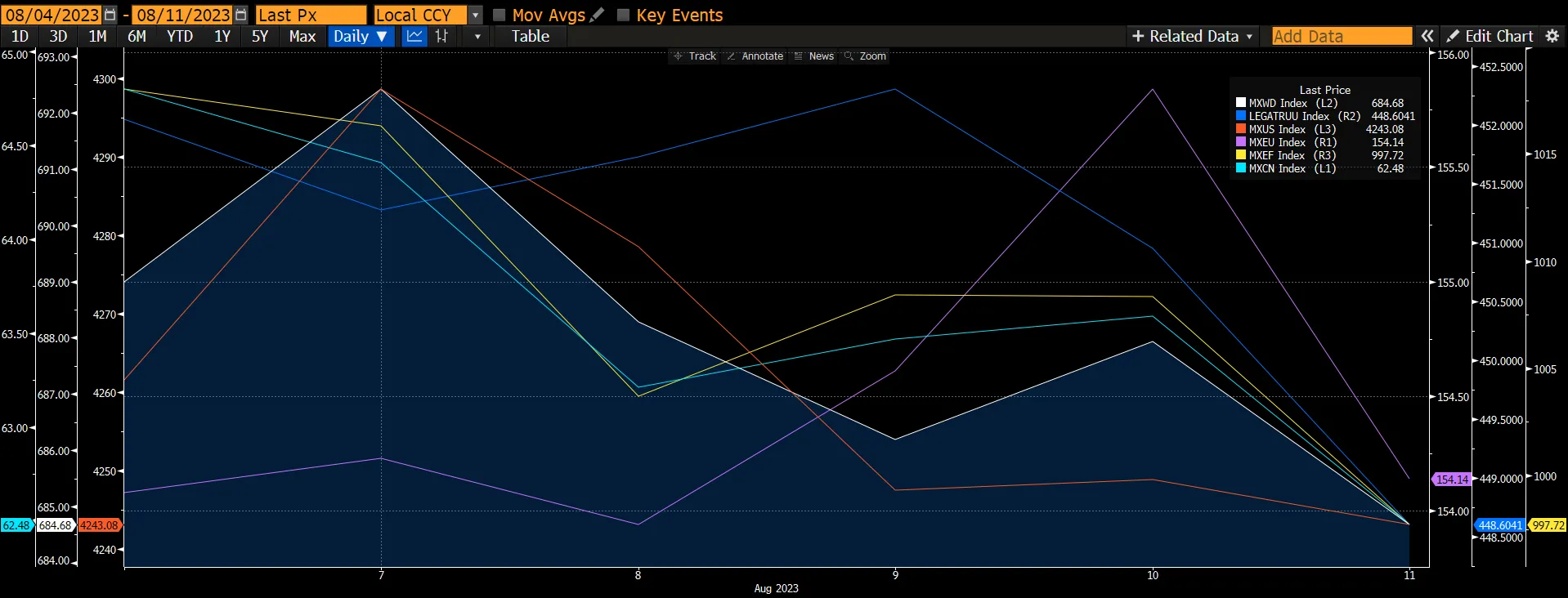

For the consecutive second week, the global equity market sustained a decline, propelled by a complex interplay of data signals emanating from the US producer price index (PPI) and consumer price index (CPI), coupled with the deepening economic challenges in China. The latter has been exacerbated by the specter of potential defaults by property enterprises and a consequential descent into deflation. The broader global equity market registered a decrement of 0.57%, largely attributed to a pronounced downturn in the Chinese market by -3.65%. Parallelly, both the US and European markets experienced contractions of 0.39% and 0.63%, respectively. Furthermore, the fixed-income market unexpectedly underwent a 0.76% decrease, a reflection of apprehensions regarding escalating default risks.

Figure 1: Major Indices Performance

Source: Bloomberg

Source: Bloomberg

This week, markets were treated to a relatively benign US consumer price index report for July. True, consumer inflation remains above the Federal Reserve’s 2% target, and the July producer price index came in higher than expected. But on balance, the drop in core consumer inflation should convince the Fed to keep policy rates on hold in September. However, we do expect another rate hike in the near future meetings as the tone of the minutes from the Fed’s July policy meeting to be released next week will continue to have a hawkish bias, especially as inflation expectations show signs of rising again. This rise is largely due to a rise in oil prices. Our assessment aligns with the projection of elevated Brent crude oil prices for the remaining duration of this year, compounded by the impending hurricane season.

Figure 2: Oil Prices Heads Higher Due To Undersupply

Source: Bloomberg

Source: Bloomberg

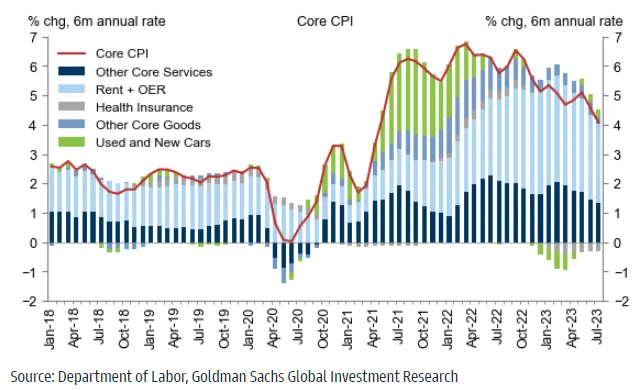

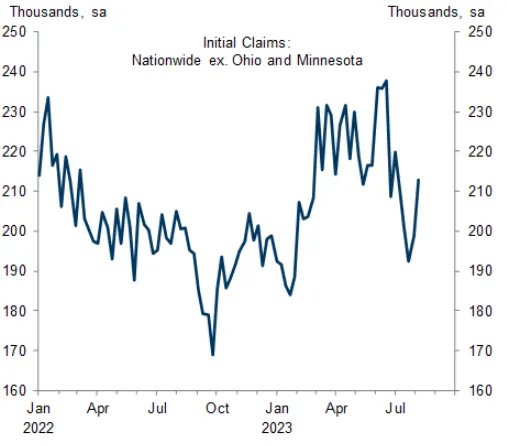

July’s US core CPI rose by 0.16%, matching the 28-month-low pace in the previous month and 4bp below consensus. The YoY rate fell one-tenth to 4.7%. The composition was slightly firmer because another surprisingly sharp decline in airfares lowered the monthly core reading by 6bps. Outside of that, the report was broadly encouraging from a disinflation perspective. Rent inflation slowed further, wage-sensitive services categories were softer, and the 1.3% drop in used car prices represents the early stages of a larger pullback. This report could further reduce the possibility of a September rate hike. The market is currently expecting an 11% chance of a rate hike. Supporting the reduced chance, initial jobless claims had increased 21k to 248k, above consensus expectations.

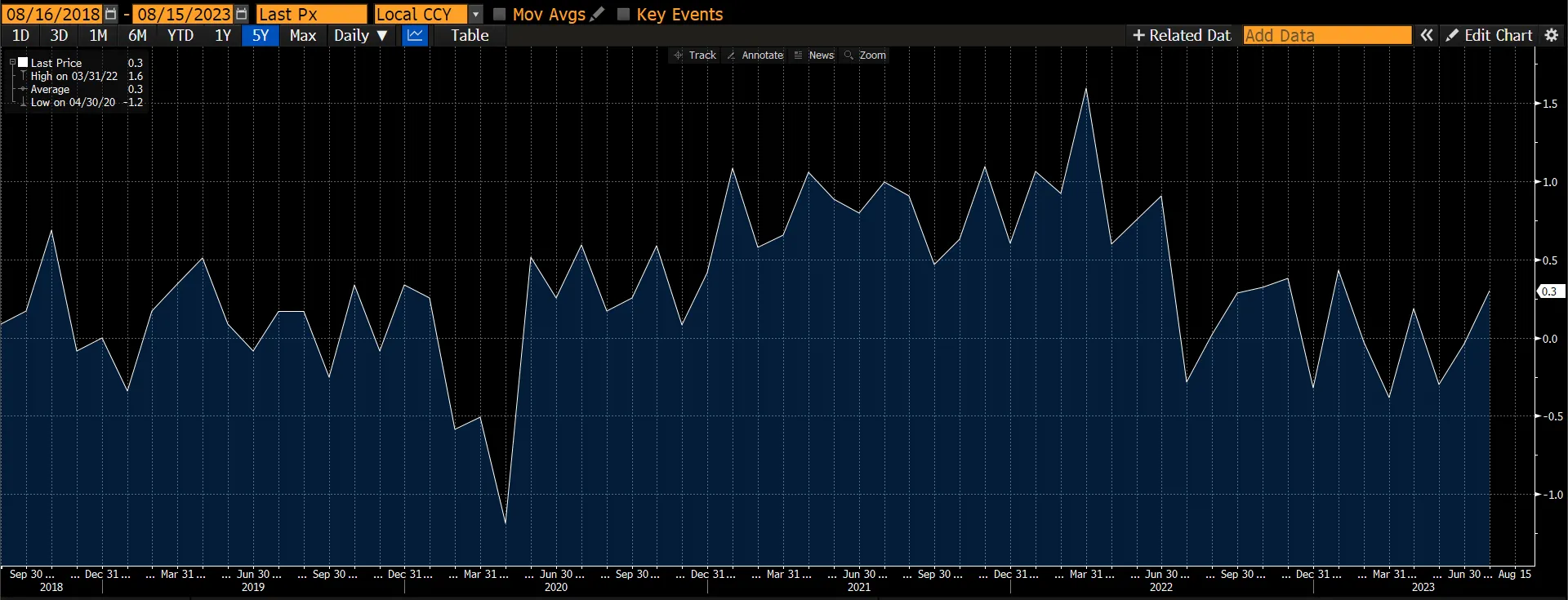

However, the producer price index (PPI) increased by 0.3% in July, one-tenth above consensus expectations. Core measures were stronger than consensus expectations, as the PPI excluding food and energy increased by 0.3% and the PPI excluding food, energy, and trade services increased by 0.2%. These recent data releases had therefore created mixed signals for investors.

Figure 3: Core CPI Falling

Figure 4: Nationwide Initial Claims

Source: Department of Labour

Source: Department of Labour

Figure 5: US PPI Final Demand MoM SA

Source: Bloomberg

Source: Bloomberg

The Chinese market performance continues to be plagued by numerous negative newsflows throughout the week.

- China's geopolitical tensions remained in focus on President Biden’s curbs on US investments in China and comments on China’s economic problems, while China announced the lifting of the ban on group travel to more than 70 locations globally. Not surprisingly, Taiwan remains out of the list. Also, at a political fundraiser, Biden described China as a “ticking time bomb in many cases” because of the economic challenges it is facing. Biden’s remarks were reminiscent of comments he made at another fundraiser in June when he referred to President Xi as a “dictator”. China called the remarks a provocation.

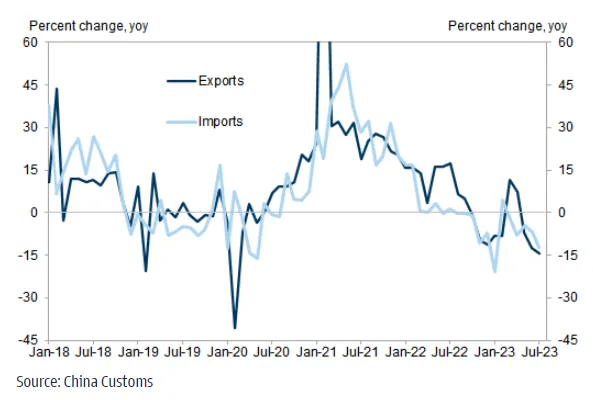

- Both export and import values declined sharply in July in YoY terms, below the consensus forecast. The weakness in exports was broad-based across major trading partners and products, suggesting soft external demand. The import value of commodities declined somewhat on a YoY basis, partially due to a high base of commodity prices last year. China's trade surplus rose further in July (US$80.6b vs. US$70.6b in June).

Figure 6: China Trade Growth Surprised On The Downside In July

-

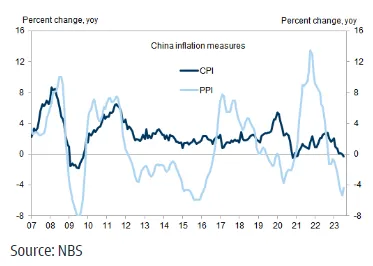

China's headline CPI inflation turned negative in July for the first time since early 2021, though slightly above consensus expectations. China’s headline CPI edged down to -0.3% YoY in July from 0% in June primarily driven by a high base of food prices last July. PPI inflation rose in July in YoY terms but below consensus expectations. China’s inflation problem is of a different order. The headline consumer price figure for July indicated that the country has fallen into deflation.

-

China’s largest property developer by sales missed coupon payments on two international bonds, and trading halted on other bonds. The blow to investor confidence and the risk of contagion cannot be overstated. While the Chinese property sector might be considered a special case, the events unfolding help explain why we should avoid non-investment-grade corporate bonds overall. Indeed, the problems of noninvestment-grade property-related debtors are not confined to China, with a high-profile US office-space company admitting there was “substantial doubt” it could continue its operations.

Figure 7: Headline CPI Inflation Turned Negative

-

Year-over-year PPI inflation increased to -4.4% YoY in July from -5.4% YoY in June. In MoM terms, PPI inflation rose to -2.3% in July (vs. -7.2% in June). PPI inflation in producer goods rose to -5.5% YoY in July from -6.8% YoY in June, and PPI inflation in consumer goods edged up to -0.4% YoY in July (vs. -0.5% YoY in June). NBS commented that the PPI of upstream sectors rebounded on rising prices of crude oil and non-ferrous metals.

-

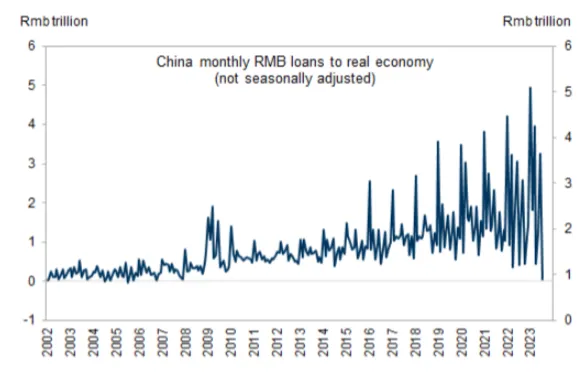

The July money and credit data released on Friday (11 August) missed expectations by a large margin. New flows of Total Social Financing (TSF) were only RMB528b in July, not even half the size of consensus expectations (RMB1100b). RMB loans to the real economy plummeted to RMB36.4b, the lowest since 2006. Even taking into consideration the more pronounced seasonality observed in recent years, this week's print was no doubt soft. It underscores the weak demand in the economy and the need for the government to implement more easing measures.

Figure 8: RMB Loans To The Real Economy Fell In July

Source: PBOC

Source: PBOC

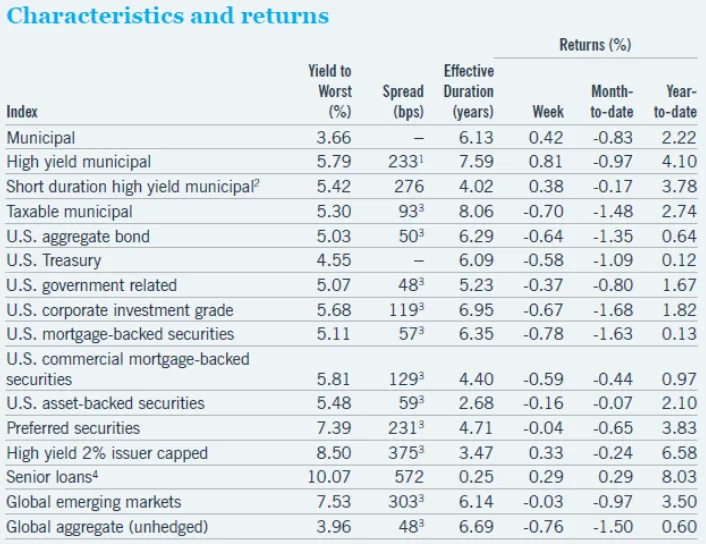

On the fixed income front, U.S. Treasury yields increased last week, with the 10-year yield rising 12bps to 4.16%. The entire curve shifted higher, with 2-year yields up 13 bps. July’s consumer price inflation came in close to expectations, while producer prices rose more than expected. The releases point to an increase in PCE inflation (the Fed’s preferred measure) of around 0.3% for last month. The gap between two-year and 10-year yields is still about -80bp. Historically, an inverted curve has been a lead indicator of recession which we expect to occur in the latter part of this year.

June’s industrial production for Germany was weaker than expected, falling by 1.7%, given lower output in the automotive and construction industries; the figure was flat in May. The yield on 10-year Bunds declined by 3bp to 2.53% over the week.

UK GDP in the three months from April to June expanded by a higher-than-expected 0.2% sequentially (or 0.4% YoY). In June alone, the economy grew by a better-than-expected 0.5% from the previous month. In addition, industrial production in June expanded by a better-than-expected 0.7% year-on-year, which was the first increase in industrial activity since September 2021. Ten-year gilt yields were largely unchanged, declining by 2bp to 4.36% over the week.

Figure 9. Yield Changes Across Fixed Income Universe

Source: Fidelity Investments

Source: Fidelity Investments

Investment grade corporates weakened, returning -0.67% for the week, though the asset class outpaced similar-duration Treasuries by 1 bps. The new issue market was relatively active, at nearly $38b.

High-yield corporates performed well, returning 0.33% for the week and outperforming similar-duration Treasuries by 72 bps. Moody's warns it may downgrade some major lenders after cutting the credit ratings of 10 small- to mid-sized US banks. Rising interest rates and slowing economic growth have led to a more challenging backdrop for banks, bringing pressure on their fixed-rate assets and leading to higher funding costs and increased credit losses (with risks growing in commercial real estate loans).

The yield spread between double-B and triple-C high-yield bonds in the US narrows to its lowest level for 15 months. Having been as high as 8.5 percentage points as recently as April, the gap is now well below 7 percentage points as markets appear to see a reduced likelihood of a US recession following some better-than-expected US economic data, which may also be contributing to increased investor risk appetite.

Emerging markets were mixed, returning 0.03% for the week but beating similar-duration Treasuries by 60 bps. Economic data in China was very weak. Total social financing, a measure of credit growth, slowed to 8.9% year-over-year, as loan creation dropped sharply. New loans totalled RMB346b in July, the lowest monthly print since 2009. Announced fiscal easing also disappointed expectations, presenting downside risks to Chinese growth this year. Outflows from emerging markets funds exceeded the movements in US markets, with around -$1.6b combined leaving hard- and local-currency funds.

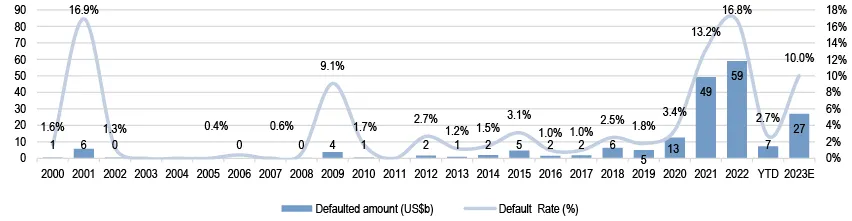

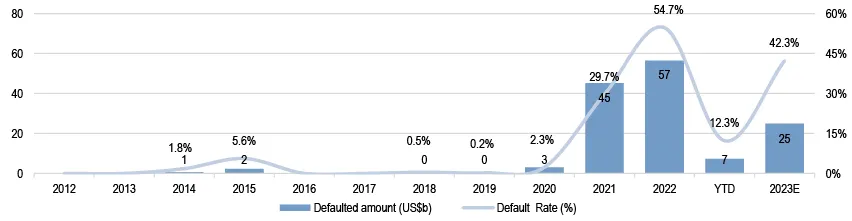

We see Country Garden’s default as the final nail for the China HY property sector. This event would add US$9.9b to the Asia default tally, bringing the YTD total default amount to US$17b and the default rate to 6.4%. This may not be the end, as other smaller surviving names feel the reverberations of this event. We still see another US$10b of HY bonds at risk for the remainder of the year, which could push the full-year default amount even higher to US$27 billion (10% default rate).

We believe that this default would likely prolong the downturn of the physical housing market as potential home buyers turn even more cautious. Prior to Country Garden, the China HY property sector had already chalked up US$109b of cumulative defaults since the beginning of 2021. The sector accounts for 94% of total defaults in Asia over that time frame. This has effectively wiped out close to 55% of the US$203b China property bond stock (IG + HY) outstanding at the end of 2020. The removal of defaulted names and distressed prices has caused the market capitalization of the China HY property sector to shrink to US$8b from a peak of US$103b. We also see a higher risk of contagion not only across the sector but also possible spillover to the wider economy. We fear that Country Garden’s default may cause the banks to become more risk-averse and selective.

Figure 10: Asia HY Corporate Default Rate Is Expecting To Hit 10% This Year.

Source: J.P. Morgan

Source: J.P. Morgan

Figure 11. China HY Property Default Rate Can Hit 42%, Close To 2022 With Evergrande Default.

Source: J.P. Morgan

Source: J.P. Morgan