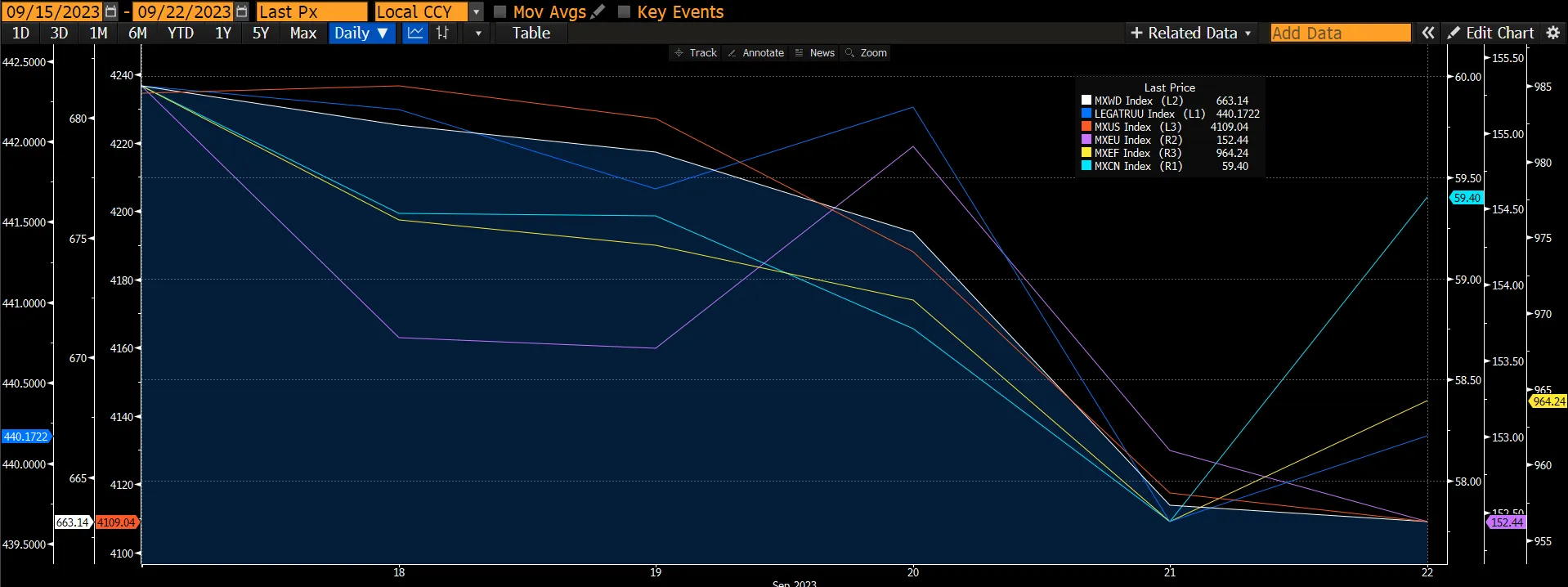

The Global Equities Markets fell sharply (-2.65%) after the Fed announced a hawkish pause leading to investors having to digest corporate and macro cross currents. The US market led the decline of 2.95% on the back of hawkish comments from the Fed; rates were held steady, but a further hike is on the cards by the end of the year. The European equities market fell by 1.95% as BOE, ECB, and SNB reiterated the possibility of further rate hikes. The Chinese equities market ended lower by 0.8% partly cushioned by policymakers further eased measures in the property market (including Guangzhou City further relaxing home purchasing rules). Furthermore, Beijing and Shanghai eased foreign capital transfers. The Fixed Income index fell by 0.49%, outperforming the global equities, on the hawkish Fed’s stance that drove yields higher.

Figure 1. Major Indices Performance

Source: Bloomberg

Source: Bloomberg

Topic of the week – Fed funds rate decision

Last week The Fed delivered a more “hawkish hold” than what markets had expected, and Treasury yields reached new cycle highs.

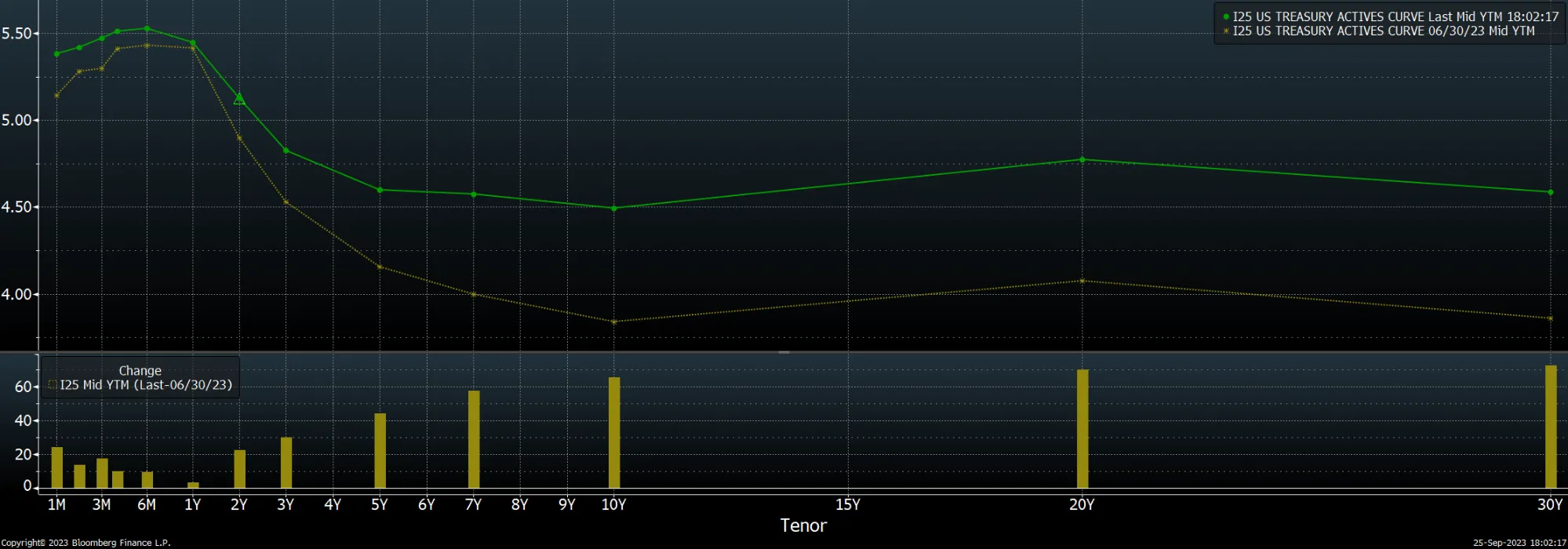

Figure 2. Yields are up across all maturities of US Treasuries since end of Q2 2023, with sharp increase in longer-term bonds.

Source: Bloomberg

Source: Bloomberg

Treasury yields continue their march higher, rising 9-12bp over the week with the belly leading the way. With this move, yields reached YTD and cycle highs across the curve, and in some cases, moved to the highest levels observed since prior to the onset of the Global Financial Crisis.

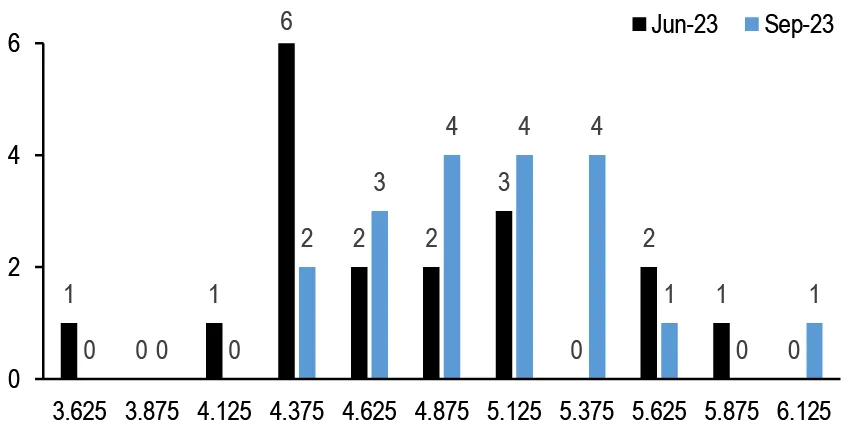

As expected, the post-meeting FOMC statement was little changed, with forward guidance maintaining the same hawkish tone it has for the last two meetings. Away from the statement, the updated Summary of Economic Projections skewed even more hawkishly: the 2024 and 2025 median dots were both revised higher by 50bp, supported by stronger growth outturns and inflation projections remaining above target through 2026.

Figure 3. Fed dots are more hawkish now.

Source: Goldman Sachs

Source: Goldman Sachs

Figure 4. The latest SEP shows that the Fed expects to cut policy rates less than previously.

Source: Federal Reserve

Source: Federal Reserve

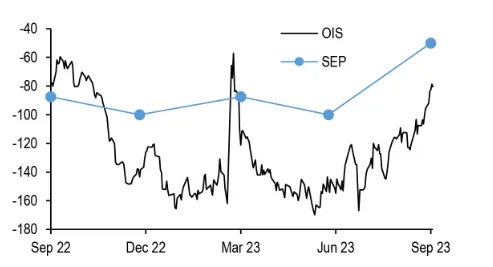

In the press conference it appeared that Chair Powell did not want to close off any options: on one hand, Chair talk about “how far we have come” with respect to policy tightening. However, he also emphasized that “We want to see convincing evidence, really, that we have reached the appropriate level, and we have seen progress and we welcome that, but we need to see more progress before we will be willing to reach that conclusion.”

Thus, it’s no surprise that markets are now pricing in a greater than 60% probability of another hike in coming months, and terminal has been pushed out further, with the peak OIS forward rate being priced in February 2024, while at the same time not pricing in a full ease until summer 2024.

Figure 5. OIS curve has steepened sharply

Source: J.P. Morgan

Source: J.P. Morgan

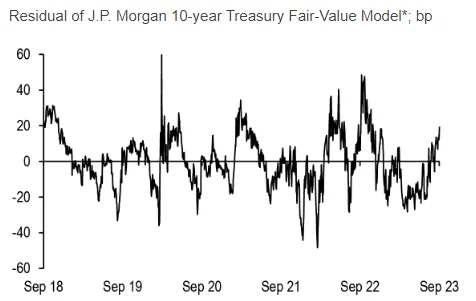

Figure 6. Treasuries seem to be priced cheaper.

Overall, despite more hawkish stance of Fed, fundamentals imply adding more duration might be a good medium-term play.