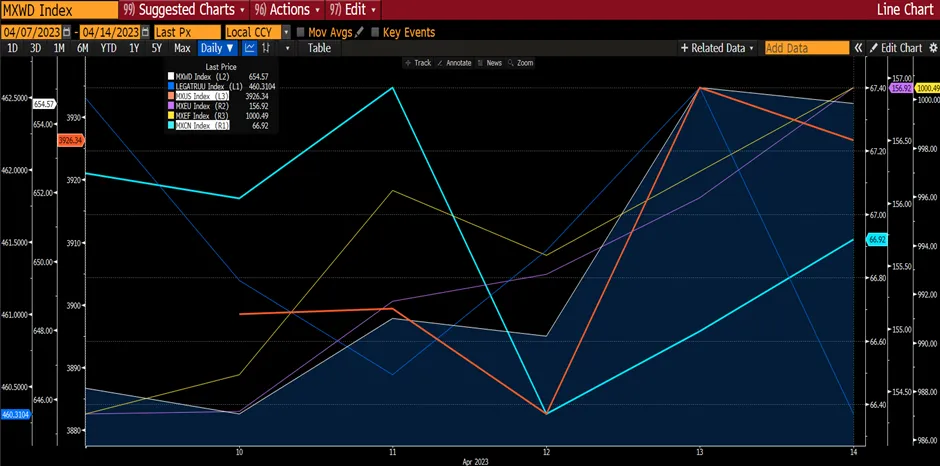

Global markets continued to be volatile but managed gains for the week on the back of 1) banking crisis fear has eased thus investors took on more risk (risk on trade), 2) peak in interest rates is near, 3) Nasdaq has entered a bull market territory, and 4) USD declined in the risk on mood. Overall, market sentiments remain relatively positive. MXWD rose by 3.58% and outperformed the Bloomberg global aggregate total return index that fell by 0.37%. MXUS increased by 3.61% while MXEU surged by 5.15%. MXEF jumped 1.93% on the back of MXCN rising by 2.32%.

Figure 1: Major Indices Week Performance

Source: Bloomberg

Source: Bloomberg

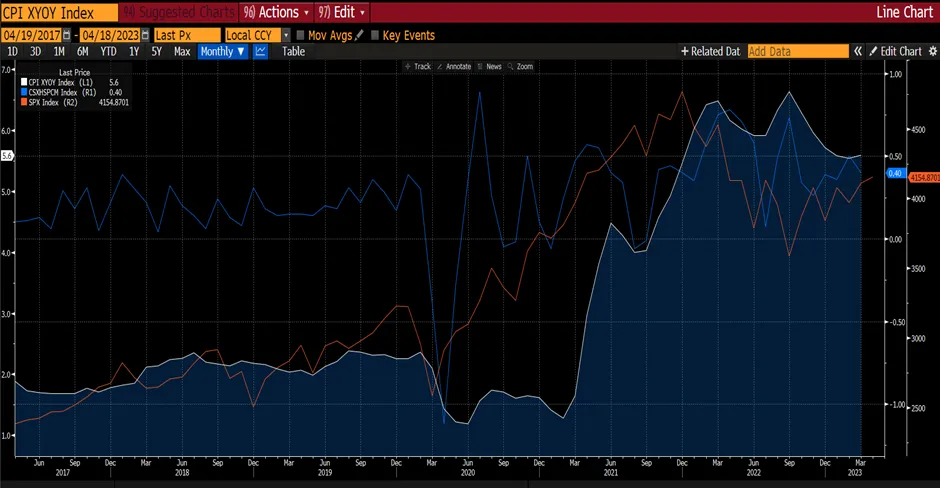

US equities have been range bound for much of the previous week as investors digested the banking sector turmoil. However, as contagion fears steadily eased, the market recovered this week despite rising risk of a recession. Moreover, because of stress within the banking sector, many investors now believe the Fed hiking cycle is ending. The futures market assigns roughly 50% odds of a 25bp hike in May and a greater likelihood of cuts than hikes in subsequent meetings. The recent hiking cycle has been the steepest trajectory of Fed rate hikes among the 6 hiking cycles since 1982. The average of these episodes lasted 20 months and resulted in a 292bp increase in the target fed funds rate. The current cycle has lasted 12 months, and the Fed has raised rates by 475bp.

According to Bloomberg Intelligence, the New York Federal Reserve’s two probability models appear fairly convinced that a recession is likely next year. The yield curve based model, which uses the spread between 10-year and 3-month Treasuries, jumped to 57.1% in January before retreating slightly – surpassing the probabilities recorded ahead of the past 4 recession. Historically, exceeding 30% has accurately predicted recession one year out.

In the last Fed meeting, the Fed hinted that the rate hiking cycle was near the end but not ready for a pivot yet as inflation is still high.

Figure 2: Fed Recession Model

Source: Bloomberg

Source: Bloomberg

Figure 3: Path of Fed Funds During Previous Hikes

During the week, US Tech sector continued to trend higher on positioning for reversal in Fed policy later this year despite earnings recession looks to be deepening and lengthening suggesting the run might still be premature. Because of the rate hike, in March, just 6 names - Microsoft, Apple, Nvidia, Google, Amazon, Meta – accounted for 84% of the SPX’s net move in the month. Together they added almost US$1t in combined market capitalization for the month. This has driven the new bull market in Nasdaq and lifted S&P.

Figure 4: Nasdaq Entering Bull Market Territory

Source: Bloomberg

Source: Bloomberg

The decline in bond yields has supported growth stocks YTD but with wide variation. We therefore would recommend owning high-margin growth stocks instead of low-margin growth stocks, given the current resilient economic growth pricing within equity markets but pessimistic pricing in rates markets. If the economy avoids a recession, real yields are likely to rise and affect low-margin growth stock valuations which are more sensitive to higher yields. If the economy enters recession, equity market pricing of growth will likely deteriorate and investors will be somewhat supported by quality attributes, including high-margin stocks. The key risk is that current equity market pricing of a contained economic slowdown but a dovish Fed persists.

**Two major news that came out of China this week that drove the China market higher. **

Firstly, Premier Li’s keynote speech at Boao Forum where he cited that China’s economy is showing “strong momentum” despite a challenging global environment, promising to bolster support for business as the country emerges from strict Covid controls that hammered GDP. “Judging from the situation in March, it is better than in January and February”. In his speech, Beijing would focus on preventing major financial risks, promising further support to the private sector still reeling from a regulatory crackdown on the property, technology and private education industries. He also vowed to reconnect the Chinese economy to the world. Overall, a very supportive tone and encouraging for the recovering economy.

Secondly, Alibaba announced the group reorganization plan into six independently run units, followed by JD.com which also announced plans to list two units in Hong Kong.

Alibaba was the most talked about this week. On March 28, Alibaba's CEO Daniel Zhang shared a company-wide letter that announced Alibaba will begin a group reorganization of its business units (China Commerce, Cloud, International Commerce, Cainiao, Local Consumer Service, Digital Media & Entertainment) into six independently run entities with respective standalone board governance (for quicker decision-making), self-financing/listing capabilities (reviving of entrepreneurial spirit, with greater focus on financial health) and leaner holdco back-end operations (lowering headquarter costs).

Figure 5: Alibaba’s Share Price Trend

Source: Bloomberg

Source: Bloomberg

We see potential positives from the spin-off, including: (1) potentially faster profit turnaround of non-China Commerce businesses given all six entities will have to be self-sustainable, (2) lower costs at the headquarters level on a leaner back-end, (3) greater value appreciation of the different ‘parts’ of Alibaba’s businesses, especially for the independent China Commerce business and AliCloud business in the future, and (4) potentially lower employee share count dilution at the Alibaba holdco level if ESOP programs are applied within each subsidiary’s own capital.

In our opinion, the key takeaway from the announcement is Alibaba after years of “knocking heads” with the government, the proposed breakup would suggest that Alibaba has gotten the blessing from Beijing. It follows revelation that the government planned to take golden shares in Alibaba and other tech giants like Tencent – a small stake that includes a board seat and veto power over some decisions. Furthermore, we don’t think that it is purely coincidental that the disclosure was made at the same time Jack Ma returned to China after 2 years away from the spotlight. This breakup and spinoffs for Alibaba is an opportunity to move forward and suggests that government crackdown on internet companies has eased. The breakup of Alibaba would also help unlock shareholder value within the group with potential to improve valuation as well as the choice for shareholders to own the business which they prefer.

After the split, the units will include a cloud intelligence division, a digital business unit, Taobao Tmall online shopping, local services such as meal delivery, Cainiao logistics and digital media and entertainment. Each of these are among the leading players in their respective fields, but as separately run entities, it will become increasingly harder to lean on stablemates for data and customer referrals. Each will also explore their own fundraising, possibly including share listings. Equity and bond offerings tend to shine a light on the finances of a business, so their respective management teams will be looking to tighten up operations and hasten a drive toward profitability for those that have yet to break even.

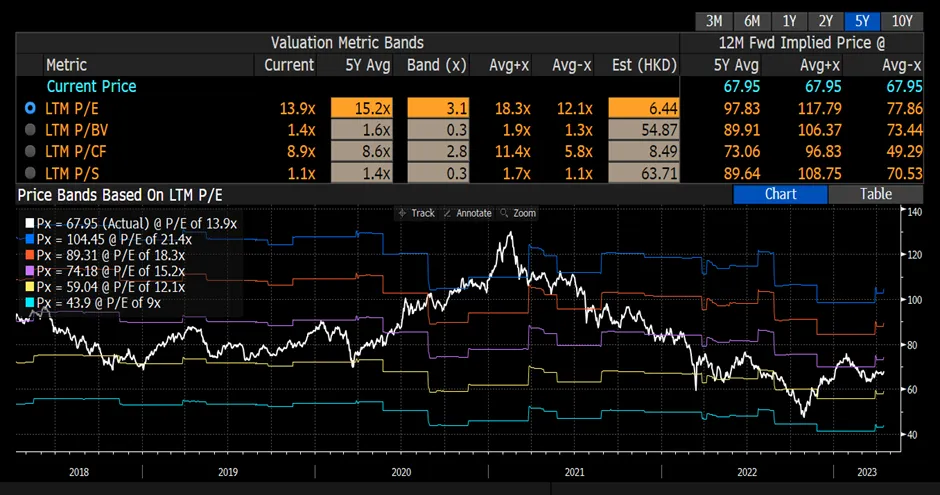

Figure 6: Sum of Parts Valuation

We see Alibaba as a quality and value stock with proxies to enjoy the advertising recovery, fintech (via. 33%-owned Ant) and cloud structural growth as we see large room for valuation multiple re-rating as its top line growth resumes and 2023-25 earnings resume to teens growth. Growth would be driven by (1) back to positive advertising + commission growth from June 2023 quarter, (2) plateauing of competing live-streaming shopping format in a reopening year, (3) next growth drivers across AliCloud and international (Lazada), entering into an easy base, (4) upward earnings revision, and (5) attractive valuation that is trading below its historical average.

Figure 7: Alibaba Valuation

Source: Bloomberg

Source: Bloomberg

Figure 8: Earnings Revision

Source: Bloomberg

Source: Bloomberg