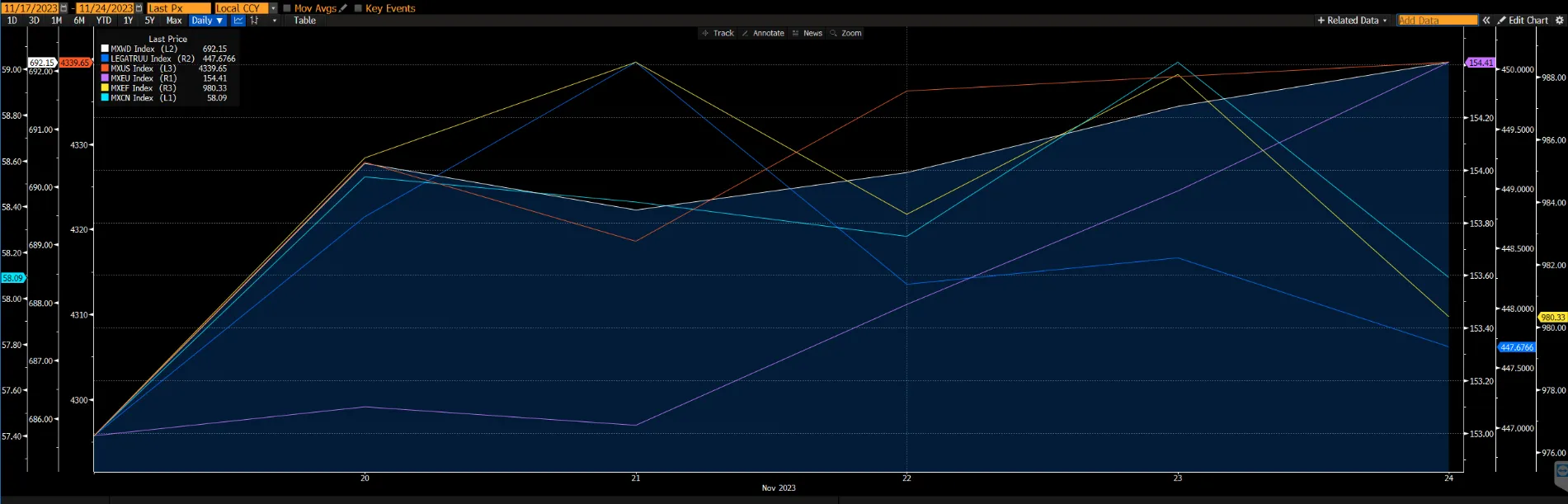

For the fourth consecutive week, the global equities market continued to rise. The index finished higher (+0.97%) amid a shortened trading session as sentiment remained positive, driven by the consensus of the Fed pausing rate hikes in the next meeting on 12-13 December. Driving the rise of the global equities market were the European and the Chinese markets which rose by 1.48% and 1.28% respectively. The US markets increased by 1.04%, a slower rate because of a flat MoM PMI of 50.7. As risk-on sentiment continues, the global fixed-income market increased by 0.17% because of massive inflows into corporate bonds and the treasury markets. Market participants believe interest rates have peaked and no material rate hikes will occur. The US 10-year yield rose 6bps to 4.47%.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

Topic in focus – Some Relief For China’s Property Sector

Chinese leaders are making their most forceful push yet to end the nation’s property crisis, ramping up pressures on banks to plug an estimated $446b shortfall in funding needed to stabilize the industry and deliver millions of unfinished apartments. Policymakers are in the midst of finalizing a draft list of 50 developers eligible for financial support and indicating a pivot by Beijing to help some of the most distressed builders. Meanwhile, the country’s top law-making body said banks should increase funding for developers to reduce the risk of additional defaults and ensure housing projects get finished. This new policy would slow the pace at which the property sector winds down, but it would not turn the market around, in our opinion. A painful adjustment is inevitable. That said, the current speed is untenable. It risks bringing down even top developers causing severe disruptions to the economy and financial system.

We think the reported measures will help constrain the downturn and keep its pace manageable. Ensuring financing for a broader range of developers – public and private – will reduce the odds of a systemic meltdown. Sending the message that the government won't allow the problems to metastasize is also important.

Regulators are reported to be prepping a so-called whitelist of 50 public and private developers to help guide financial institutions as they weigh support for the industry via bank loans, debt, and equity financing. This would expand the prior list of systemically important state-backed firms. The new plan would also add to a raft of recent support measures for the property sector, including mortgage rate cuts for homebuyers, down payment reductions, income tax rebates and a push for urban infrastructure upgrades and affordable housing.

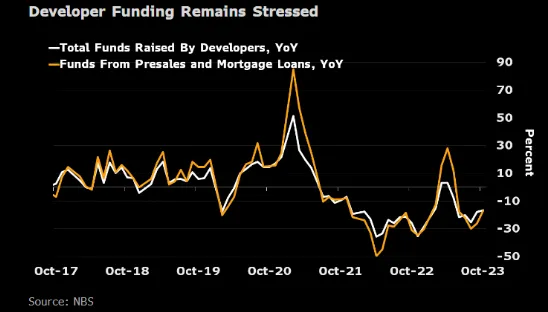

The financial pressures on developers have become intense. Bloomberg estimates firms in the sector need 18.9t yuan (15% of GDP) in 2023 to fill a liquidity shortfall, including short-term liabilities and funds needed to finish pre-sold homes. Next year is likely to see a funding gap of a similar size.

Figure 2: Developers Funding Remains Stressed

Developers are struggling to bring in funds because housing sales continue to disappoint. Both housing demand and supply continue to contract from last year’s depressed levels – despite government efforts to put a floor under the market. The fundamentals behind the housing market have changed – and this fact has sunk in with ordinary home buyers. A shrinking population and slowing urbanization mean that the market must shrink, and prices will likely fall too. Bloomberg estimates that property construction must fall by 30% between 2021-2026 to bring supply in line with demand. A slow economic recovery and a general lack of confidence add to the headwinds.

Without official support, debt defaults and slow construction progress will continue. It is clear that the government would like to wean the economy from its dependence on housing. But it does not want the adjustment to happen too quickly.

China’s government property measures also have a social and political dimension. They are designed to ensure the delivery of homes – a key policy objective for maintaining social stability. Many residential projects have been delayed or even halted since the 2H21, as more developers have fallen into financial distress. This led to boycotts of mortgage payments on pre-purchased homes in mid-2022, which alerted the government to the threat to social stability. Since then, home delivery has become a policy priority.

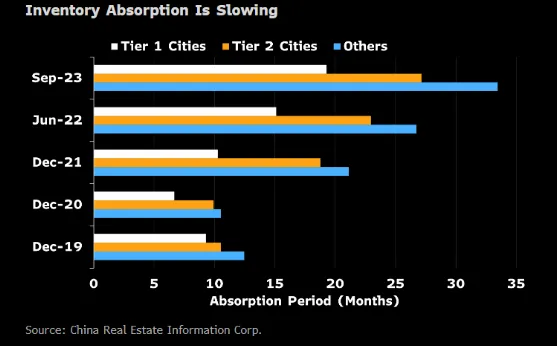

Figure 3: Housing Inventory

Furthermore, the $56t banking industry has been battling shrinking margins and rising bad loans since they were drafted by authorities to backstop the economy and prevent risk spillover from the sluggish property sector. Authorities have guided banks to trim deposit rates three times over the past year to ease their margins pressure and slashed banks’ reserve requirements twice this year to boost their lending capacity. Increasing funding would ease “panicked expectations” of households, said members of the standing committee of the National People's Congress. The comments, by members who have nominal oversight of the central bank under the guidance of the Communist Party’s leadership, add pressure on the PBOC to do more to support the property sector.

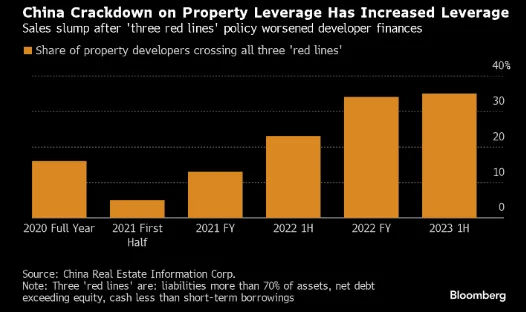

Figure 4: Property Developers’ Leverage

A Bloomberg index of Hong Kong-listed Chinese banks tumbled as much as 18% this year from a high in May, while the big four state banks remain near record low valuations of about 0.4x book value. Although valuations are cheap, we would remain cautious and selective in both the property and banking sectors.