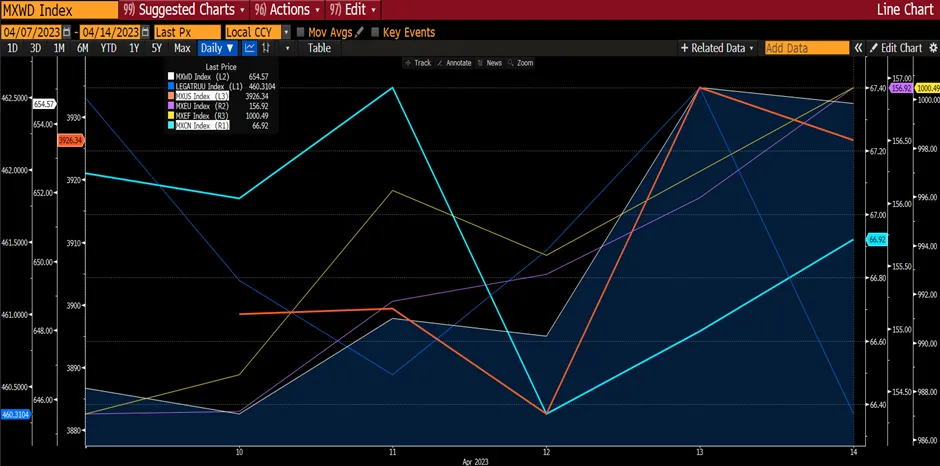

Market rallied this week on the back of China reopening and US inflation receding. Market rose despite comments made by 2 Federal Reserve Officials that rates need to be higher. Driving the global markets was North Asia (mainly China and Japan). MXWD rose 3.4% for the week while Global Aggregate Total Return (bonds) index rose by 1.9%. MXCN increased by 4.2% and MXJP surged by 5.1%, outperforming MXUS (+2.9%) and MXEU (+3.6%). USD however continued to weaken against the other currencies (1.6%).

Figure 1: Major Indices Movement For The Week

Source: Bloomberg

Source: Bloomberg

Two Federal Reserve officials said on Monday that the central bank will likely need to raise interest rates above 5% before pausing and holding for some time. “We are just going to have to hold our resolve” said Raphael Bostic, president of the Atlanta Fed. “Fed is committed to tackling high inflation and this warrants raising interest rates into a 5-5.25% range to squeeze excess demand out of the economy. Also he told reporters that the case for reducing the size of the Fed’s rate hikes to 25bps would be boosted if data due Thursday showed consumer prices cooling, following evidence that wage gains have also slowed.

San Francisco Fed President Mary Daly also said she expects the central bank to raise interest rates to somewhere above 5%, though the ultimate level is unclear and will be data dependent. “It is still too early to declare victory over persistent inflation”.

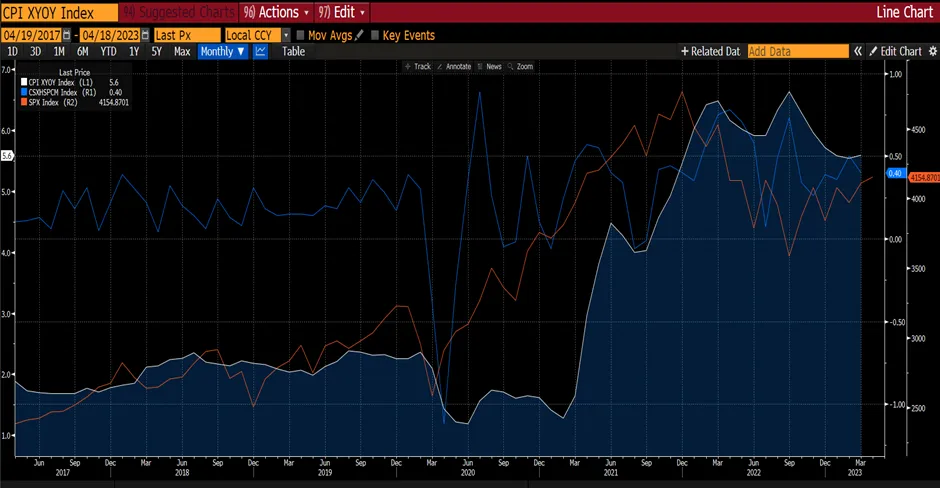

Figure 2: USD Weakens as Core Inflation Slows

Source: Bloomberg

Source: Bloomberg

Later in the week, the much-anticipated release of CPI data suggests that inflation is slowing and further rate hikes could be at a slower rate. December core CPI rose 0.3% MoM in line with consensus and the year on year fell another three tenths to 5.7%. Shelter categories surprisingly accelerated despite weakness in the new rental market, but wage-sensitive services categories were mixed, and used car and airfares contributed an outsized -0.15pp to the monthly core reading. Initial and continuing jobless claims declined against consensus expectations for increase. Following the release of the CPI report, we see the case for a step down to a 25bp rate hike in February.

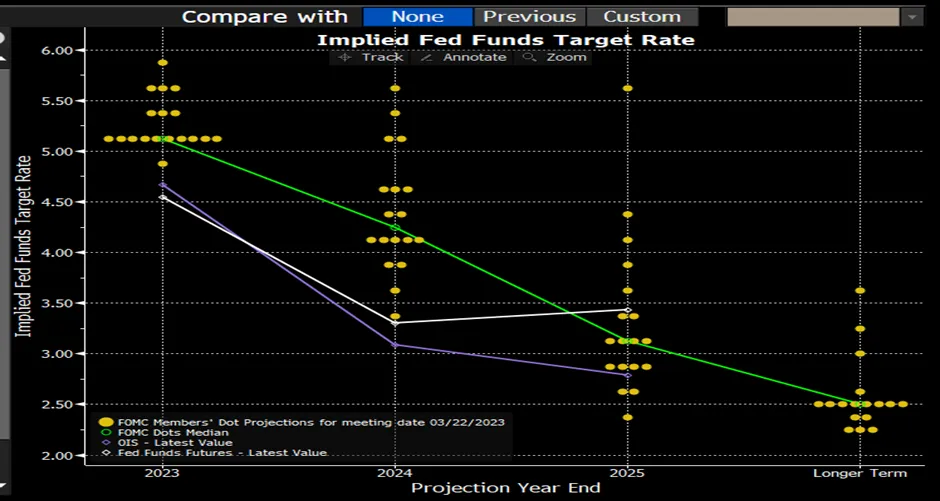

Figure 3: China CPI and Wage Grain Slowed

Meanwhile, deflationary pressure in China worsened in the fourth quarter as the economy slumped, with price-growth likely to be subdued even when the economy rebounds later this year, according to China Beige Book International. Companies recorded the weakest growth in wages and input costs in the final three months of 2022 since mid-2020. Growth in sale prices also slowed to the worst level since late 2020. “Short term disinflation is already here, with sales price growth slowing to a crawl” and “the Covid blow to retail could push this into deflation in the first quarter.”

Meanwhile, deflationary pressure in China worsened in the fourth quarter as the economy slumped, with price-growth likely to be subdued even when the economy rebounds later this year, according to China Beige Book International. Companies recorded the weakest growth in wages and input costs in the final three months of 2022 since mid-2020. Growth in sale prices also slowed to the worst level since late 2020. “Short term disinflation is already here, with sales price growth slowing to a crawl” and “the Covid blow to retail could push this into deflation in the first quarter.”

China consumer inflation slowed to 1.6% in November from 2.1% in the prior month as Covid disruptions suppressed demand, official data showed. Economists polled by Bloomberg expect full-year inflation to remain relatively subdued at 2.3% this year even as economic growth picks up. Inflation will likely return after the first quarter, but “will largely represent the making up of lost ground before fading,” CBBI said in the report. Any sustained and substantial price increases would require prolonged policy easing, while China still faces long-term deflationary pressures from demographic challenges. In addition, Chinese exports declined 9.9% YoY in December. Weak ex-China demand suggests that the bar is high for China reopening to add meaningfully to global inflation.

While signs of weakness in China’s economy continue for December and probably into January stemming from the bruised by Covid control measures in 2022, we believe the economy will improve as the impact from further relaxation of its Zero Covid policy fully kicks in. We are already beginning to see a pick-up in movement data and economists have continued to revise up their GDP targets. Furthermore, a rally in stocks of brokerages – usually an indicator of recovering sentiment in China – also shows that investors are putting more faith in the economic recovery amid a pivot to pro-growth policies, particularly the dismantling of Covid Zero. That makes the China surge more durable especially as global funds participate. According to Bloomberg, offshore investors have bought more than $2b of shares on Friday, the largest in two months. The influx of liquidity would likely continue and provide support to the market, which has risen by 52% since the beginning of November 2022.

We think China reopening and global economic recovery in 2024 will be prominent themes for 2023. North Asia is likely to lead after ASEAN and India strength last year as China markets rebound further and Korea anticipates semis' cycle recovery. Regional earnings growth is likely to accelerate to 14% in 2024 from 4% this year. Furthermore, as the reporting session begins, most regional companies will report CY4Q/2H22 earnings in late January to late March. This could possibly lead further downward earnings revisions and increases market volatility.