A late rally helped the major indexes end flat to modestly higher for the week. The small-cap Russell 2000 Index outperformed the S&P 500 Index for the third time in the past four weeks, helping narrow its significant underperformance for the year-to-date period. Growth stocks built modestly on their lead over value shares, however. Within the S&P 500, energy stocks lagged as domestic oil prices fell below USD 70 per barrel for the first time since June.

Continuing enthusiasm over the potential of generative artificial intelligence (AI) appeared to be one factor in boosting the growth indexes and the technology-heavy Nasdaq Composite. Shares of Google parent Alphabet rose over 5% on Thursday after the company revealed its new AI model, Gemini, which can process text, code, audio, images, and video and can be incorporated into mobile applications. Meanwhile, Advanced Micro Devices rose nearly 10% on the same day after it announced the launch of a new generation of AI chips. Earlier in the week, Apple once again eclipsed USD 3 trillion in market capitalization and moved back near its summer all-time highs.

In local currency terms, the pan-European STOXX Europe 600 Index advanced for a fourth consecutive week, ending 1.30% higher. Stocks appeared to receive a lift from expectations that central banks could cut interest rate next year due to slowing inflation and signs that European economies have been faltering. Major stock indexes rose as well. France’s CAC 40 Index climbed 2.46%, Germany’s DAX gained 2.21%, and Italy’s FTSE MIB added 1.59%. The UK’s FTSE 100 Index tacked on 0.33%.

Japan’s stock markets lost ground over the week, with the Nikkei 225 Index falling 3.4% and the broader TOPIX Index down 2.4%. Comments by Bank of Japan (BoJ) officials stoked speculation that the central bank may abandon its policy of negative interest rates earlier than anticipated, weighing on riskier assets.

Chinese equities fell after a credit downgrade on China’s sovereign debt by Moody’s underscored worries about its economic outlook. The Shanghai Composite Index declined 2.05%, while the blue chip CSI 300 gave up 2.4% after falling midweek to its lowest level in nearly five years. In Hong Kong, the benchmark Hang Seng Index fell 2.95%, according to FactSet.

The data on job openings, in particular, seemed to drive a continued decrease in long-term interest rates over much of the week, with the yield on the benchmark 10-year U.S. Treasury note hitting an intraday low of 4.10% on Thursday. Yields rebounded in the wake of the payrolls report, however. The investment-grade corporate bond market weakened relative to Treasuries among softer tones in the beginning of the week. Issuance came in slightly above expectations, and about half of the issues were oversubscribed.

European government bond yields broadly ended lower as comments by some European Central Bank (ECB) policymakers fueled hopes that rate reductions could come sometime in the first half of 2024. The yield on the benchmark 10-year German bond slid toward its lowest levels so far this year. Italian government bond yields also declined. In the UK, the 10-year government bond yield fell to below 4% for the first time since mid-May on expectations that the Bank of England could start cutting borrowing costs by mid-2024.

Topic in focus – Korean equity perspectives for 2024

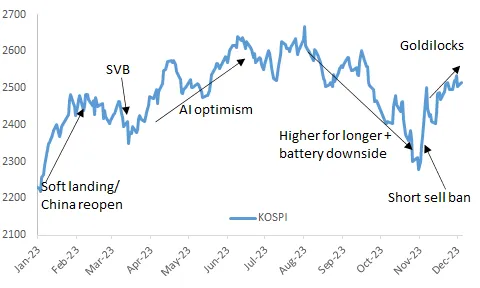

Korean equities (KOSPI) are on track to deliver double-digit returns in 2023, which would be the third-best year since 2011. Gains have been almost exclusively driven by the Tech sector, though, with all others underperforming. After a strong run in 1H23 (pricing in an anticipated earnings bottom and AI benefits), KOSPI stabilized over Jun-Aug 2023 (as earnings downgrades proved more protracted while AI upside continued) and witnessed a sharp decline in Sep-Oct 2023 (“higher for longer” pricing in the US and downside in battery material stocks) followed by an equally sharp rally in Nov 2023 (“goldilocks” pricing in the US + short-sell ban in Korea).

While an unusually deep cycle bottom is playing out right now, consensus estimates already build in a very robust recovery into 2024 and 2025 which the market has started pricing in this year already.

The key upside risks come from:

(1) if the US/global “goldilocks” macro conditions persist. Weak dollar should also prove a tailwind in this scenario.

(2) If a recovery in lithium prices and battery/material profitability arrives imminently, it may also help the market.

(3) Retail investors’ (who contribute ~60% of cash turnover) participation has fallen in 2H23 and they have turned net sellers in November. Should they return as buyers, this would help, in particular the Growth and Momentum stocks.

On the other hand, as a global-demand sensitive economy and market, Korea also faces downside risk from:

(1) a potential US recession in mid-2024. Taiwan and Korea are the two markets with the highest revenue exposure to US+EU.

(2) A return to “higher for longer” environment may resurface questions about higher refinancing risks and elevated debt levels in Korea.

(3) Another downside risk to consider is on earnings if memory price recovery is hampered by an inventory overhang.

Figure 1: KOSPI performance YTD and key drivers

Source: J.P. Morgan

Source: J.P. Morgan

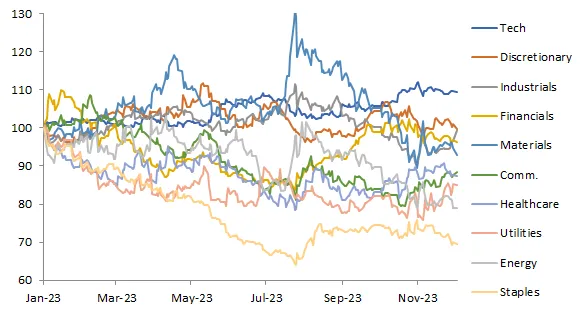

Figure 2: Korea sectors’ relative performance YTD

Source: Bloomberg

Source: Bloomberg

Fundamentals

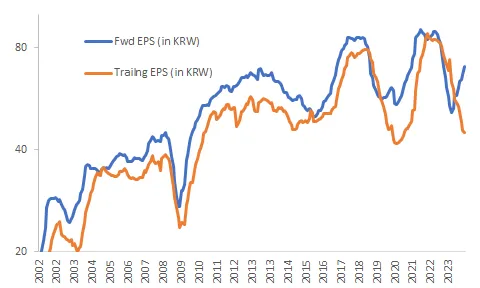

While the Korean market has always been the most cyclical in the region, EPS/margin swings in recent years have been unusually large and in the latest case misaligned with global demand growth (Korea as an export-heavy economy and market traditionally sees cycles aligned with global demand). Thus, trailing 12m EPS in Korea has now fallen by 48% from the peak in end-2021 (and is likely to fall further over 4Q). This is a larger decline than what was seen at the double-bottom low of 2018+COVID or the GFC. Notably, this has happened at a time when global growth has generally held up well over 2023.

Figure 3: Korea EPS was very cyclical in the past 10 years

Source: Bloomberg

Source: Bloomberg

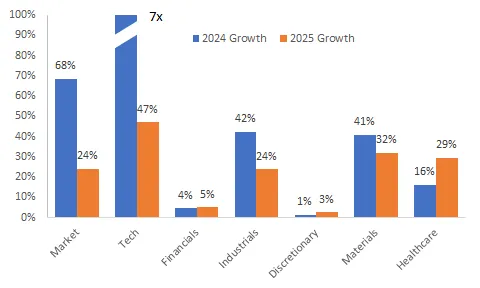

Consensus estimates currently expect 68% EPS growth for MSCI Korea in 2024 and 24% in 2025. The 2024E growth is largely driven by a 7x jump in Tech sector EPS. Industrials, Materials and Healthcare are also expected to contribute to earnings growth, while growth in Financials and Discretionary remains lackluster.

Figure 4: EPS growth estimates for key sectors

Source: J.P. Morgan

Source: J.P. Morgan

This is happening at a time when valuations do not leave a lot of cushion. On a price to trend-adjusted forward EPS multiple (particularly useful for cyclical markets like Korea), the market is currently trading at a 10.4x multiple, above the post-GFC average of 9.8x. Outside of the post-COVID surge, this is not very far from cyclical highs. Typically, cyclical markets and sectors trade at above-average multiples when earnings are in the upper half of the cycle. Looking by sector, valuations in the Tech sector look particularly elevated, with trend-adjusted valuations trading close to highs, leaving very little upside from here. On the other hand, Banks, Consumer sectors and Energy trade at extremely deep discounts to long-term averages.