Stocks continued their weekly winning streak—the longest since 2017—as investors appeared to grow more assured that the economy would skirt a recession in the coming months. The S&P 500 Index briefly moved within 84 basis points (0.84 percentage points) of its all-time intraday high at the start of 2022, while the Nasdaq 100 Index and Dow Jones Industrial Average managed new records. Communication services stocks led the gains within the S&P 500, boosted by rises in Google parent Alphabet and Facebook parent Meta Platforms. Energy shares also outperformed as oil prices rose in response to worries over attacks on shipping in the Red Sea.

The week’s economic data arguably provided evidence that the economy was on its way to fulfilling the Fed’s twin goals of low inflation and low unemployment. On Friday, the Commerce Department reported that the core (less food and energy) personal consumption expenditures price (PCE) index, the Fed’s preferred inflation gauge, rose only 0.1% in November, while October’s increase was revised lower to the same level. The headline PCE index fell 0.1% in November, marking its first decline in 21 months, thanks to a sharp decline in goods prices. In local currency terms, the pan-European STOXX Europe 600 Index ticked 0.21% higher and stayed near its almost one-year high. Major continental stock indexes were softer to little changed. France’s CAC 40 Index lost 0.37%, Germany’s DAX declined 0.27%, and Italy’s FTSE MIB was down modestly. The UK’s FTSE 100 Index gained 1.60%.

In the UK, the FTSE 100 Index tacked on 0.3% and the FTSE 250 Index climbed 2.8%. The British pound strengthened versus the US dollar, ending the week at USD 1.27 for GBP, up from 1.25.

UK headline inflation slowed more than expected to 3.9% in the 12 months through November, from an annual rate of 4.6% in October, due to a drop in prices for motor fuels, recreation, culture, and food. Underlying price pressures measured by core and services inflation eased, coming in at 5.1% and 6.3%, respectively, but were still above the Bank of England’s 2% inflation target. Revisions to gross domestic product (GDP) by the Office for National Statistics indicated that the economy performed worse than previously thought in recent quarters. GDP was lowered from 0.2% to flat in the April to June period, while the final estimate for the third quarter showed that the economy shrank 0.1%.

Japan’s stock markets registered modest gains over the week, with the Nikkei 225 Index rising 0.6% and the broader TOPIX Index up 0.2%, supported by a dovish Bank of Japan (BoJ). As widely anticipated, the central bank retained its ultra-accommodative monetary policy stance, including forward guidance, at its December meeting. It refrained from making comments about possible policy tweaks next year, appearing to push back against market expectations of a near-term interest rate hike.

Against the backdrop of the dovish BoJ, the yield on the 10-year Japanese government bond (JGB) fell to 0.62% from 0.70% at the end of the previous week. While the yen initially weakened, it finished the week broadly unchanged at the low end of the JPY 142 range against the U.S. dollar.

Stocks in China declined after the government announced new restrictions on the gaming sector. The Shanghai Composite Index gave up 0.94% while the blue chip CSI 300 fell 0.13%, its sixth weekly decline and capping its longest losing streak since January 2012, according to Bloomberg. In Hong Kong, the benchmark Hang Seng Index lost 2.69%, according to FactSet.

Topic of the week – Thailand equity outlook

Political uncertainties, a slow recovery of China tourists, and weakening global demand have weighed on Thai equities in 2023, driving more than US$5.5 billion of equity outflows from the market. That said, there is a better upside/risk trade-off for Thailand in 2024, driven by fiscal easing, a continuing tourism recovery, THB appreciation and the light positions of foreign investors. Thailand as offering a rare combination of resilient GDP growth and a sizable current account surplus, which should provide an offset to global headwinds. Additionally, potential rate cuts by the Fed could create tailwinds for risky assets, driven by multiple re-rating.

The government has embarked on a Bt600bn stimulus (3.5% of GDP, 6% of private consumption) to be financed through borrowing. There are signs of tourist arrivals picking up further in 2024, led by European, South Asia and Korean tourists. The government has also lent its full policy support to the industry by announcing 5mn-6mn temporary visa waivers for Chinese and Indian tourists. Thailand’s market share of outbound Chinese tourists (ex HK SAR/Macau SAR) continued to recover in 2023 despite concerns.

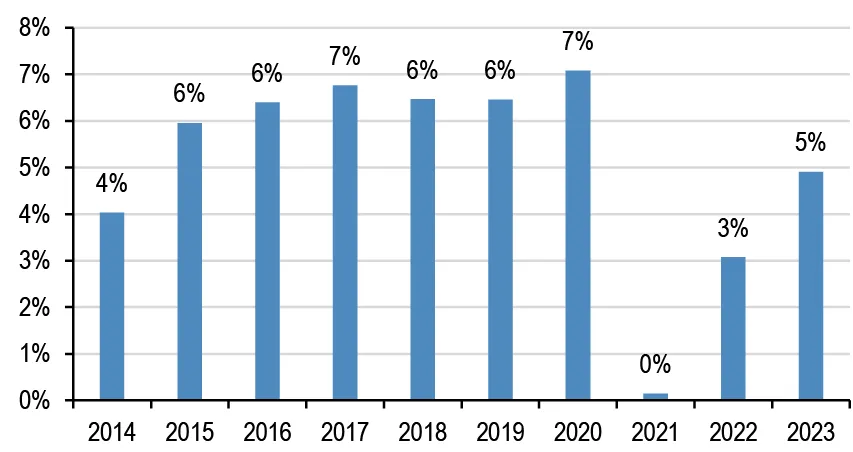

Figure 1. Thailand market share of outbound Chinese tourists

Source: Bloomberg

Source: Bloomberg

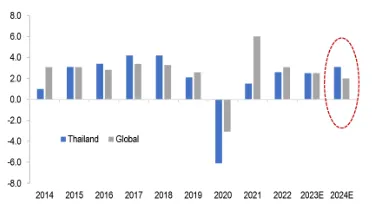

Figure 2. Thailand GDP growth to exceed global growth for the first time since 2018

Source: J.P. Morgan

Source: J.P. Morgan

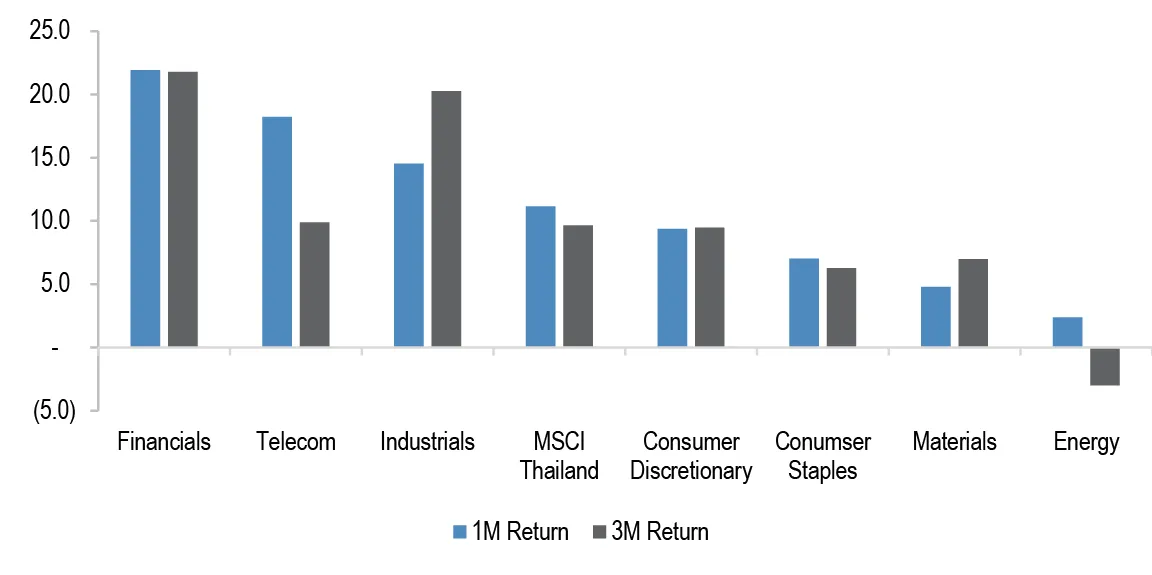

Figure 3. Thailand’s sector returns after Fed cut (%)

Source: J.P. Morgan

Source: J.P. Morgan

Key themes for 2024

First, it is recommended that investors position for stocks that can benefit from the energy transition in ASEAN, as governments need to ramp up the share of renewable energy usage to keep up with net-zero targets and avoid punitive tariffs from the EU. High dependence on fossil fuel would pressure governments to accelerate wind/solar project build-outs. Stock beneficiaries for Thailand in this space would be electricity operators with a high mix of renewables (GPSC, BGRIM), and battery materials (IVL).

Second, there is growth-compounding opportunities in the hospital sector. Medical spending per capita is still in the low range for Vietnam, Philippines and Indonesia, while Thailand and Malaysia lag other middle-income peers. In addition, cost remains the key competitive advantage to attracting medical tourism for Malaysia, with the cost of several typical treatments considerably lower than in developed countries.

Third, it is believed that the deepening of the semiconductor and EV value chain in ASEAN will lead to the long-term growth of the manufacturing sector and generate compounding impacts on technological advancement, income growth, and infrastructure development. Key long-term beneficiaries of this trend in Thailand are leading hardware producers (HANA, DELTA, KCE).