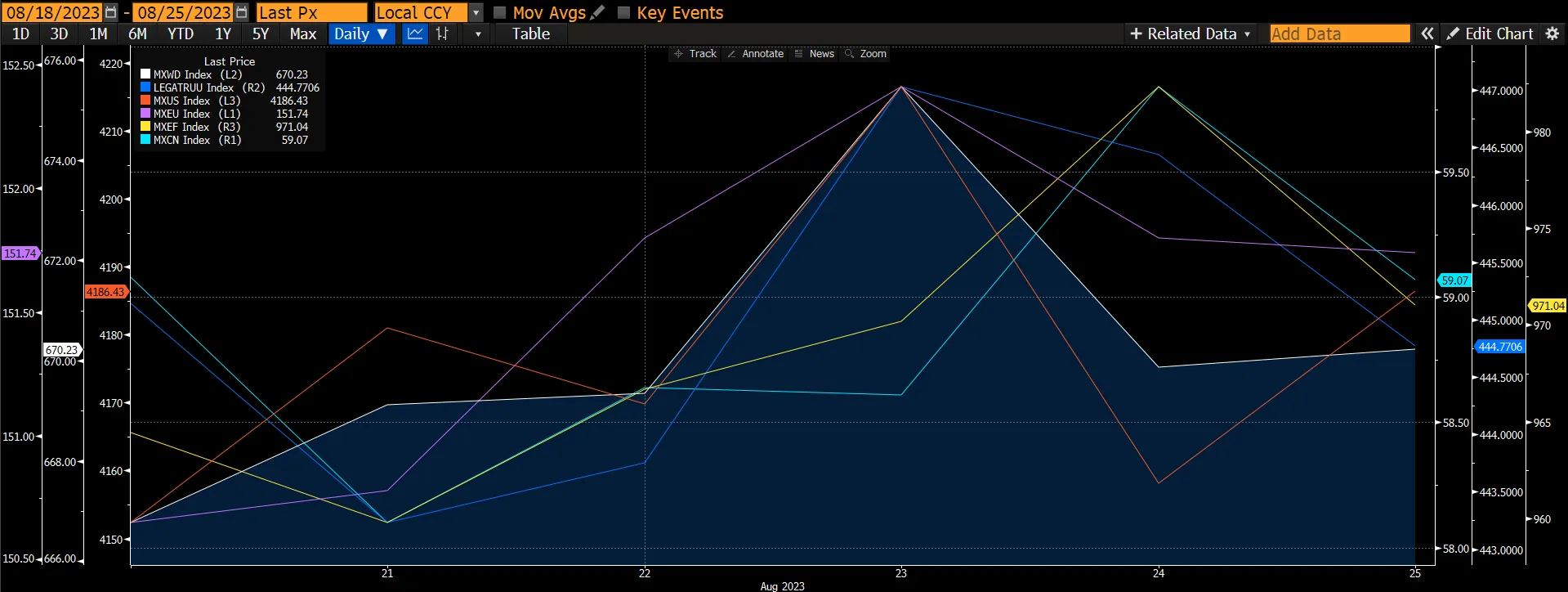

Markets rallied into the close on Friday after positive implications of a strong US economy, despite calls for data monitoring and potential further rate hikes from Jackson Hole to get inflation back to the Fed’s desired 2% target. The global equities market rose 0.54%, after 3 consecutive weeks of decline led by the US and emerging markets. The US market rose 0.84% while the emerging markets rose 0.74% despite the Chinese market declining by -0.14% on concern that the property sector, the financial system on the brink of collapsing, and smaller than expected cut in 1-year LPR (10bps) and left 5-year LPR unchanged. The global fixed income market was flat (-0.08%).

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

At the annual Jackson Hole symposium where the world’s top central bankers met stressed the need to keep interest rates high until inflation is contained and wrestle with deeper economic shifts. Speeches from Fed Chair Jerome Powell and ECB President Christine Lagarde laid out the challenges each is facing in deciding if they should extend historic strings of rate increases that began last year.

Fed Chair Powell’s speech noted that the FOMC will “proceed carefully” when deciding whether to hike or hold the policy rate constant at future meetings. Powell was slightly more hawkish than at the July press conference when characterizing the risks to the outlook, saying that the FOMC is “attentive to signs that the economy may not be cooling as expected.” Powell did not provide strong views on the neutral rate, instead noting that “we cannot identify with certainty the neutral rate of interest.” Furthermore, Powel in this speech, remained vague about whether the Fed could lift its benchmark rate again, though he warned that “additional evidence of persistently above-trend growth could put further progress on inflation at risk and could warrant further tightening of monetary policy.” Currently, the market is factoring in a 21% probability of a rate hike at the September meeting.

In ECB President Lagarde's address, she too stayed out of the debate over whether the ECB should lift interest rates for a 10th straight time in September. Lagarde restrained in laying out a clear path for the coming months merely citing “It’s critically important that inflation expectations remain anchored at 2%.” From the speech, we believe the ECB will set borrowing costs as high as needed and leave them there for as long as it takes to bring inflation back to its goal.

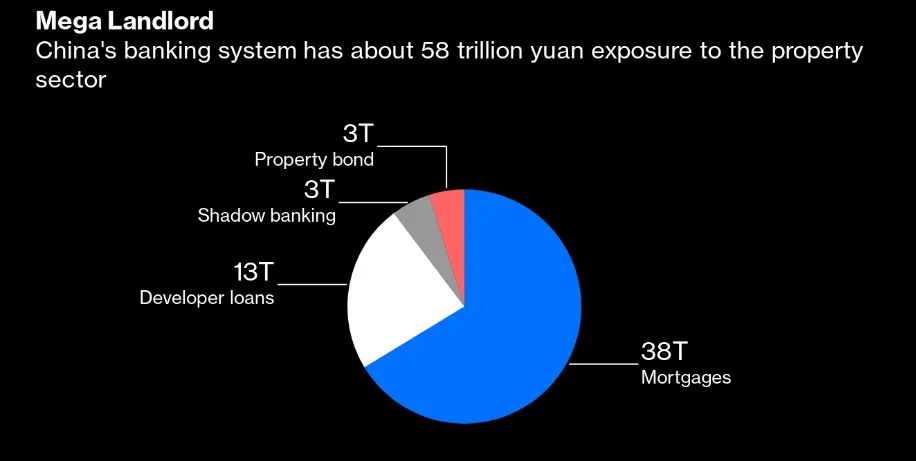

China's property sector once again took the limelight for the week and as a result, China’s financial system appears to be on the brink of collapse. Country Garden, once its biggest real estate developer, is slipping into default and one of the nation’s largest private wealth managers has been missing payments to investors. Meanwhile, distressed signals from regional governments, which rely heavily on land sales for fiscal income, keep on bubbling up. These events bring back memories of the 2008 subprime mortgage crisis that brought down Lehman Brothers. According to Goldman Sachs’ estimates, China’s banking system owns RMB94t ($12.9t) of local government debt, or 29% of total assets. On top of that, there is about RMB58t exposure to the real estate sector. Yes, the amount is alarming and concerning, in our opinion.

Figure 2: Chinese Banks' Exposure To Property Sector

Source: Goldman Sachs

Source: Goldman Sachs

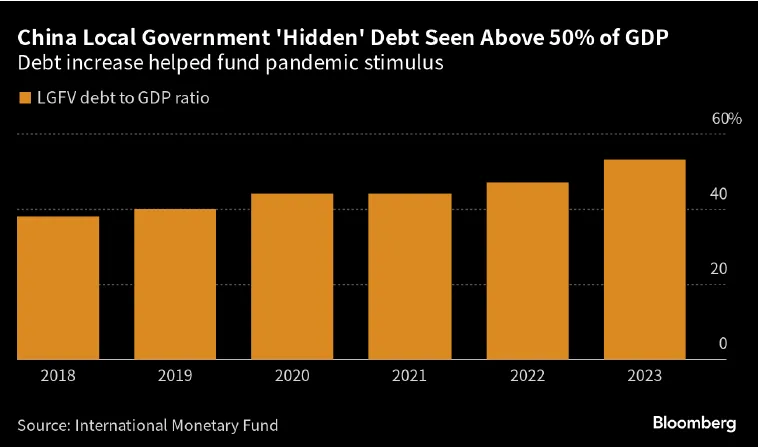

Property-related activities drive a large fraction of China's economic activity. Residential and non-residential activity together drove almost 18% of GDP in 2018; adding infrastructure spending and services related to real estate, the broader property/construction sector, and its upstream suppliers (ie. cement producers, etc) account for about 30% of GDP. Given its outsized share of economic activity, the downturn in the property sector over the past two years has weighed heavily on GDP growth. GS estimates that 10-15 years ago the property boom was contributing about 3pp to China's real GDP growth. This fell to 1-2pp in the years prior to the pandemic, and went sharply negative by 2022, after the implementation of credit controls began to significantly constrain activity. GS expects property-related activity to subtract 1.5pp from GDP growth this year and continue to drag on growth (albeit to a lesser extent) in the coming years.

Figure 3: LGFV Debt To GDP Ratio Has Risen

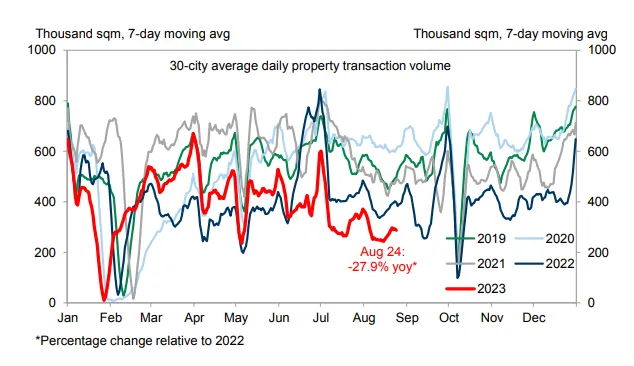

Figure 4: Property Sales Volume Remained Depress In August

Source: Wind, Goldman Sachs

Source: Wind, Goldman Sachs

In summary, for equities, we still prefer developed markets over emerging markets despite their cheaper valuations. One shouldn’t be buying into the market just because it is cheap (i.e. China). For the US, the probability of a recession has been declining, which is good news for growth. However, growth would slow and so could share prices. Thus, we suggest investing in good quality/value stocks and research would be key to shiv out companies with these traits. This would be similar for the European markets. For China, we remain cautious and selective at least until we see the announcement of a meaningful stimulus that would drive the resumption of economic growth. We see risks arising from the property and banking sectors capping any significant rally in the market.

US Treasury yields surged to the highest level since 2007, before easing. The 10-year Treasury yield reached its highest level since late 2007 as it rose to over 4.30% early in the week. Investors worried that the recent firm US economic data would delay the next Federal Reserve easing cycle until later. This week’s annual economic symposium in Jackson Hole will likely give more insight into the Fed’s stance, with the market expecting Chair Jerome Powell to reiterate the central bank’s focus on a steady but firm course for interest rates.

Last week’s publication of the Fed’s policy meeting minutes for July indicated worries from policymakers about continued signs of inflationary pressure in the economy. Market expectations for cuts in interest rates continued to be pushed out further into the future, with the Fed Funds rate showing that the first cut is now not expected until the early summer of 2024. The market went from pricing around a 37% chance of another rate hike at the start of the week to a 62% chance on Friday after Powell spoke. However, by the end of the week, bond yields had fallen back, largely owing to the weak PMI data, with the 10-year yield at 4.25%.

PMI data for August weakens. Purchasing Managers Index (PMI) data across the US, UK, and eurozone indicated that western countries continue to face a tough economic backdrop. August’s eurozone composite PMI fell to 47.0, its lowest level since November 2020. The equivalent figure in the UK was 47.9, the lowest since January 2021. It was also the first time the UK index had dipped below the 50.0 level – which separates economic expansion from contraction – for six months, driven by weaker trends in both manufacturing and services. In the US, the composite PMI remained above 50; however, its fall to 50.4 is the lowest level for six months and was below forecasts, with manufacturing notably weaker. The data contributed to lower bond yields over the week.

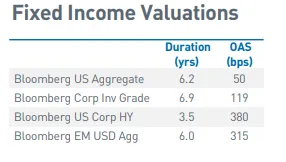

Investment grade corporates gained, rallying 0.61% for the week after four straight weeks of losses. The asset class outperformed similar-duration Treasuries by 41 bps.

High yield corporates also advanced, returning 0.41% for the week and beating similar-duration Treasuries by 51 bps. The backdrop of strong economic growth and higher rates is supportive for both high yield and loans, thanks to their lower duration and elevated credit risk compared to core fixed income asset classes.

Figure 5: Performance of the major bond classes

Source: RBS

Source: RBS

Emerging markets improved after recent underperformance, gaining 0.49% for the week and outpacing similar-duration Treasuries by 37 bps. The rally came despite continued sluggish growth data from China, where corporate profits were reported down -6.7% year-over-year in July. A survey of economists showed that consensus expectations for China’s full-year GDP growth have been marked down from 5.5% to 5.2% for this year.

With recent spread widening, both IG and HY corporate bonds look attractive value wise. Softened recession prospects and predictable Fed policy trims-off volatility in bond markets. However, within each sector, security selection is a key aspect in order to optimise credit and market risk of the portfolio.