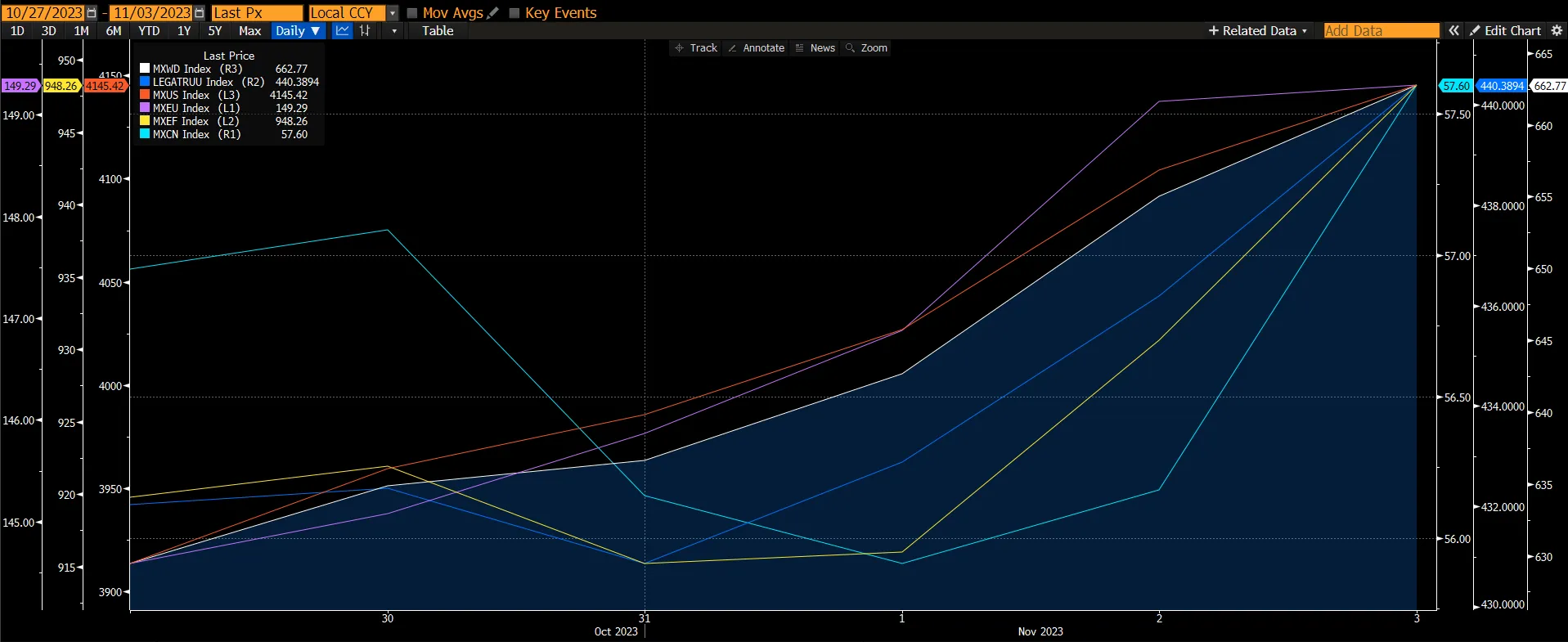

The global equities market recovered strongly following a “dovish pause” by the Feds, slower-than-expected job growth (150k vs estimates of 170k), and this earnings season brought more surprises than disappointment. The global equities market surged by 5.3% led by the US and European markets which increased by 5.96% and 4.79% respectively. Despite poor PMI data out of China that indicated softer domestic demand, the Chinese market rose 1.12%. US Treasury yields declined both before and after the Fed’s policy meeting, at which policymakers decided to keep interest rates at the same level. The two-year Treasury yield fell back below 5%, while the 10-year declined to 4.67%. The Fed’s decision encouraged the belief among some investors that rates are already at peak levels. As a result, the global fixed-income market rose by 1.93%.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

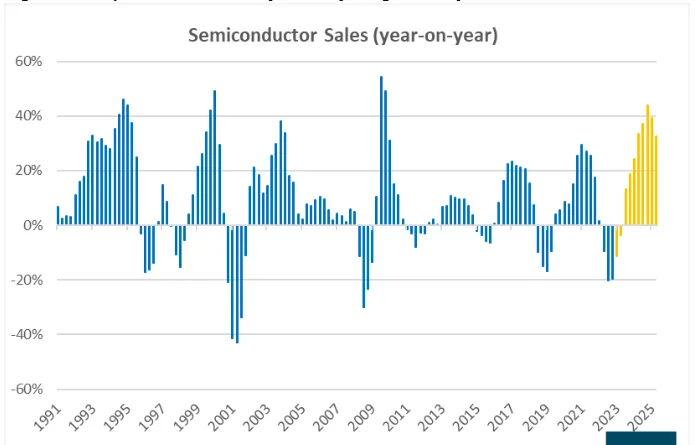

Topics On Focus – Expecting The Chip Industry To Turnaround

The semiconductor industry has been mired in a downturn since 4Q22 as chip sales plunged by nearly 10% YoY, the first decline since 2019. The slump further worsened as the rate of decline rose to 20% in 2Q23. This comes as many chipmakers warned of falling demand and rising inventories, a trend that could likely persist for the rest of this year.

Figure 2: Semiconductor Sales

Source: Bloomberg, SIA

Source: Bloomberg, SIA

However, we believe growth will return in 2024 underpinned by chipmakers seeing a massive structural increase in demand as the world becomes increasingly digitalised, leading to more semiconductor applications, and higher silicon content. Furthermore, the industry will be grappling with the rapid adoption of AI, which requires highly advanced processors that are capable of handling huge, complex workloads efficiently. AI’s revenue potential is projected to proliferate over the next decade.

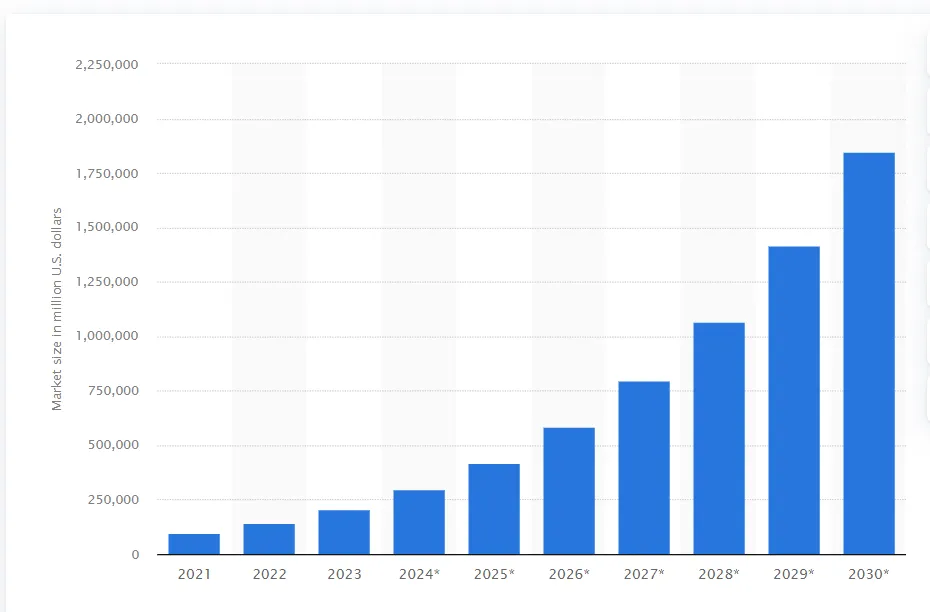

According to Nex Move Strategy Consulting, the market for artificial intelligence (AI) value of nearly US$100 billion is expected to grow twentyfold by 2030, up to nearly US$2 trillion. The AI market covers a vast number of industries. Everything from supply chains, marketing, product making, research, analysis, and more are fields that will in some aspect adopt artificial intelligence within their business structures. Chatbots, image-generating AI, and mobile applications are all among the major trends in improving AI in the coming years.

Figure 3: AI Market Size

Source: STATISTA 2023

Source: STATISTA 2023

Over the past 2 months, many chipmakers have upgraded their outlook for 2024 as the generative AI frenzy took the world by storm following the launch of ChatGPT in late 2022. However, AI will not be only the key driver for the semiconductor industry, but we believe it will grow at a faster rate compared to the handset, PC, etc. Anecdotal evidence from this recent reporting season is

-

TSMC - Management delivered a positive message citing an incoming end of the inventory correction with early signs of demand stabilization for PCs and smartphones. Overall inventory level is expected to continue decreasing into 4Q23 and TSMC now expects a healthy growth outlook for 2024.

-

Samsung Electronics - Like Hynix’s earnings call, many analysts came out incrementally positive on the company's fundamentals, with a solid outlook on HBM confirmed, pricing upcycle for both DRAM and NAND just beginning, memory inventory accelerating its decline after peaking out in May, and smartphone shipment expected to rebound next year.

-

Intel – Intel delivered a strong beat and raised its 3Q/4Q revenues, benefitting from cyclical headwinds abating across end markets in addition to its own impressive operational execution. Also, the gross margin outlook came in better than the street anticipated along with OPEX discipline.

-

Qualcomm – The company gave a revenue forecast for the current quarter that indicates the mobile-phone industry inventory glut may finally be receding. According to its CFO, “We have seen stabilization in the market”. Some of that improvement stems from customers building up their inventory to a normal level.

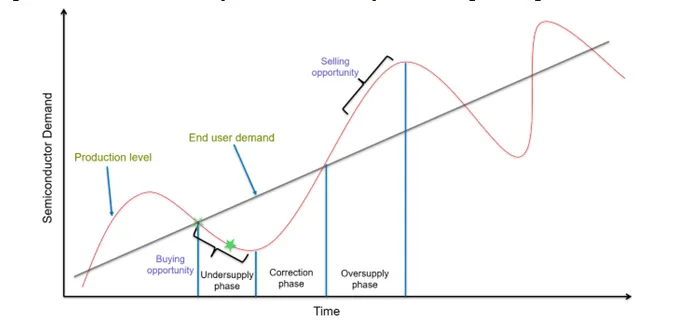

Figure 4: Semiconductor Cycles Are Driven By Fluctuating Sales Growth Numbers

Source: iFast

Source: iFast

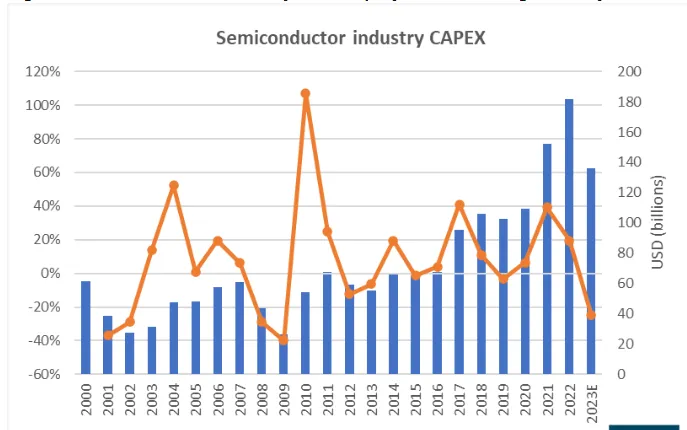

The current downcycle began with a shortage back in 2020. Back then, chipmakers were under enormous pressure from stakeholders and clients to meet the growing demand for semiconductors, which many responded to by ramping up their capacity. Industry capex rose by a staggering 39% and 20% in 2021 and 2022 respectively. Unsurprisingly, this sudden and sharp increase in capex resulted in a supply glut. Today, several chipmakers have already made significant downward revisions to their capex budgets, citing bloated inventory channels as one of the key reasons.

For 2023, industry capex is projected to shrink by 20%. While demand is expected to pick up in 2024, we potentially could see capacity tightness returning due to the lack of capacity expansion in 2023. This potentially could lead to the semiconductor manufacturers having the pricing power.

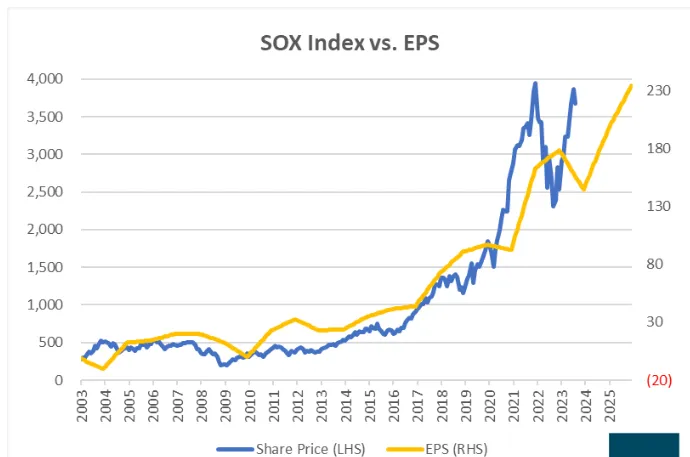

Considering all the factors mentioned above, particularly the structural megatrends such as AI and digitalisation, the reduction in capex in 2023, and comments made by bellwether semiconductor manufacturers, we believe that the semiconductors sector will be one of the best-performing sectors for 2024-2025. And with a recovery of the chip cycle in sight, we see a positive earnings outlook for semiconductor companies in the near to mid-term. The recent selloff has also made valuations slightly more attractive, providing investors with a better entry point.

Figure 5: Semiconductor Industry Capex

Source: Bloomberg, Gartner

Source: Bloomberg, Gartner

Figure 6: Semiconductor Index vs EPS

Source: Bloomberg

Source: Bloomberg