The global equities market fell the most in a week since March due to central banks indicating that interest rates will move higher as well as fears of inflation and recession. Furthermore, geopolitical tension intensifies following President Biden calling President Xi a “dictator”. Despite a short trading week for the US and China, the global equities market fell by 2.21% as it was affected by the 3.2% and 3.59% decline in the European index (MXEU) and the Emerging Market index (MXEF) respectively. MXUS fell at a slower rate of 1.43% while MXCN plummeted 6.68% due to a rise in geopolitical tension and a lack of stimulus and policy easing measures to support the recovering economic growth. Because of the risk-off trades, the Global Fixed Income index fell by a mere 0.26%.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

In a surprising move, the Bank of England unexpectedly raised its benchmark interest rate by half a percentage point as it steps up its fight against the worst bout of inflation since the 1980s and warnings it may have to hike again. The nine-member Monetary Policy Committee voted 7-2 for an increase to 5%, the highest level in 15 years and the biggest move since February. Markets had priced in only a 40% chance of a 50bps hike, with most economists anticipating a quarter point.

Governor Andrew Bailey reiterated the earlier guidance pointing towards higher rates but said nothing to rein in market expectations for rates peaking around 6% by early next year, which would be the highest in over two decades. “The economy is doing better than expected, but inflation is still too high, and we have got to deal with it”. “We know this is hard – many people with mortgages or loans will be understandably worried about what this means for them. But if we don’t raise rates now, it could be worse later”.

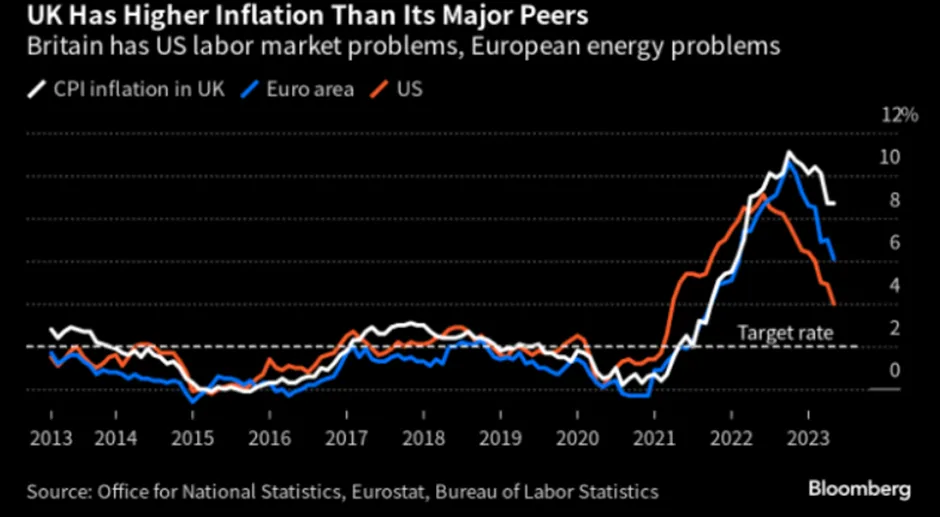

Figure 2: UK CPI Still Above 2% Target

Figure 3: UK Mortgage Rate Continues To Trend Higher

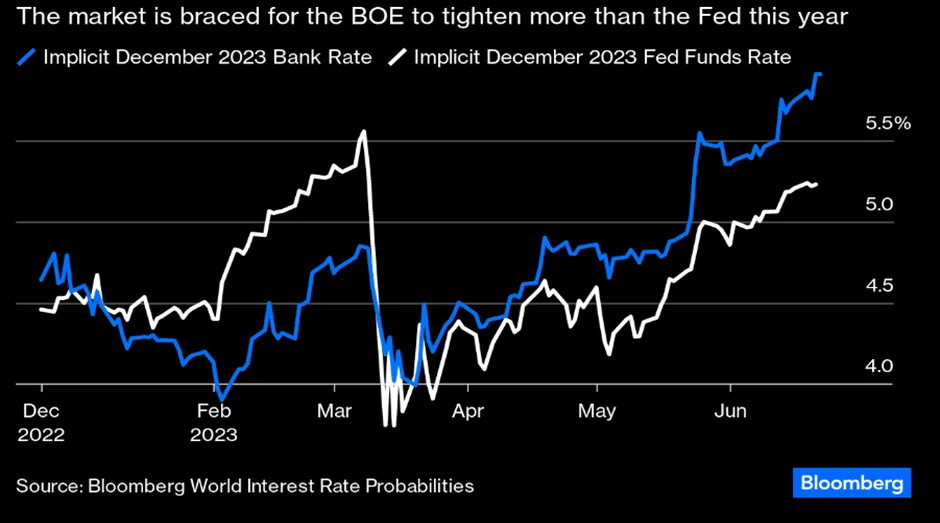

Figure 4: BOE Rates Will Surpass That Of Feds

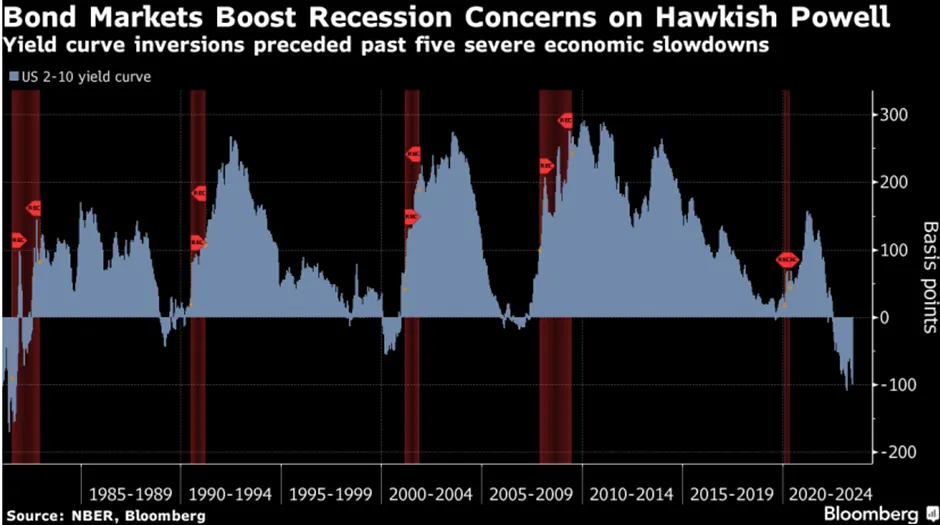

In the US, hard-landing fears re-established themselves amid the prospect of tighter policy, pushing the inversion of a key segment of the Treasury yield curve to a full percentage point for the first time since March. Jerome Powell underscored the need to tame inflation during his semi-annual report to Congress, saying two more rate hikes this year was “a pretty good guess”. In our opinion, this shouldn’t be a surprise as the announcement made last week has already alluded to the possibility of two more 25bps hikes to come.

Figure 5: Inverted Yield Curve

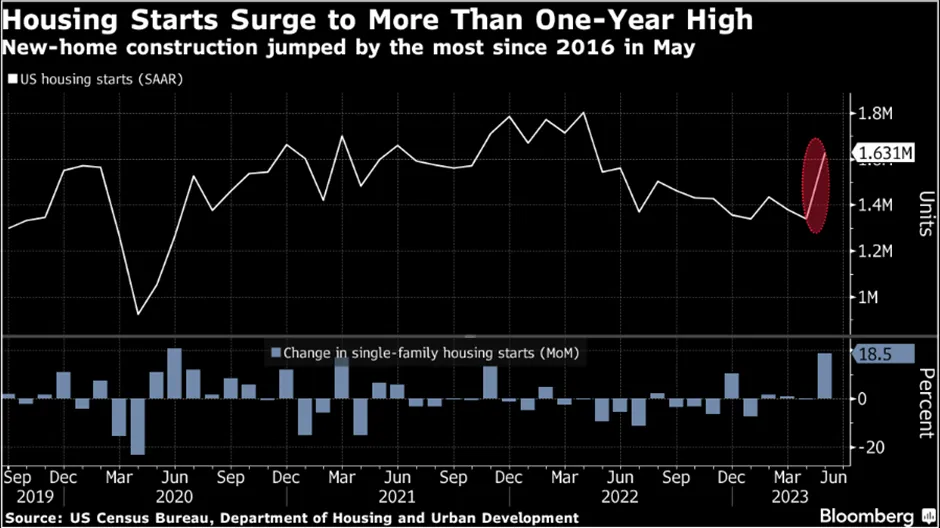

During an interview with Bloomberg, Treasury Secretary Janet Yellen said that she sees diminishing risk for the US to fall into recession and suggested that a slowdown in consumer spending may be the price to pay for finishing the campaign to contain inflation. Yellen said, “my odds of a US recession if anything, have gone down – because look at the resilience of the labour market, and inflation is coming down.” “I’m not going to say it’s not a risk, because the Fed is tightening policy”. Her remarks contrasted with rising recession concerns during the week and economic activity almost stalled in the Euro area, based on data compiled by S&P Global which subsequently sent stocks plugging while bonds surged as investors fled to safety amid heightened anxiety that aggressive central banks’ policy will tip economies into a downturn. However, business activity in the US expanded in early June at the slowest pace in 3 months, held back by a deeper contraction at factories. Nevertheless, the US economy has proven to be resilient with May’s employment report showing job gains beating all economists’ forecasts. Home construction and retail sales for last month have also shown surprising resilience in the face of the Fed’s monetary tightening.

Figure 6: Housing Start Rebounded Strongly

We would expect to see signs of slowing consumer spending as well as a higher unemployment rate before the Fed starts to pause its interest rate hike again later this year.

Separately, the tension between US-China, we believe has escalated once again. Following a candid discussion between US Secretary of State Antony Blinken and President Xi, according to China, US President Joe Biden made a “public political provocation” by referring to President Xi as a “dictator”. This isn’t the first time a seemingly unscripted Biden comment has complicated the relationship between the US and China. Chinese Foreign Minister spokeswoman Mao Ning called the US leader’s comments “irresponsible” at a press briefing. “It is against the basic facts and diplomatic protocols, seriously violates China’s political dignity, and amounts to public political provocation.” With such tension between the two countries, the Chinese market took it negatively and it partly contributed to the sharp decline of the week.

Figure 7: Retail Sales Still Rising Suggesting Willingness To Spend

Following cuts to China’s OMO 7-day reverse repo rate and MLF rate, PBOC cut 1-year and 5-year LPR by 10bps as well (20 June 2023), to guide effective lending rates lower, revive loan demand and facilitate economic growth. 1-year and 5-year LPRs are now at 3.55% and 4.20% respectively after this cut. This move was expected by the market but is disappointing for some forecasters who expected a deeper cut of at least 15bps to the 5-year LPR to boost sentiment in the property sector. We expect further policy easing measures to be announced in the next few weeks, especially on fiscal, housing, and consumption, although the magnitude of stimulus could be smaller than in previous easing cycles.

With regards to policy easing which the market is expecting are 1) further cuts in policy interest rates and one more RRR cut in 2H this year; 2) more fiscal measures such as acceleration of local government special bond issuance and additional policy bank support; 3) additional measures to consumption such as subsidies to home appliance and new energy vehicle purchases; and 4) further property policy easing such as cuts to downpayment ratios and mortgage rates and removal of home purchase restrictions in selected (mainly large) cities. That said, policymakers are now focusing on "high-quality growth" and emphasize the need for improving medium to long-term growth outlook, rather than only providing massive property and infrastructure stimulus solely for the sake of near-term growth. Policymakers are keen on stabilizing the property sector, but property policy easing has been constrained given the more challenging long-term demographic trend, the already elevated debt levels, and the “housing is for living in, not for speculation” mantra.

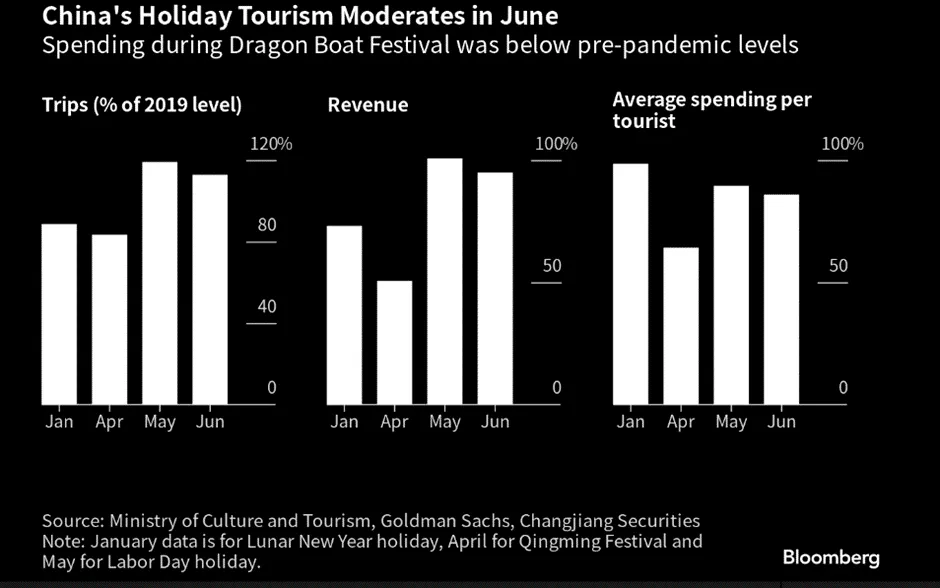

Investors are expecting more stimulus because China’s consumer-driven recovery is showing more signs of losing momentum as spending slows on everything from holiday travel to cars and homes. Domestic travel spending during the recent holiday for the dragon-boat festival was lower than pre-pandemic levels. Home sales figures were also below the level in previous years while estimates for June car sales showed a drop from a year ago. China’s economy is currently facing mounting evidence of a slowdown and several investment banks have downgraded their growth forecasts though most of them expect Beijing to still meet its relatively conservative target of around 5% this year. We believe it will take more stimulus and improvement in data for investors to regain confidence in China and thus in the near term, the Chinese market remains challenging. We are also seeing numerous brokers beginning to downgrade China’s economic growth forecast as well as rating in recent weeks.

Figure 8: China Holiday Spending

On the fixed income front, the week was more muted in terms of market-moving news except for the continued interest rate hike path by UK officials despite a pause by the Fed. The stubborn inflation has forced the Central Bank to act hawkishly. Riskier sectors within the fixed income spectrum like high-yield bonds and convertible bonds were the main detractors (-0.8% and -0.5%), whilst Treasury and IG corporates returned +0.2% over the week. Despite a negative performance this week, the Global Fixed Income index was partly supported by investors fleeing for safety.