI under control. October’s drop in headline inflation to 3.2% from 3.7% in September was slightly better than expected and was driven by a continued fall in energy costs, plus easing of food and shelter prices.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

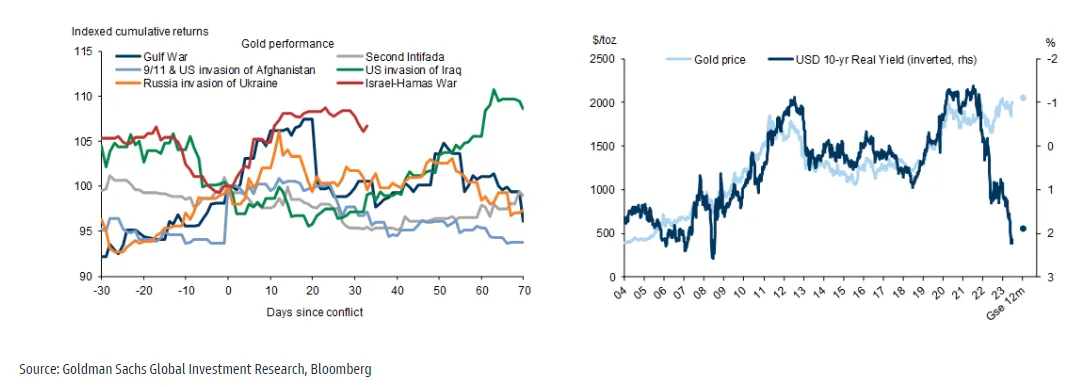

Topic in focus – Gold To Shine?

It is almost a foregone conclusion that gold benefits during tumultuous times given its status as a haven asset. Unsurprisingly, the recent escalation of Israel-Hamas tensions into a full-blown war boosted gold significantly, lifting spot prices almost 5% since 7 October (the inception of the latest flareup). What remains uncertain at this point is how much more and how much longer gold prices will continue to rally from here.

Figure 2: Gold Hedges Market Uncertainties

To a large extent, this would depend on how the conflict plays out – if it is contained and resolved within the next one to three months, then it is likely that the bulk of the rally is behind us. However, if the conflict spreads and becomes a destabilising force regionally, gold may yet have legs to run. Given the efforts by the US and its allies to contain the conflict, which include back-channel talks with Iran to warn against escalation, as well as the maintenance of a safe corridor open between Israel and north Gaza, our base case is that of a ring-fenced conflict rather than a regional crisis. On a more quantitative front, we analysed past risk-off incidents to see their effects on gold prices and found that such episodes resulted in a gold rally that lasted an average of 15 days (trough to peak) and resulted in an average increase in price of c.8.0%. Since the start of the Fed’s rate hiking cycle in March last year, interest rates and the dollar have been the primary headwind for gold. This makes sense as treasury yields represent the (risk-free) opportunity cost of holding noninterest-bearing gold. However, this relationship has been somewhat challenged in recent times; the inverse directionality between real rates and the gold price remains, but the downside sensitivity of the gold price (in response to a rise in rates) has diminished to some extent. From 1 June to 16 October, the 10Y inflation-indexed US Treasury yield, which is seen as a proxy for real rates, increased 58.8%, while gold receded just 1.5%. Even if we disregard the supportive effect of the Israel-Hamas conflict on gold, the point on reduced downside sensitivity remains valid – between 1 June to 6 October (just before tensions escalated in the Middle East), the 10Y yield increased 73.6%, while gold fell 7.3%. There are many reasons behind this phenomenon, but a key explanation is that markets are predicting a peak in rates in the near future and positioning themselves for it.

Rates although remain a risk, but the inflection point could be near. With US economic growth staying resilient, labour markets continuing to be tight, and inflation remaining sticky, the Fed is likely to keep the doors open for another hike in December. However, in the larger scheme of things, it appears that the US may soon be at an inflection point where the efficacy of high rates in cooling the economy and bringing about price stability is outweighed by the negative effects of US deficits and indebtedness. To illustrate how much US indebtedness has ballooned, gross interest payments on US debt have risen c.50% to c.USD970b within a year of the Fed’s first 25 bps hike in 2022. Net interest payments are projected by the Congressional Budget Office (CBO) to reach USD835b by 2025 (the deadline for the debt ceiling suspension), which ceteris paribus, would make this non-productive area of spending a larger component than other mandatory categories such as National Defense and Medicare. All this to say that the US will not be able to indiscriminately hike rates much further without running into massive fiscal deficits. The inference for gold is that further rate-driven downside, while possible, will likely be limited.

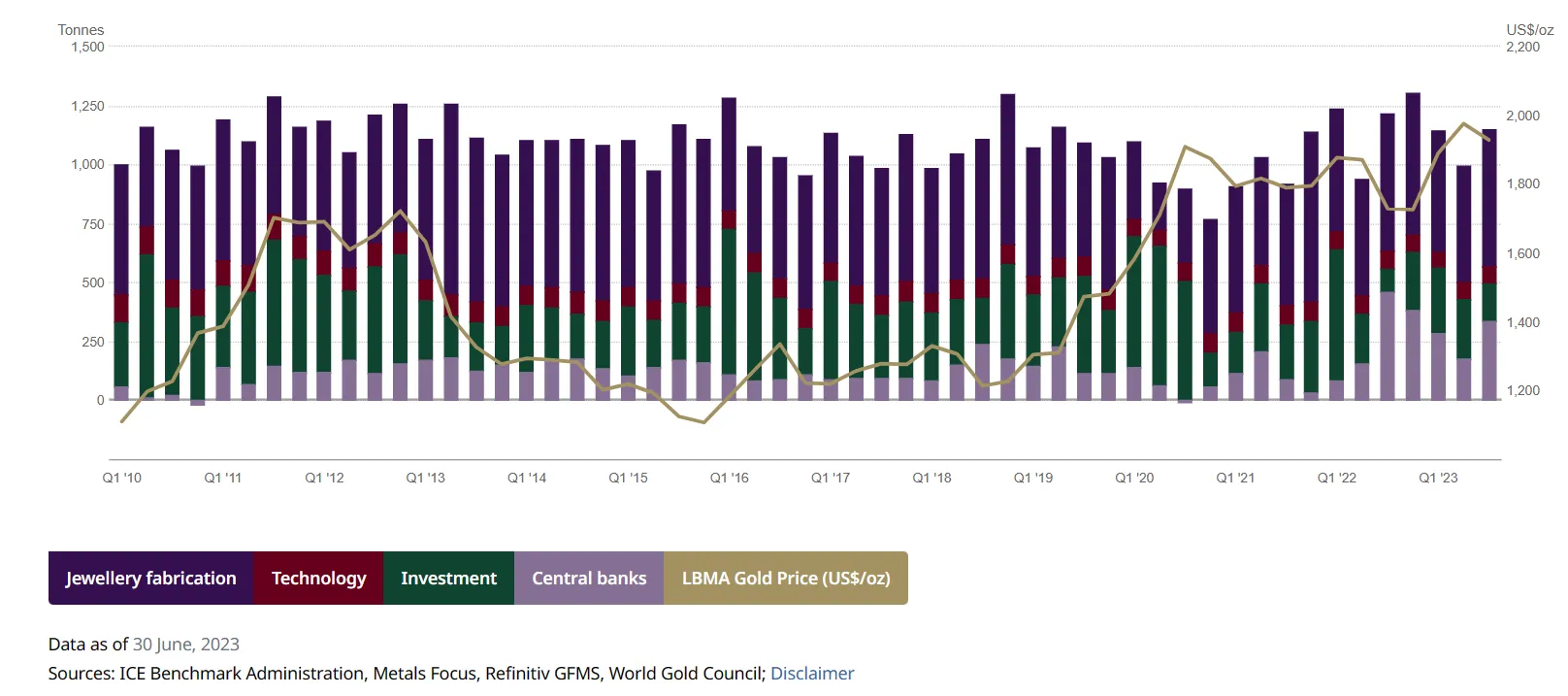

Figure 3: World Gold Demand

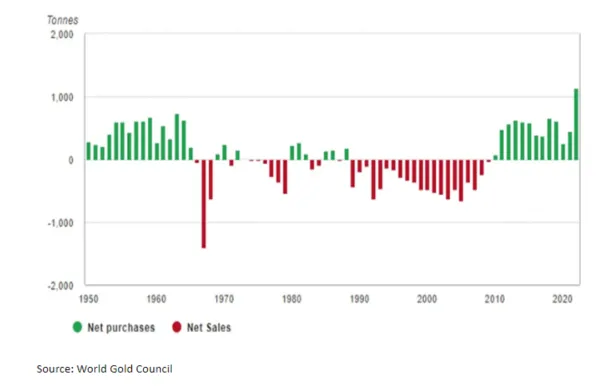

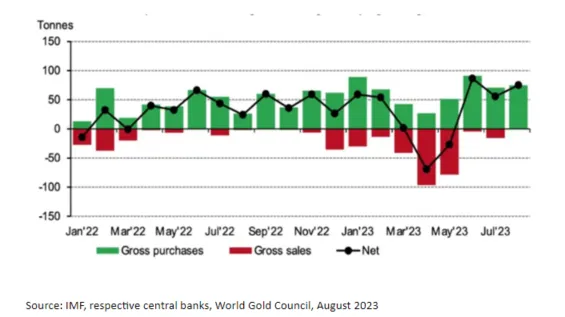

Additional tailwinds for gold can be found in central banking buying, which turned from net negative in April and May, to net positive in June, July, and August. The largest buyers remained the usual suspects with China, Poland, Turkey, Qatar, Singapore, and Czech Republic rounding out the buyer group for July. In particular, the PBOC has been extremely active in adding to its gold reserves, with its latest purchase of 29 tonnes in August stretching its buying spree to 10 consecutive months and a total purchase amount of 217 tonnes since last November. We believe this continued strength in central bank buying is part of a wider geopolitical trend that involves countries wanting to diversify their foreign exchange reserves and increase their holdings in neutral hard assets. This long-term trend should prove supportive of gold prices over the long run.

Figure 4: Central Bank Net Purchases/Sales of Gold Trend

Figure 5: Central Bank Demand For Gold Since 2022

Figure 6: Negative Correlation to USD

Source: Bloomberg

Source: Bloomberg

We would expect any selloff to be limited in scale due to a dovish Fed, slowing wage growth, weakening of USD, and resilient central bank purchases. Tactically, we would view a potential selloff in gold as a buying opportunity as we see an environment with elevated risk channels ahead playing into gold's hedge qualities. Goldman Sachs’ 12-month gold target is $2050/t oz (vs. current spot at c.$1991/t oz), suggesting a modest upside of just 2-3%.