US

US stocks gave back a portion of the past several weeks’ solid gains as investors appeared to rotate into sectors that lagged in 2023, including utilities, energy, consumer staples, and health care. Conversely, a slide in Apple shares following an analyst downgrade weighed on the large-cap, technology-heavy Nasdaq Composite Index.

Last week’s headline labour market data generally surprised on the upside, although underlying trends were more mixed. The closely watched monthly non-farm payroll report showed that employers added 216,000 jobs in December, well above consensus forecasts. Monthly growth in average hourly earnings stayed steady at 0.4%, slightly above expectations, and the unemployment rate similarly defied expectations by remaining at 3.7%. The workforce participation rate fell back unexpectedly to 62.5%, however, its lowest level since February. The ISM’s Non-Manufacturing Employment Index also fell sharply into contraction territory and hit its lowest level since July 2020.

UK

Despite global geopolitical fears, UK data released this week was quite promising. Demand for loans to purchase homes continued to recover — albeit from low levels — in the final month of 2023. Mortgage approvals increased to just above 50,000 from 47,890 in November, as lower mortgage rates and hopes of a cut in borrowing costs contributed to a 1.1% month-over-month uptick in home prices, according to a survey by mortgage lender Halifax.

Closely watched purchasing managers indexes (PMIs) show that Britain’s services sector saw the fastest jump in activity in December for six months, beating expectations. The final composite PMI - covering both manufacturing and services - rose to 52.1 in December, up from 50.7 in November in what was the best performance of all the world’s major economies. A reading above 50 indicates growth.

However, none of this good news managed to stop the FTSE 100 from falling on its 40th birthday week. The UK benchmark lost -0.56% during the first week of trading in 2024.

Europe

The pan-European STOXX Europe 600 Index ended the week lower and snapped seven consecutive weekly gains, as optimism for an early cut in interest rates waned. Major stock indexes mainly fell. France’s CAC 40 Index declined a whopping 1.62%, while Germany’s DAX lost 0.94%.

European government bonds fell sharply, sending yields higher, as traders pared aggressive rate-cut expectations. The yield on the benchmark 10-year German bund rose to more than 2.1%, while in Italy, the 10-year government bond yield closed the week above 3.8%. In the UK, the 10-year gilt ended with an almost 3.8% yield. The eurozone could well already be in recession after a contraction in business activity continued at the end of 2023.

Asia

Stocks in China retreated amid persistent concerns about its economy. The Shanghai Composite Index fell 1.54%, while the blue-chip CSI 300 gave up 2.97%. In Hong Kong, the benchmark Hang Seng Index declined 3%, according to FactSet.

Economic data for December continued to show a varied picture of China’s economy. The official manufacturing Purchasing Managers ‘Index (PMI) contracted for the third consecutive month, falling to a below-consensus 49.0 in December as declines in new orders and exports accelerated. The non-manufacturing PMI rose to 50.4 from 50.2 in November as stronger construction activity offset weakness in the services sector. Readings above 50 represent growth from the prior month.

Topic of the week – Indonesia equity outlook

Indonesia equity markets outperformed the broader Asia and emerging market indices for three consecutive years over 2021-23, with the Jakarta Composite Index (JCI) delivering a 7.5% return last year in USD terms thanks to strong FDI flow momentum as the government pushes for continued reforms, as Indonesia is one of the key beneficiaries of shifting supply chains within Asia, particularly the metals and EV spaces. JCI’s total market cap reached US$760bn as of 2023, the largest in Southeast Asia, but it is still overall under-penetrated for capital market size, at 63% of Indonesia’s ~US$1.2tn GDP. We believe Indonesia will continue to deliver outperformance in 2024, and it is one of our key OW markets within ASEAN, Asia ex Japan and EM given its structural reform, but highlights potential additional volatility in 1H24 from election period. Indonesia will also likely see GDP per Capital crossing USD 5,000 sweet spot mark in 2024, like China back in 2011, whereby we expect new wave of consumer spending to happen.

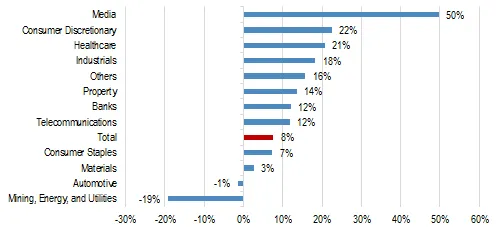

Figure 1: 2024 expected earnings growth by sector.

Key themes for 2024

2024 election year. All eyes on the upcoming 14th Feb 2024 presidential election. There are 3 presidential candidates competing in the race: 1) Prabowo & Gibran 2) Ganjar & Mahfud 3) Anies & Muhaimin. If nobody wins more than 50% vote on the first round, there will be 2nd round of election on 26th Jun 2024. There will be a nationwide governor election on 27th Nov 2024.

Potential rate reversal cycle. We expect rate reversal cycle (both Fed rate and BI rate) to materialize in 2H24, where we see upside risks to long duration assets, growth basket, and rates-sensitive names.

Current account transformation. We believe the metal downstreaming industry, which underpinned by Indonesia’s sustainable current account surplus. Assuming that nickel remains a key input into EVs, we expect nickel exports could rise by another USD 8-10 bn over the next 5 years.

EV ecosystem and FDI. Indonesia’s pathway to building EV ecosystem started from the upstream, nickel ore to sulphate, and automotive plants in the past 2-3 years and moving towards battery plants next. We see 2024 likely will be an inflection point towards electrification in Indonesia.

Green energy transition. As of 1H23, Indonesia’s renewable energy installed capacity is 12.7 GW requiring an additional 10-11 GW to meet the 2030 target. Assuming US$3mn/MW average capex outlay, the 2025 target implies needing US$30-33 bn worth of total investment.